PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064344

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064344

CT/NG Testing Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

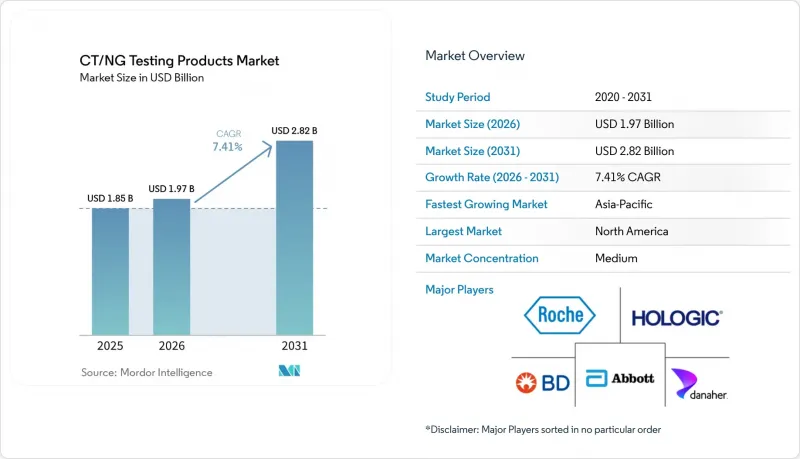

According to Mordor Intelligence, the CT/NG testing products market size is expected to increase from USD 1.85 billion in 2025 to USD 1.97 billion in 2026 and reach USD 2.82 billion by 2031, growing at a CAGR of 7.41% over 2026-2031.

This report is Segmented by Product (Assays & Kits, Instruments/Analyzers, Consumables & Accessories), Technology (NAAT [PCR, and More], Immunoassays, and More), End User (Central/Reference Laboratories, Hospital/Clinical Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global CT/NG Testing Products Market Trends and Insights

Routine Screening Mandates in Women Under 25 and High-Risk Groups

The CT/NG testing products market is supported by public health screening guidance that continues to widen testing among younger women and people with defined risk factors. Canada's Public Health Agency revised its guidance in April 2025 and reaffirmed annual universal CT/NG screening for individuals under 25, while also supporting repeat testing based on risk among those aged 25 and older. The Canadian Task Force on Preventive Health Care also recommends opportunistic screening up to age 30 for people who are not in high-risk groups, which broadens the addressable pool beyond the narrowest clinical risk definitions.

Kaiser Permanente Washington updated its approach through June 2025 and used opt-out extragenital screening questions in routine visits so providers can capture asymptomatic infections that standard discussions may miss. This makes testing less dependent on patient disclosure and increases the clinical value of broader specimen menus within the CT/NG testing products market. Quality frameworks such as CLIA in the United States and ISO 15189 in accredited laboratories also make these recommendations more practical to implement at scale because they support consistent workflows and result reliability.

Rapid NAAT and CLIA-Waived Point-of-Care Expansion

The CT/NG testing products market is gaining from rapid molecular platforms that reduce turnaround time from days to minutes and support treatment during the same visit. Roche received FDA 510(k) clearance and a CLIA waiver on January 21, 2025, for cobas liat CT/NG and CT/NG/MG assays that deliver PCR-quality results in 20 minutes with under 1 minute of hands-on time. These systems are being positioned for urgent care centers, retail clinics, and community health venues where same-visit diagnosis can reduce loss to follow-up.

A WHO-supported evaluation of Cepheid's GeneXpert Xpert CT/NG assay across Italy, Malta, and Peru enrolled 1,702 men who have sex with men and showed pooled sensitivity of 91.4% for NG in urine, specificity above 98% for CT and NG across all tested sites, and willingness among 96% of participants to wait for point-of-care results. Providers in the same study rated the instructions very clear or excellent in 79% of cases and reported optimal training times of 30 to 60 minutes, which shows that the CT/NG testing products market can expand beyond specialized laboratory staff. This combination of short hands-on time, acceptable workflow, and high willingness to wait supports continued movement of testing volumes toward decentralized care settings in the CT/NG testing products market.

EU IVDR Compliance Costs and Notified Body Bottlenecks

The CT/NG testing products market faces a clear drag in Europe from the In Vitro Diagnostic Regulation and the burden it creates for certification, recertification, and portfolio maintenance. Transition deadlines now run through December 2027 for Class D devices, December 2028 for Class C devices, and December 2029 for Class B and A-Sterile devices, which keeps compliance pressure elevated for several more years.

MedTech Europe reported in March 2025 that the administrative load under IVDR and MDR is heavy enough to redirect company resources away from innovation and toward regulatory upkeep. This matters for the CT/NG testing products market because sexual health menus often depend on multiplex claims, specimen-specific validation, and regular updates as guidelines change. When certification paths slow down, companies are less willing to expand panels or localize launches for Europe, especially if those products already have better commercial timing in the United States or Asia. The result is slower menu renewal, higher compliance cost per assay, and a tougher environment for smaller developers that do not have the same regulatory infrastructure as global incumbents in the CT/NG testing products market.

Other drivers and restraints analyzed in the detailed report include:

- Lab Automation and High-Throughput Platforms Lower Turnaround Time and Cost per Test

- AMR Surveillance Needs for NG Favor Precise Molecular Diagnostics

- Insufficient Evidence for Routine Screening in Men

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Assays and kits accounted for 73.8% of the CT/NG testing products market size in 2025 and are expected to expand at a 7.67% CAGR through 2031. This leadership reflects the way laboratories prefer reagent-rental arrangements that avoid upfront instrument purchases and shift capital risk to the supplier. BD's COR MX approach fits this pattern because hospitals commit to reagent volumes for CTGCTV2 assays in exchange for instrument placement, training, and service bundled into per-test pricing. Roche followed a similar model in decentralized settings, where cobas liat CT/NG and CT/NG/MG assays use closed single-use cartridges and allow molecular testing without dedicated batch preparation. That combination keeps assays and kits at the center of revenue generation in the CT/NG testing products market even when placement growth starts with instruments rather than consumables.

Instruments and analyzers are growing from a smaller base, but expansion in the CT/NG testing products industry still depends on rising menu breadth and automation intensity. Hitachi High-Tech's October 2025 installation at Seegene Medical Foundation Seoul showed how larger laboratories are scaling pre-processing and retesting capacity to absorb more complex molecular workloads. Consumables and accessories also benefit as self-collection becomes more accepted, because transport media, swabs, and specimen-handling materials gain volume when home or clinic self-swab workflows expand. The 2025 European guideline on chlamydia management stated that self-collected vulvo-vaginal, pharyngeal, and rectal specimens have similar diagnostic accuracy to clinician-collected samples for NAATs, which supports broader packaging of collection devices with simplified instructions. Across the CT/NG testing products market, this keeps product demand tied not only to instrument placements but also to how often patients are screened and how many anatomical sites are tested in the same episode.

Geography Analysis

North America held 38.47% of the CT/NG testing products market share in 2025, making it the largest regional contributor. The United States anchors this position because CDC guidance supports extragenital screening for men who have sex with men at 3 to 6 month intervals when they are on PrEP, living with HIV, or have multiple partners. Kaiser Permanente Washington reinforced that direction through its June 2025 opt-out screening workflow that asks patients whether any exposure sites should be excluded from routine STI testing. This kind of operational change lifts specimen volumes per patient and supports broader uptake across the CT/NG testing products market in North America. Canada also adds demand through updated 2025 guidance that reaffirmed annual universal CT/NG screening for people under 25 and targeted repeat screening in older groups based on risk.

Asia-Pacific is the fastest-growing regional block in the CT/NG testing products market, with an expected 8.13% CAGR through 2031. The China-Malaysia IVD mutual recognition arrangement became effective on July 30, 2025, and shortened approval timelines for qualifying Chinese products in Malaysia to 30 working days and for Malaysian products in China to 60 working days. Sansure also added a 6,100-square-meter research center and a 7,900-square-meter manufacturing base, which shows how regional suppliers are preparing for larger diagnostic demand. Australia strengthens the regional case from a surveillance standpoint, because 2024 data showed ceftriaxone decreased susceptibility in 0.5% of 10,702 isolates and supported the need for resistance-aware molecular diagnostics. Europe remains an important revenue base for the CT/NG testing products market, but it is operating under heavier regulatory pressure as MedTech Europe continues to report high administrative burden under IVDR and MDR.

The United Kingdom also remains clinically important because GRASP data to September 2025 showed rising resistance pressure, including 15 confirmed ceftriaxone-resistant cases in the first 8 months of 2025 and multiple extensively drug-resistant cases linked mainly to Asia-Pacific travel. Across continental Europe, Euro-GASP tested 3,579 isolates across 22 countries in 2024 and found tetracycline resistance of 62.3%, which keeps surveillance needs elevated. Middle East and Africa remain more fragmented, with stronger uptake in Gulf states that rely on centralized laboratory infrastructure and standardized procurement. South America is also growing from a smaller base, with adoption centered in larger urban systems and private clinic networks rather than broad nationwide testing saturation. Across both regions, the CT/NG testing products market still depends heavily on public procurement consistency, import conditions, and the ability of vendors to support decentralized testing where central laboratory access is uneven.

- Abbott Laboratories

- Beckton Dickinson

- bioMerieux

- Bioneer

- Danaher

- DiaSorin

- ELITechGroup S.p.A.

- GeneProof a.s.

- Hologic

- QIAGEN

- QuidelOrtho

- Randox Laboratories

- Roche

- Sansure Biotech Inc.

- SD BIOSENSOR, Inc.

- Seegene

- Thermo Fisher Scientific

- Visby Medical, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Routine Screening Mandates in Women Less Than 25 and High-Risk Groups

- 4.2.2 Rapid NAAT and CLIA-Waived Point-Of-Care Expansion

- 4.2.3 OTC At-Home CT/NG Testing Approvals Expand Access

- 4.2.4 Lab Automation and High-Throughput Platforms Lower TAT/Cost Per Test

- 4.2.5 Extragenital Screening Adoption Increases Tests Per Patient

- 4.2.6 AMR Surveillance Needs for NG Favor Precise Molecular Diagnostics

- 4.3 Market Restraints

- 4.3.1 EU IVDR Compliance Costs and Notified Body Bottlenecks

- 4.3.2 Insufficient Evidence for Routine Screening in Men (USPSTF I Statement)

- 4.3.3 Stigma/Privacy Barriers Still Limit Testing Uptake in Some Groups

- 4.3.4 LDT Restrictions and Migration to CE-IVD Reduce Menu Flexibility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Assays & Kits

- 5.1.2 Instruments/Analyzers

- 5.1.3 Consumables & Accessories

- 5.2 By Technology

- 5.2.1 NAAT

- 5.2.1.1 PCR

- 5.2.1.2 Transcription-Mediated Amplification

- 5.2.1.3 Isothermal amplification

- 5.2.2 Immunoassays

- 5.2.3 Culture / Other Methods

- 5.2.1 NAAT

- 5.3 By End User

- 5.3.1 Central/Reference Laboratories

- 5.3.2 Hospital/Clinical Laboratories

- 5.3.3 Point-of-Care Settings

- 5.3.4 At-Home / Remote Collection

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 bioMerieux SA

- 6.3.4 Bioneer Corporation

- 6.3.5 Danaher Corporation

- 6.3.6 DiaSorin

- 6.3.7 ELITechGroup S.p.A.

- 6.3.8 GeneProof a.s.

- 6.3.9 Hologic, Inc.

- 6.3.10 QIAGEN

- 6.3.11 QuidelOrtho Corporation

- 6.3.12 Randox Laboratories Ltd.

- 6.3.13 Roche Diagnostics

- 6.3.14 Sansure Biotech Inc.

- 6.3.15 SD BIOSENSOR, Inc.

- 6.3.16 Seegene Inc.

- 6.3.17 Thermo Fisher Scientific

- 6.3.18 Visby Medical, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment