PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064008

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064008

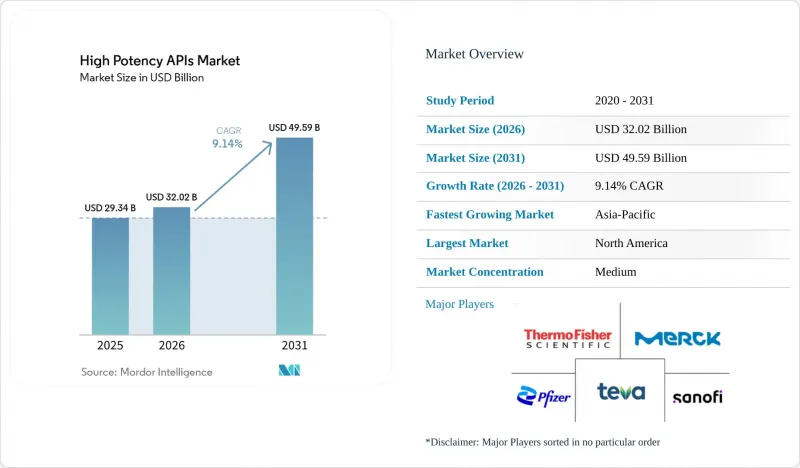

High Potency APIs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the high potency aPIs market size is projected to be USD 29.34 billion in 2025, USD 32.02 billion in 2026, and reach USD 49.59 billion by 2031, growing at a CAGR of 9.14% from 2026 to 2031.

This report is Segmented by Product Type (Innovative HPAPIs and Generic HPAPIs), Application (Oncology, Hormonal Disorders, and More), Synthesis Route (Synthetic HPAPIs and Biotech HPAPIs), Manufacturer Type (Captive Manufacturers and Merchant Manufacturers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global High Potency APIs Market Trends and Insights

Increasing Prevalence of Chronic and Oncologic Diseases

Cancer-related APIs already constitute 73.23% of overall demand, and 28% of FDA new molecular entity approvals in 2024 fell into the highly potent category. Emerging metabolic-disorder blockbusters such as semaglutide generated USD 138.90 million in 2024 sales, demonstrating commercial traction beyond oncology. Cytotoxic payloads within antibody-drug conjugates require occupational exposure limits below 10 µg/m3, thereby mandating high-containment installations that smaller plants cannot support. An aging global population further increases chronic-disease prevalence and extends therapy durations, lifting baseline API volumes. Accelerated-approval pathways compress development cycles, compelling sponsors to secure capable manufacturing slots early in clinical planning.

Expansion of Contract Development and Manufacturing Organizations

The global CDMO segment is projected to grow, propelled by sponsors' preference to externalize high-risk processes. Smaller biotech firms lacking internal containment infrastructure now represent a majority of HPAPI outsourcing volume, deepening order books for service providers. The BIOSECURE Act obliges US firms to sever Chinese CDMO links by 2032, directing fresh mandates toward Indian and European vendors; Indian outfits such as Aurigene and Aragen Life Science reported double-digit inquiry spikes in 2024. Specialized CDMOs must therefore scale cytotoxic suites, continuous-flow units, and occupational-hygiene labs in parallel. Lonza has reorganized into three divisions, including a dedicated Specialized Modalities arm, to align resources with this trajectory.

Stringent Global Regulatory and Occupational Safety Standards

EMA's updated Variations Regulation effective January 2025 demands deeper validation records for post-approval changes, lengthening documentation lead-times. OSHA's hazardous-drug directives in the United States oblige multi-stage air-locking and specialized PPE, cutting production efficiency by up to 15% relative to conventional pharmaceuticals. PIC/S Annex 1, enforced from August 2024, embeds quality-risk management into sterile containment, compelling retrofit projects at legacy plants. China's broadened Anti-Espionage Law has prompted some European inspectorates to halt on-site audits, risking delayed release for Chinese-sourced intermediates. Collectively, these layers inflate compliance budgets and favor incumbents with established regulatory affairs teams.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Targeted and Personalized Therapies

- Technological Advancements in High-Containment Manufacturing

- High Capital and Operational Expenditure Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Innovative compounds generated the bulk of 2025 revenue, capturing 61.89% owing to patent-protected assets that deliver premium returns capable of offsetting high fixed costs. Continuous inflows of FDA approvals-50 NMEs in 2024, 91% of which were small molecules-maintain the innovation pipeline. CDMOs supporting first-in-class assets negotiate multi-year exclusivity packages, assuring capacity monetization.

Generic HPAPIs, though smaller, are set to grow at 11.18% CAGR through 2031 as blockbuster oncology agents face expirations. Specialized manufacturers such as Aarti Pharmalabs commercialized 54 APIs in FY 2023-24, signaling maturing capability in replicating complex processes without compromising containment.

The oncology franchise accounted for 72.53% of 2025 spend, reflecting cytotoxic dosing requirements that inherently demand robust containment. Lonza's Stein, Switzerland campus has seen repeated ADC capacity expansions to meet sponsor demand.

Glaucoma and broader ophthalmology segments, though comparatively small, exhibit the fastest momentum at 12.61% CAGR through 2031, aided by next-generation controlled-release implants such as Glaukos's Epioxa, which secured FDA NDA acceptance with an October 2025 PDUFA date.

Geography Analysis

North America dominates gross revenue, absorbing 39.62% of 2025 demand on the back of a dense innovator ecosystem and an advanced regulatory environment. Pfizer's USD 465 million Kalamazoo expansion underscores its entrenched commitment to domestic API capability. CARES-Act funding and state-level incentives offset a portion of the capital burden, while the BIOSECURE Act's 2032 deadline expedites further reshoring. Canada's alignment with FDA CGMP standards allows seamless cross-border distribution, and Piramal Pharma Solutions recently committed CAD 25 million to expand its Aurora HPAPI output. The high-potency APIs market continues to see additional brownfield retrofits that bring legacy North American sites into compliance with Annex 1 and OSHA revisions.

Asia-Pacific registers the highest regional CAGR at 10.32% through 2031. India's CDMO sector is driven by Western sponsor diversification. Facility additions in Hyderabad and Visakhapatnam gear toward cytotoxic and peptide synthesis, supported by India's Production Linked Incentive scheme. China retains a cost-lead position but faces compliance headwinds following the Anti-Espionage Law, leading some multinationals to dual-source. Singapore's biologics initiative and South Korea's regulatory harmonization further cement APAC's stature as a multi-modality HPAPI hub.

Europe remains a pivotal manufacturing node, especially for complex biologics and conjugates. EMA's Variations Regulation harmonizes procedural clarity, easing pan-EU lifecycle management. Switzerland, outside the EU but deeply integrated, hosts Lonza's flagship sites that anchor European antibody-drug conjugate output. The European Commission's Critical Medicines Act lists 270 APIs for strategic support, opening grant pathways for plant retrofits and capacity expansions. Attractive electricity-price hedging and experienced labor pools keep Western European facilities competitive despite higher operating costs.

- Abbvie

- Merck

- Corden Pharma

- Pfizer

- Sanofi - EUROAPI

- SK Biotek

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Thermo Fisher Scientific

- Viatris

- Lonza Group

- WuXi App Tec

- Cambrex

- Dishman Carbogen Amcis

- Piramal Group

- Sterling Pharma Solutions

- Siegfried Holding

- Evonik Health Care

- Novasep (Seqens)

- Delpharm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic and Oncologic Diseases

- 4.2.2 Growing Biopharmaceutical Research and Development Investments

- 4.2.3 Expansion of Contract Development and Manufacturing Organizations

- 4.2.4 Rising Demand for Targeted and Personalized Therapies

- 4.2.5 Technological Advancements in High-Containment Manufacturing

- 4.2.6 Government Incentives and Reshoring Initiatives for Domestic API Production

- 4.3 Market Restraints

- 4.3.1 High Capital and Operational Expenditure Requirements

- 4.3.2 Stringent Global Regulatory and Occupational Safety Standards

- 4.3.3 Dependence on Limited Suppliers for Specialized Raw Materials and Equipment

- 4.3.4 Shortage of Skilled Workforce in High-Potency Manufacturing Facilities

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Innovative HPAPIs

- 5.1.2 Generic HPAPIs

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Hormonal Disorders

- 5.2.3 Glaucoma

- 5.2.4 Other Applications

- 5.3 By Synthesis Route

- 5.3.1 Synthetic HPAPIs

- 5.3.2 Biotech HPAPIs

- 5.4 By Manufacturer Type

- 5.4.1 Captive Manufacturers

- 5.4.2 Merchant Manufacturers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 Merck KGaA

- 6.3.3 Corden Pharma

- 6.3.4 Pfizer, Inc.

- 6.3.5 Sanofi - EUROAPI

- 6.3.6 SK Biotek

- 6.3.7 Sun Pharma

- 6.3.8 Teva

- 6.3.9 Thermo Fisher Scientific, Inc.

- 6.3.10 Viatris

- 6.3.11 Lonza

- 6.3.12 WuXi AppTec

- 6.3.13 Cambrex

- 6.3.14 Dishman Carbogen Amcis

- 6.3.15 Piramal Pharma Solutions

- 6.3.16 Sterling Pharma Solutions

- 6.3.17 Siegfried Holding

- 6.3.18 Evonik Health Care

- 6.3.19 Novasep (Seqens)

- 6.3.20 Delpharm

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment