PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064345

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064345

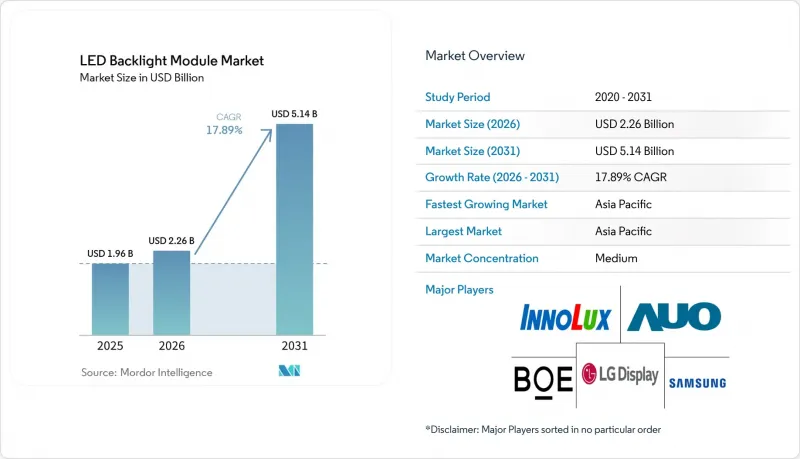

LED Backlight Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the lED backlight module market size is expected to increase from USD 1.96 billion in 2025 to USD 2.26 billion in 2026 and reach USD 5.14 billion by 2031, growing at a CAGR of 17.89% over 2026-2031.

This report is Segmented by Backlighting Technology (Edge-Lit LED Modules and Direct-Lit LED Modules), Panel Size (Small-Size Panels, Medium-Size Panels, and More), Application (Television, Monitor/Laptop, Smartphone/Tablet, Automotive Display, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Backlight Module Market Trends and Insights

Growing Penetration of Mini-LED Backlighting in Premium TVs

Samsung's Neo QLED and LG's QNED lineups now ship with 1,000-plus dimming-zone Mini-LED modules that deliver peak brightness beyond 1,500 nits and 100% DCI-P3 gamut. Retail price compression 65-inch sets selling below USD 1,000 in North America broadens adoption beyond early enthusiasts. Each Mini-LED backlight employs 5,000-25,000 chips, driving demand for advanced driver ICs with per-zone pulse-width modulation. The resulting bill-of-materials uplift underpins a multiyear revenue tailwind for direct-lit suppliers and accelerates the LED backlight module market's migration toward premium configurations.

Rising Demand for High-Brightness Automotive Displays

Electric-vehicle cockpit redesigns mandate 2,000-3,000 nit backlights for daytime readability. HARMAN's Ready Display platform integrates redundant LED strings and over 1,000 dimming zones to satisfy both ISO 15008 legibility and ISO 26262 functional-safety rules. Automotive tiers now pay 10-15% module premiums for this capability, locking in multiyear design wins and lifting average selling prices across the LED backlight module market.

Intensifying Competition from OLED and Micro-LED Displays

OLED panels dominate flagship smartphones and tablets priced above USD 800, displacing conventional backlights. Micro-LED pilots promise OLED-like contrast without organic degradation and could enter large-screen production once mass transfer yields stabilize. These self-emissive technologies siphon premium share, trimming the attainable ceiling for the LED backlight module market.

Other drivers and restraints analyzed in the detailed report include:

- Supply-Chain Localization Incentives in China and India

- Cost Advantages of Edge-Lit Architectures for Thin Notebooks

- IP Royalty Disputes Elevating BOM Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-lit Mini-LED modules are projected to post an 18.23% CAGR, reflecting rising adoption in televisions and gaming monitors. The LED backlight module market for edge-lit designs will expand more slowly, yet its lightweight profile and sub-USD 20 bill of materials keep it vital for notebooks and budget TVs. Manufacturers continue to refine dual-edge configurations and reflective cavities to defend share, but the contrast advantage of thousands of dimming zones positions Mini-LED as the long-term growth engine.

Production cost curves reinforce this split. Falling driver-IC prices and improved LED binning yields reduced Mini-LED television street prices from USD 3,000 in 2022 to nearly USD 1,200 in 2025. Conversely, edge-lit lines enjoy higher utilization and low capital intensity, enabling manufacturers to profit even as average selling prices decline, ensuring balanced growth across the LED backlight module market.

Geography Analysis

Asia Pacific contributed 67.82% of revenue in 2025 and is projected to sustain an 18.35% CAGR, underpinned by BOE, Tianma, and TCL CSOT expansions, as well as supportive incentives in China, Vietnam, and India. Localization programs reduce landed costs by exempting domestic sub-assemblies from import duties, driving internal investment into module integration lines. Capacity corridors in Guangdong and Jiangsu now combine LED epitaxy, phosphor synthesis, and quantum-dot film production, fortifying the regional supply chain.

North America and Europe collectively register outsized growth in automotive displays. Stricter power-consumption limits accelerate the transition to high-efficiency backlights across commercial signage and hospitality displays. Proposed reshoring projects, such as Japan Display's USD 13 billion fab in the United States, could diversify supply away from the Asia Pacific while maintaining momentum for the LED backlight module market.

South America, the Middle East, and Africa remain nascent, with local integrators assembling modules for retail signage and price-sensitive televisions. Volumes in these regions are insufficient to challenge Asia Pacific dominance, yet tariff barriers and regional content rules could spur incremental localized assembly over the forecast horizon.

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- Sharp Corporation

- Shenzhen Refond Optoelectronics Co., Ltd.

- Tianma Microelectronics Co., Ltd.

- Japan Display Inc.

- Rohinni LLC

- Radiant Opto-Electronics Corporation

- Lextar Electronics Corporation

- Winstar Display Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Penetration of Mini-LED Backlighting in Premium TVs

- 4.2.2 Rising Demand for High-Brightness Automotive Displays

- 4.2.3 Cost Advantages of Edge-Lit Architectures for Thin Notebooks

- 4.2.4 Supply-Chain Localisation Incentives in China and India

- 4.2.5 Energy-Efficiency Regulations Favouring LED Backlight Retrofits

- 4.2.6 Integration of Quantum-Dot Enhancement Films in LCD Panels

- 4.3 Market Restraints

- 4.3.1 Intensifying Competition from OLED and Micro-LED Displays

- 4.3.2 IP Royalty Disputes Elevating BOM Costs

- 4.3.3 Supply Volatility of High-Performance Phosphors

- 4.3.4 Environmental Scrutiny on Rare-Earth Extraction

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Backlighting Technology

- 5.1.1 Edge-lit LED Modules

- 5.1.2 Direct-lit LED Modules (Full Array / Mini-LED)

- 5.2 By Panel Size

- 5.2.1 Small-size Panels (Less Than or Equal To 10 inches)

- 5.2.2 Medium-size Panels (Less Than 10 to Greater Than or Equal to 32 inches)

- 5.2.3 Large-size Panels (Less Than 32 inches)

- 5.3 By Application

- 5.3.1 Television (TV) Backlight Modules

- 5.3.2 Monitor / Laptop Backlight Modules

- 5.3.3 Smartphone / Tablet Backlight Modules

- 5.3.4 Automotive Display Backlight Modules

- 5.3.5 Other Application - Display Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Display Co., Ltd.

- 6.4.3 BOE Technology Group Co., Ltd.

- 6.4.4 AU Optronics Corp.

- 6.4.5 Innolux Corporation

- 6.4.6 Sharp Corporation

- 6.4.7 Shenzhen Refond Optoelectronics Co., Ltd.

- 6.4.8 Tianma Microelectronics Co., Ltd.

- 6.4.9 Japan Display Inc.

- 6.4.10 Rohinni LLC

- 6.4.11 Radiant Opto-Electronics Corporation

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 Winstar Display Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment