PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064412

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064412

South America Oil And Gas Drone Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

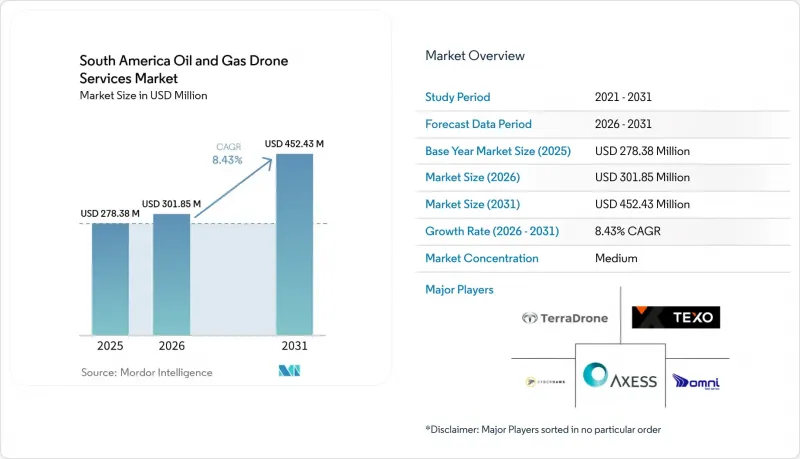

According to Mordor Intelligence, the south america oil and gas drone services market size is projected to expand from USD 278.38 million in 2025 and USD 301.85 million in 2026 to USD 452.43 million by 2031, registering a CAGR of 8.43% between 2026 to 2031.

This report is Segmented by Service Type (Inspection & Monitoring, Surveying & Mapping, Emergency Response & Environmental Monitoring, and Logistics Support), Application (Pipeline Monitoring & Integrity, and More), Drone Type (Multi-Rotor, and More), and Geography (Brazil, Argentina, Guyana, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Oil And Gas Drone Services Market Trends and Insights

Cost and Safety Economics Are Reframing the Total Value Proposition

The South America oil and gas drone services market is seeing stronger adoption because operators are treating drone inspection as a safer and more repeatable alternative to confined-space entry, rope access, and other labor-heavy methods. This shift is especially visible in Brazil, where Transpetro reported savings of up to BRL 1 million, or USD 171,000, per tanker inspection cycle after moving to drone-based confined-space surveys, while inspection time fell from 1 week to 3 to 4 days. The commercial effect is important because once inspection moves into routine operating budgets, procurement becomes steadier and contract renewals become easier to justify. The South America oil and gas drone services market is also supported by growing comfort with drone-generated inspection data in formal survey environments, which reduces resistance from operators that previously viewed drone use as a pilot activity rather than a core process . This combination of lower field exposure, shorter downtime, and clearer documentation is helping drone services move into long-cycle maintenance programs.

Pipeline and Critical Asset Integrity Requirements Drive Long-Cycle Contracts

The South America oil and gas drone services market continues to gain from the region's large network of pipelines, terminals, storage systems, and offshore transfer assets that need regular visual and thermal review. Operators are placing more value on documented inspection history because asset failures now carry operational, financial, and reputational consequences well beyond the repair itself. That is especially relevant in remote corridors, where weather, terrain, and access limits make manual inspection slower and less consistent. In this setting, drone services are becoming part of integrity management programs rather than one-off field jobs, which supports longer contract duration and more frequent repeat work. The South America oil and gas drone services market therefore benefits not only from the need to inspect assets, but also from the need to preserve an auditable inspection trail across distributed infrastructure.

Fragmented BVLOS Frameworks and Aviation Approval Overhead

The South America oil and gas drone services market still faces a major scaling challenge because operators must navigate separate drone approval systems across national borders. Brazil's ANAC opened Public Consultation No. 09 in June 2025 and proposed RBAC 100, which shifts regulation toward a risk-based system with Open, Specific, and Certified categories and introduces a Specific Category operating framework tied to risk assessment methods such as SORA . Argentina also issued Resolution 550/2025 and moved to RAAC 100, 101, and 102, replacing its older class-based system with Open, Specific, and Certified categories aligned with ICAO and Latin American Aeronautical Regulations. Even with that progress, BVLOS missions in the Specific Category still require operational approvals and supporting risk mitigation, which adds lead time and raises deployment cost for cross-border corridor work. The South America oil and gas drone services market therefore favors firms with local entities, local compliance experience, and the ability to absorb country-specific approval delays.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Multi-Sensor Payloads Extend Inspection Scope Per Flight

- Offshore Brazil and Guyana Development Expanding Remote Inspection Demand

- Environmental and Infrastructure Limitations at the Operating Edge

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inspection and Monitoring retained a 41.8% share in 2025, which kept it as the largest service type in the South America oil and gas drone services market. The segment leads because it addresses the region's most immediate need, which is frequent review of pipelines, tanks, flare stacks, offshore structures, and other integrity-sensitive assets. Its position is strongest in Brazil, where offshore maintenance programs and tanker inspections already support routine use of drone-based visual review and confined-space access. Formal acceptance of drone-based ultrasonic thickness workflows also strengthens this service line because it makes drone output more usable in recognized inspection and survey settings.

Surveying and Mapping is projected to expand at a 9.8% CAGR from 2026 to 2031, making it the fastest-growing service type in the South America oil and gas drone services industry. Growth is being supported by new route studies, pre-construction planning, right-of-way mapping, and digital twin development across emerging and expanding oil and gas projects. Emergency Response and Environmental Monitoring is also rising as emissions control and leak traceability become more regular contractual needs rather than occasional field exercises. In the South America oil and gas drone services industry, Logistics Support remains the smallest segment because payload limits and operating approvals still restrict routine cargo missions in controlled or complex airspace.

List of Companies Covered in this Report:

- Cyberhawk Innovations Limited

- Terra Drone Corporation

- OMNI Taxi Aereo

- TEXO DSI

- Axess GLASS Inc.

- SkyX Systems Corp.

- DATUM Ingenieria SAS

- DR1 Technology Solutions

- Aurora Data

- Uali

- Terra Vision

- Fugro

- Saipem

- Percepto

- Flyability

- Voliro

- Intertek

- GuyDrones

- DronesSkycam

- Aerodyne Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Market Definition

- 1.3 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends and Developments

- 4.3 Market Drivers

- 4.3.1 Cost and safety gains versus scaffolding, rope access, and helicopters

- 4.3.2 Rising pipeline and critical asset integrity requirements

- 4.3.3 AI-enabled thermal, LiDAR, OGI, and digital twin inspection workflows

- 4.3.4 Offshore Brazil and Guyana development expanding remote inspection demand

- 4.3.5 Vaca Muerta methane-monitoring demand

- 4.3.6 Remote pipeline-right-of-way surveillance in hard-to-access corridors

- 4.4 Market Restraints

- 4.4.1 Fragmented aviation approvals and BVLOS constraints

- 4.4.2 Weather, salt spray, wind, and GPS-denied operating conditions

- 4.4.3 Sparse digital maintenance backbones at regional operators

- 4.4.4 Critical-infrastructure data sovereignty and security sensitivity

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Inspection & Monitoring

- 5.1.2 Surveying & Mapping

- 5.1.3 Emergency Response & Environmental Monitoring

- 5.1.4 Logistics Support

- 5.2 By Application

- 5.2.1 Pipeline Monitoring & Integrity

- 5.2.2 Offshore Platforms & FPSOs

- 5.2.3 Refineries & Petrochemical Facilities

- 5.2.4 Exploration, Construction & ROW Survey

- 5.2.5 Emissions, Spill & ESG Monitoring

- 5.3 By Drone Type

- 5.3.1 Multi-rotor Drones

- 5.3.2 Fixed-wing Drones

- 5.3.3 Hybrid VTOL Drones

- 5.3.4 Confined-space / Indoor Drones

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Guyana

- 5.4.4 Colombia

- 5.4.5 Ecuador

- 5.4.6 Peru

- 5.4.7 Chile

- 5.4.8 Venezuela

- 5.4.9 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Cyberhawk Innovations Limited

- 6.4.2 Terra Drone Corporation

- 6.4.3 OMNI Taxi Aereo

- 6.4.4 TEXO DSI

- 6.4.5 Axess GLASS Inc.

- 6.4.6 SkyX Systems Corp.

- 6.4.7 DATUM Ingenieria SAS

- 6.4.8 DR1 Technology Solutions

- 6.4.9 Aurora Data

- 6.4.10 Uali

- 6.4.11 Terra Vision

- 6.4.12 Fugro

- 6.4.13 Saipem

- 6.4.14 Percepto

- 6.4.15 Flyability

- 6.4.16 Voliro

- 6.4.17 Intertek

- 6.4.18 GuyDrones

- 6.4.19 DronesSkycam

- 6.4.20 Aerodyne Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment