PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064429

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064429

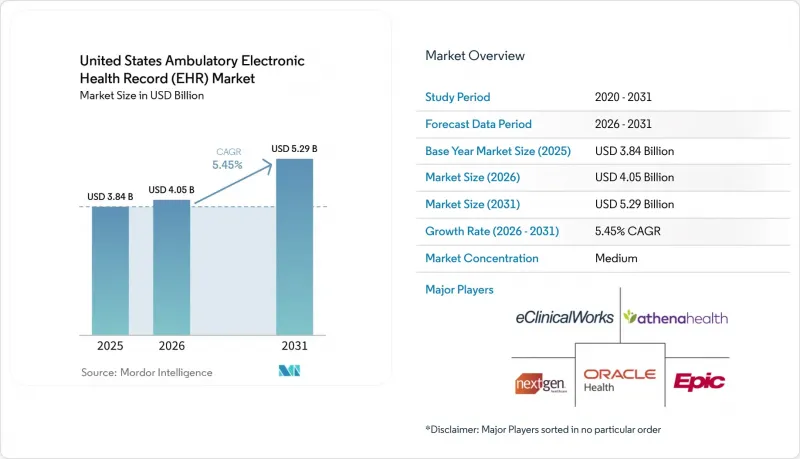

United States Ambulatory Electronic Health Record (EHR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states ambulatory electronic health record (EHR) market size is expected to grow from USD 3.84 billion in 2025 to USD 4.05 billion in 2026 and is forecast to reach USD 5.29 billion by 2031 at 5.45% CAGR over 2026-2031.

This report is Segmented by Delivery Mode (Cloud-Based, On-Premise, Hybrid), Functionality (Practice Management, Patient Management, E-Prescribing, Referral Management, and More), Practice Size (Small, Mid-Size, Large Group), and Ownership (Hospital-Owned, Health-System Affiliated, Independent Ambulatory Centers). Forecasts are Provided in Terms of Value (USD).

United States Ambulatory Electronic Health Record (EHR) Market Trends and Insights

Outpatient Care Shift and ASC Expansion Drive Structural Demand

The United States ambulatory EHR software market is gaining durable support from the continued shift of surgery into outpatient settings. A 2026 Penn LDI research update, based on a study in Medical Care Research and Review, found that outpatient surgery grew 6% annually after the pandemic and that more than 65% of surgeries were already being performed outside inpatient settings. MedPAC reports in March 2026 that Medicare-certified ASCs increased 2.2% to 6,436 facilities in 2024 and that ASC procedures per fee-for-service Medicare beneficiary rose 3.5% in the same year. CMS is reinforcing that shift by removing 285 procedures from the inpatient-only list for 2026 and adding 271 procedures to the ASC covered list, which expands the outpatient case mix that ambulatory records systems must support. MedPAC also shows faster procedure growth in orthopedics, cardiology, and multispecialty pain management, which raises the need for specialty-specific documentation, scheduling, and authorization workflows inside the United States ambulatory EHR software market.

Cloud-Native Replacement Cycle Reshapes Vendor Economics

The United States ambulatory EHR software market is also being reshaped by an active migration away from legacy on-premise systems. The ONC HTI-1 final rule requires certified health IT to support USCDI v3 through FHIR US Core profiles, which makes modern API support a basic product requirement rather than an optional enhancement. Cloud architectures are better aligned with recurring standards updates because they can push interoperability and compliance changes without the slower local upgrade cycle common in older deployments. Oracle Health reinforces that direction with its OCI-native ambulatory EHR and Clinical AI Agent, which connect new AI functionality directly to cloud infrastructure choices. As data portability becomes a compliance expectation, switching friction should keep easing and replacement activity should continue to move through the United States ambulatory EHR software market.

Cybersecurity And Outage Exposure Slow Cloud Adoption Among At-Risk Segments

Cybersecurity remains the clearest operating restraint in the United States ambulatory EHR software market. IBM reports that the average healthcare breach cost reached USD 7.42 million in 2025 and that the average breach lifecycle extended to 279 days, which kept healthcare as the costliest sector for the 14th consecutive year. A July 2025 study in JAMA Network Open found that 34% of Epic-using hospitals experienced detectable service disruption during the July 2024 CrowdStrike outage, including interruptions tied to scheduling, lab results, prescription refills, and secure messaging. These events show that risk does not stop with ransomware and also includes wider infrastructure and third-party failures that can interrupt basic ambulatory operations. Smaller and independent providers will therefore keep assessing vendors through a strong security lens, which can slow replacement timing inside the United States ambulatory EHR software market.

Other drivers and restraints analyzed in the detailed report include:

- Value-Based Care Reporting Pressure Drives Certified EHR Upgrades

- Ambient AI Embeds Into EHR Workflows At A Sector-Defining Pace

- High Implementation And Migration Costs Persist As A Barrier

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions held 84.3% of the United States ambulatory EHR software market size in 2025 and are projected to grow at a 6.4% CAGR through 2031. That lead shows the replacement cycle is still active rather than complete. Cloud delivery is gaining support because it makes regulatory updates, interoperability changes, and recurring software releases easier to manage across distributed ambulatory sites. The ONC HTI-1 rule and the CMS prior authorization framework both favor platforms that can deliver FHIR-based exchange as a routine product function instead of a major local project. This gives cloud vendors a practical advantage when buyers weigh compliance risk against aging technology debt.

The United States ambulatory EHR software market still keeps a smaller on-premise base among academic groups, research-linked settings, and organizations with long legacy contract cycles. Some larger systems will continue using hybrid designs where core records remain tightly governed while analytics, interoperability layers, or AI tools shift into hosted environments. Even so, AI capability is moving closer to cloud infrastructure, and Oracle Health makes that link clear through its OCI-native ambulatory EHR roadmap. As a result, cloud growth should remain broad across practice tiers, while on-premise demand is more likely to come from delayed replacement than from fresh expansion. In the ambulatory EHR software industry, delivery choices now depend on compliance readiness and automation access as much as on hosting preference.

Practice management held 22.2% share in 2025, which made it the largest functionality block in the United States ambulatory EHR software market. That position reflects the daily role of scheduling, billing, coding support, and claims follow-up in outpatient economics. Ambulatory providers still treat these tools as the first defense against revenue leakage because front-office errors and denial issues affect cash flow quickly. The segment also benefits from the rise of ASCs and multi-site outpatient groups, which need consistent administrative routines across locations. This keeps practice management central even as more advanced clinical and AI functions expand.

Patient management is projected to grow at a 6.5% CAGR through 2031, the fastest rate among functionality segments in the United States ambulatory EHR software market. Growth is tied to stronger quality reporting demands, population health tracking, and the need to close care gaps within value-based contracts. The 2026 Physician Fee Schedule rule and ongoing Promoting Interoperability requirements make more consistent data capture unavoidable for ACO-aligned ambulatory practices. Referral management and e-prescribing should remain important because compliance and care coordination both depend on clean data moving across the ambulatory workflow. The ambulatory EHR software industry is therefore shifting toward platforms that combine financial, clinical, and reporting functions within one connected record.

List of Companies Covered in this Report:

- AdvancedMD

- Athenahealth

- Azalea Health Innovations, Inc.

- CompuGroup Medical US

- CureMD Healthcare

- DrChrono by EverHealth

- eClinicalWorks

- Elation Health, Inc.

- Epic Systems

- Greenway Health

- Infor-Med, Inc. (Praxis EMR)

- Medical Information Technology, Inc. (MEDITECH)

- Modernizing Medicine, Inc. (ModMed)

- Nextech Systems, LLC

- NextGen Healthcare

- Oracle Health

- Practice Fusion, Inc.

- Tebra Technologies, Inc.

- Veradigm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outpatient Care Shift and ASC Expansion

- 4.2.2 Cloud-Native Replacement Cycle

- 4.2.3 Value-Based Care Reporting Pressure

- 4.2.4 Ambient AI and Specialty Workflow Upgrades

- 4.2.5 Prior-Authorization API Readiness

- 4.2.6 FHIR, USCDI, and TEFCA Interoperability Refresh

- 4.3 Market Restraints

- 4.3.1 Cybersecurity and Outage Exposure

- 4.3.2 High Implementation and Migration Costs

- 4.3.3 Workflow Disruption and Staff Training Burden

- 4.3.4 API Monetization and Integration Overages

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Delivery Mode

- 5.1.1 Cloud-based Solutions

- 5.1.2 On-premise Solutions

- 5.1.3 Hybrid Solutions

- 5.2 By Functionality

- 5.2.1 Practice Management

- 5.2.2 Patient Management

- 5.2.3 E-Prescribing

- 5.2.4 Referral Management

- 5.2.5 Population Health Management

- 5.2.6 Others

- 5.3 By Practice Size

- 5.3.1 Small Group Practices

- 5.3.2 Mid-size Group Practices

- 5.3.3 Large Group Practices

- 5.4 By Ownership

- 5.4.1 Hospital-owned Ambulatory Centers

- 5.4.2 Health-system Affiliated Physician Groups

- 5.4.3 Independent Ambulatory Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AdvancedMD, Inc.

- 6.3.2 athenahealth, Inc.

- 6.3.3 Azalea Health Innovations, Inc.

- 6.3.4 CompuGroup Medical US

- 6.3.5 CureMD Healthcare

- 6.3.6 DrChrono by EverHealth

- 6.3.7 eClinicalWorks, LLC

- 6.3.8 Elation Health, Inc.

- 6.3.9 Epic Systems Corporation

- 6.3.10 Greenway Health, LLC

- 6.3.11 Infor-Med, Inc. (Praxis EMR)

- 6.3.12 Medical Information Technology, Inc. (MEDITECH)

- 6.3.13 Modernizing Medicine, Inc. (ModMed)

- 6.3.14 Nextech Systems, LLC

- 6.3.15 NextGen Healthcare, Inc.

- 6.3.16 Oracle Health

- 6.3.17 Practice Fusion, Inc.

- 6.3.18 Tebra Technologies, Inc.

- 6.3.19 Veradigm LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment