PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064358

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064358

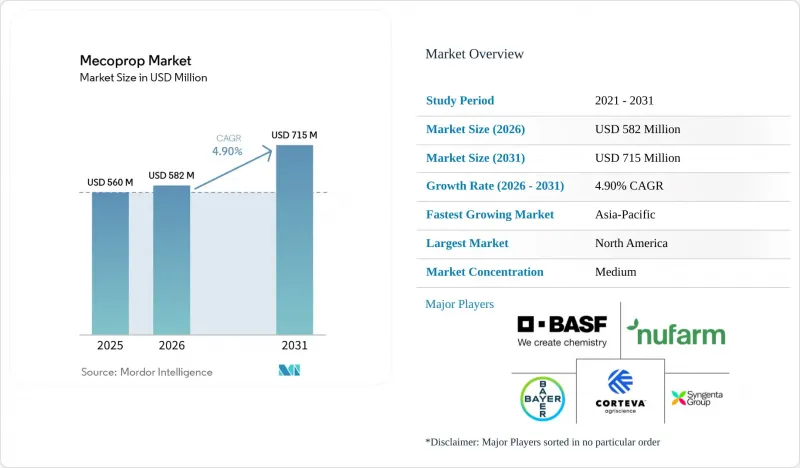

Mecoprop - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the mecoprop market size was valued at USD 560 million in 2025 and estimated to grow from USD 582 million in 2026 to reach USD 715 million by 2031, at a CAGR of 4.9% during the forecast period (2026-2031).

This report is Segmented by Product Type (Mecoprop-P Technical, and Mecoprop-P Formulated Products), by Formulation (Emulsifiable Concentrate (EC), and More), by Crop/Application (Turf and Ornamentals, and More), by Distribution Channel (Direct Sales To Distributors, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD)

Global Mecoprop Market Trends and Insights

Expanding Bans on Glyphosate Pushing Turf Managers Toward Selective Phenoxy Herbicides

Municipal limitations on glyphosate have accelerated substitution toward phenoxy herbicides in golf courses, sports fields, and municipal parks. Turf managers increasingly adopt three-way mixes of 2,4-D, dicamba, and Mecoprop-P to maintain broadleaf control without depending on non-selective burndown programs. Health Canada renewed multiple Mecoprop-P combinations in 2025, keeping professional and residential label uses open. Extension guides in the Pacific Northwest recommend broadcast rates of 0.75 pound acid equivalent per acre, highlighting Mecoprop-P's safety on fine bentgrass. Ongoing United States policy reviews of glyphosate supply reliability reinforce the shift, ensuring steady demand for phenoxy alternatives through 2031. The trend provides a durable tailwind for the mecoprop market across mature and emerging regions.

Regulatory Approvals of Mecoprop-P Enantiomer with Lower Toxicity Profile

Fast-track registrations for single-enantiomer Mecoprop-P reduce mammalian toxicity and environmental persistence relative to racemic mixtures, unlocking new consumer and professional applications. Health Canada cleared several new or renewed dossiers in 2025, signaling confidence in the R-enantiomer's safety profile. The University of Hertfordshire database still flags racemic Mecoprop-sodium as posing reproductive hazards, underscoring the advantage of purified material. Manufacturers with enantiomer-specific synthesis capacity are gaining regulatory preference, consolidating market share in high-value turf segments. Lower hazard ratings open distribution in jurisdictions that previously restricted phenoxy use, such as several European municipalities. As approvals spread, demand for Mecoprop-P formulations will support stable volume growth and improved pricing power during 2026-2031.

Stringent Maximum Residue Limits for Phenoxy Acids in Food Crops

Food-safety regulators in Europe and North America enforce lower residue tolerances that restrict phenoxy applications in cereals, oilseeds, and forage. Extension guides list long preharvest intervals for 2,4-D and related mixtures, highlighting compliance challenges. Export-oriented growers face shipment rejection if residues exceed destination limits, prompting avoidance of Mecoprop in edible rotations. The University of Hertfordshire database continues to flag reproductive hazards for certain salts, adding regulatory pressure for tighter oversight. As scrutiny mounts, demand migrates from food crops to turf, ornamentals, and industrial vegetation management, potentially trimming mecoprop market growth.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Professional Turf and Lawn Care Services in Urbanizing Economies

- Integration of Herbicide-Tolerant Seed Coatings Enabling Combined Pre and Post Emergence Control

- Emerging Resistance in Broadleaf Weeds is Reducing Field Efficacy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mecoprop-P formulated products generated the largest 56% share of mecoprop market size in 2025 as contractors and homeowners preferred the ready-to-spray ease of use. Technical concentrates serve toll formulators and experienced distributors and are projected to grow at the fastest 7.7% CAGR during 2026-2031, propelled by rising generic output in China and India. Regulatory pathways, such as United States conditional registrations, allow new technical imports once data call-ins are met. Growing concentrate availability boosts local formulation in price-sensitive regions. Consequently, formulated products will retain the bulk of the mecoprop market, while concentrates expand their reach into emerging economies.

Technical material buyers benefit from flexible blending that tailors solvent choice, adjuvants, and packaging to local agronomic needs. Asian formulators often down-pack into one-liter bottles that align with the purchasing power of smallholders. Larger distributors in South America prefer drum imports that feed automated filling lines for regional brands. As phytotoxicity data accumulate for Mecoprop-P alone and in mixes, demand for concentrates should strengthen. The interplay between premium branded formulations and cost-efficient generics will shape future mecoprop market dynamics.

Emulsifiable concentrates maintained the largest 40% mecoprop market share in 2025 because professional applicators value tank-mix flexibility and equipment compatibility. Soluble concentrates followed due to higher active loading and lighter packaging. Ready-to-use aerosols are forecast for the fastest 8.4% CAGR from 2026-2031, supported by DIY merchandising, low-volatility salts, and built-in drift guards. Granular formulations serve niche lawn segments where combined fertilizer and weed control provide season-long benefit. Continued innovation in emulsifiable technology, such as built-in safeners, maintains relevance in broadacre cereals facing resistant weeds.

Consumer convenience dictates aerosol growth as homeowners seek grab-and-go weed solutions without measuring. Retail planograms place aerosols near sprinkler gear and grass seed to capture impulse traffic. Manufacturers reformulate to reduce odor and staining, increasing acceptance among suburban households. Water-based, soluble concentrates appeal to parks departments seeking to reduce solvent emissions. Segment diversity ensures steady demand and balances the overall mecoprop market size against evolving user preferences.

Geography Analysis

North America held the largest 31% share of the mecoprop market in 2025, driven by extensive use on golf courses, sports fields, and residential lawns. Growth is forecast to be at a descent CAGR during 2026-2031, as mature demand is offset by stricter municipal pesticide bylaws and rising organic preferences. United States policy discussions on glyphosate supply encourage diversification into phenoxy mixes, underpinning baseline Mecoprop demand. Canada maintains a streamlined registration process, renewing multiple Mecoprop-P products in 2025 to ensure continued supply. Resistance emergence in waterhemp and kochia underscores the need for integrated management, but phenoxy herbicides remain a critical tool.

Asia-Pacific is the fastest-growing regional market, with a 8.6% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and expanding e-commerce distribution. China dominates technical production and exports, while India and Southeast Asian nations add residential lawn adoption. BASF SE and Corteva Agriscience introduced the Clearfield Mustard production system in India in 2026, showcasing the corporate focus on trait packages that can be transferred to turf and specialty crops. Australia's golf and sports turf sector continues to invest in selective herbicides to manage resistant broadleaf weeds, sustaining Mecoprop volume. Regional governments fund park construction and greening projects, thereby increasing demand for professional turf services.

Europe accounted for a significant share of 2025 sales and is projected to grow at descent CAGR during 2026-2031, given regulatory tightness and rising organic lawn care. Nufarm Ltd.'s Wyke facility delivered volume gains in 2025 but faced margin pressure from low phenoxy prices. Herbicide resistance surveys in Ireland and the United Kingdom highlight the spread of ALS and ACCase resistance, prompting renewed interest in multi-mode mixes that include phenoxy actives. Germany and France sustain agricultural use in cereals and oilseeds, while the United Kingdom depends on turf and amenity markets. Eastern Europe shows steady demand from broadacre grains, although geopolitical uncertainties influence spending patterns.

- BASF SE

- Corteva Agriscience

- Bayer AG

- Nufarm Limited

- Syngenta Crop Protection AG

- Albaugh, LLC

- FMC Corporation

- UPL Limited

- Jiangsu Jiangnan Agrochemical Co., Ltd.

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- Shandong Rainbow Agro Co., Ltd.

- Nutrien Ltd.

- HELM AG

- Valent U.S.A. LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding bans on glyphosate pushing turf managers toward selective phenoxy herbicides

- 4.2.2 Regulatory approvals of Mecoprop-P enantiomer with lower toxicity profile

- 4.2.3 Growth of professional turf and lawn care services in urbanizing economies

- 4.2.4 Integration of herbicide-tolerant seed coatings enabling combined pre and post emergence control

- 4.2.5 Rising adoption of ready-to-use consumer lawn weed control products in DIY retail

- 4.2.6 Rapid growth of online agrochemical marketplaces boosting distribution reach in developing nations

- 4.3 Market Restraints

- 4.3.1 Stringent maximum residue limits for phenoxy acids in food crops

- 4.3.2 Emerging resistance in broadleaf weeds is reducing field efficacy

- 4.3.3 Price volatility of key feedstock 2,4-Dichlorophenol is impacting production cost

- 4.3.4 Increasing shift toward organic lawn and landscape management

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Mecoprop-P Technical

- 5.1.2 Mecoprop-P Formulated Products

- 5.2 By Formulation

- 5.2.1 Emulsifiable Concentrate (EC)

- 5.2.2 Soluble Concentrate (SL)

- 5.2.3 Granular Formulations

- 5.2.4 Ready-to-Use Aerosols

- 5.3 By Crop/Application

- 5.3.1 Turf and Ornamentals

- 5.3.2 Cereals and Pulses

- 5.3.3 Residential Lawns and Gardens

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales to Distributors

- 5.4.2 Online Agrochemical Platforms

- 5.4.3 Retail Garden Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Corteva Agriscience

- 6.4.3 Bayer AG

- 6.4.4 Nufarm Limited

- 6.4.5 Syngenta Crop Protection AG

- 6.4.6 Albaugh, LLC

- 6.4.7 FMC Corporation

- 6.4.8 UPL Limited

- 6.4.9 Jiangsu Jiangnan Agrochemical Co., Ltd.

- 6.4.10 Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- 6.4.11 Shandong Rainbow Agro Co., Ltd.

- 6.4.12 Nutrien Ltd.

- 6.4.13 HELM AG

- 6.4.14 Valent U.S.A. LLC

7 Market Opportunities and Future Outlook