PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064430

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064430

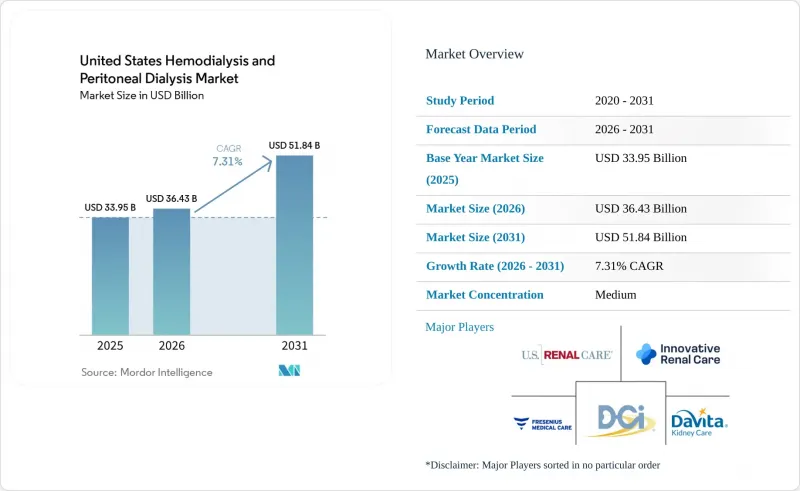

United States Hemodialysis And Peritoneal Dialysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states hemodialysis and peritoneal dialysis market size was valued at USD 33.95 billion in 2025 and is estimated to grow from USD 36.43 billion in 2026 to reach USD 51.84 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

This report is Segmented by Modality (Hemodialysis, Peritoneal Dialysis), Product and Service (Devices, Consumables, Services), Disease Indication (End-Stage Kidney Disease, Acute Kidney Injury), and End-Use Setting (Freestanding Centers, Hospital-Based Centers, Home Care, Skilled Nursing and Long-Term Care). The Market Forecasts are Provided in Terms of Value (USD).

United States Hemodialysis And Peritoneal Dialysis Market Trends and Insights

Rising ESKD Burden from Diabetes and Hypertension

Diabetic nephropathy and hypertensive renal disease continue to feed the core treatment pipeline for the US hemodialysis and peritoneal dialysis market. The United States recorded 135,000 new ESKD cases in 2025, and CKD affected 15% of U.S. adults, which leaves a large upstream pool at risk of progression into long-duration dialysis care. Incident ESKD among Black Americans runs at 3.8 times the rate seen among White Americans, and the heaviest burden remains concentrated in states with weaker chronic disease management capacity. That racial and regional concentration means the US hemodialysis and peritoneal dialysis market continues to expand even when providers add transplant referrals or improve screening. The emerging benefit from GLP-1 therapies is real, but Fresenius still framed that effect as a long-range factor rather than a near-term volume reset for 2026 through 2031.

Home Dialysis Adoption and Reimbursement Support

CMS widened support for home treatment when it extended Medicare payment for dialysis in the home setting to beneficiaries with acute kidney injury beginning January 1, 2025. The rule also allowed ESRD facilities to bill the home and self-dialysis training add-on payment for AKI beneficiaries, and the training add-on was set at USD 95.6 per session in the final rule. Vantive linked its Sharesource remote monitoring platform with lower all-cause mortality and fewer hospitalizations, which broadens the case for home modalities beyond patient convenience alone. CMS also expanded TPNIES eligibility to certain home dialysis machines and set payment at 65% of the MAC-determined pre-adjusted price, reduced by a USD 9.32 offset, for 2 calendar years. Together, those changes lower adoption friction and support a larger installed base for the US hemodialysis and peritoneal dialysis market in home settings.

Reimbursement-Cost Mismatch for Providers

The 2026 ESRD PPS base rate was finalized at USD 281.7 per treatment, which was a 2.2% increase from 2025. DaVita reported patient care costs per treatment of USD 273.3 in 2025 and USD 280.1 in the first quarter of 2026, which shows how quickly provider costs moved toward the reimbursement ceiling. This pressure is harder for independent freestanding centers because they do not have the same purchasing leverage, balance sheet strength, or vertical supply integration as the largest operators. Fresenius also highlighted projected Medicaid funding cuts through 2034 as a secondary risk for centers that serve dually eligible patients in greater proportions. If that mismatch persists, the US hemodialysis and peritoneal dialysis market could see slower investment in new equipment, tighter center economics, and a faster gap between national chains and smaller providers.

Other drivers and restraints analyzed in the detailed report include:

- Kidney Transplant Shortage Sustaining Dialysis Demand

- Connected Dialysis and Therapy Upgrade Cycle

- Nephrology Nursing and Technician Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hemodialysis held 88.31% of the US hemodialysis and peritoneal dialysis market share in 2025, which reflects the installed clinical base, long-standing physician familiarity, and payer workflows built around in-center treatment. The modality also remains central to equipment replacement because Fresenius began commercial rollout of the 5008X CAREsystem in the United States after FDA clearance in May 2025. Fresenius is converting 20% of its U.S. installed base in 2026 and aims to replace the full installed base with the 5008X by the end of 2030, which keeps hemodialysis clinically current rather than operationally static. That matters because high-volume hemodiafiltration gives the hemodialysis segment a clinical upgrade path at the same time that providers face pressure to improve outcomes and staffing efficiency.

Peritoneal dialysis remains the smaller modality, but its 8.38% CAGR makes it the faster-moving part of the US hemodialysis and peritoneal dialysis industry through 2031. The shift is supported by home treatment policy, remote monitoring, and the practical need to move appropriate patients away from fixed in-center schedules. CMS strengthened that direction by extending home dialysis payment to AKI beneficiaries and by continuing support mechanisms for home equipment through TPNIES. Vantive also said Sharesource has supported more than 100 million home dialysis treatments globally, which shows how remote patient management is moving from a helpful feature to a routine care tool. The CMS update to Kt/V adequacy measures for payment year 2027 adds separate reporting expectations for HD and PD, which means modality growth in the US hemodialysis and peritoneal dialysis market now sits alongside tighter performance visibility.

Services accounted for 68.24% of revenue in 2025, so the largest share of the US hemodialysis and peritoneal dialysis market still comes from treatment delivery rather than device sales. That structure favors large operators because scale supports billing, labor deployment, and payer contracting across thousands of treatment sites. DaVita reported average revenue per treatment of USD 417.6 in the first quarter of 2026, which shows that service revenue remains the core earnings driver even in a cost-sensitive environment. The service-heavy mix also explains why provider strategy in the US hemodialysis and peritoneal dialysis market increasingly focuses on center productivity, patient retention, and risk-based care management rather than simple unit expansion.

Consumables are the faster-growth layer, with the US hemodialysis and peritoneal dialysis market size for consumables projected to expand at 8.52% CAGR through 2031. That growth comes from recurring treatment use, especially as home schedules can require more frequent sessions than the standard in-center pattern. Outset reported that consumables and services made up 70% of revenue in the first quarter of 2026, which shows how installed-base monetization is becoming a major commercial lever. Rockwell reinforced that theme when it launched a single-use bicarbonate cartridge in February 2025 to target a USD 100 million disposables sub-market. Devices still matter because connected HDF and home-capable platforms create multi-year replacement demand, but the margin logic in the US hemodialysis and peritoneal dialysis industry is moving more clearly toward recurring supplies and associated services.

List of Companies Covered in this Report:

- B. Braun

- DaVita

- Dialysis Clinic, Inc.

- Dialyze Direct

- Fresenius Medical Care AG

- Innovative Renal Care

- Merit Medical Systems

- Mozarc Medical

- Nikkiso Medical America, Inc.

- Nipro

- Northwest Kidney Centers

- Outset Medical, Inc.

- Quanta Dialysis Technologies

- Rockwell Medical

- Satellite Healthcare

- The Rogosin Institute

- U.S. Renal Care, Inc.

- Vantive Health LLC

- W. L. Gore & Associates

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ESKD Burden From Diabetes and Hypertension

- 4.2.2 Home Dialysis Adoption and Reimbursement Support

- 4.2.3 Kidney Transplant Shortage Sustaining Dialysis Demand

- 4.2.4 Connected Dialysis and Therapy Upgrade Cycle

- 4.2.5 AKI Home Dialysis Reimbursement Expansion

- 4.2.6 Medicare Advantage and Value-Based Kidney Care Steering

- 4.3 Market Restraints

- 4.3.1 Reimbursement-Cost Mismatch for Providers

- 4.3.2 Nephrology Nursing and Technician Shortage

- 4.3.3 PD Fluid Supply Fragility

- 4.3.4 Oral Phosphate-Binder Bundle Workflow Burden

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 Hemodialysis

- 5.1.2 Peritoneal Dialysis

- 5.2 By Product & Service

- 5.2.1 Devices

- 5.2.2 Consumables

- 5.2.3 Services

- 5.3 By Disease Indication

- 5.3.1 End-stage Kidney Disease/CKD

- 5.3.2 Acute Kidney Injury

- 5.4 By End-use Setting

- 5.4.1 Freestanding Dialysis Centers

- 5.4.2 Hospital-based Dialysis Centers

- 5.4.3 Home Care Settings

- 5.4.4 Skilled Nursing and Long-term Care Settings

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 B. Braun Medical Inc.

- 6.3.2 DaVita Inc.

- 6.3.3 Dialysis Clinic, Inc.

- 6.3.4 Dialyze Direct

- 6.3.5 Fresenius Medical Care AG

- 6.3.6 Innovative Renal Care

- 6.3.7 Merit Medical Systems, Inc.

- 6.3.8 Mozarc Medical

- 6.3.9 Nikkiso Medical America, Inc.

- 6.3.10 Nipro Medical Corporation

- 6.3.11 Northwest Kidney Centers

- 6.3.12 Outset Medical, Inc.

- 6.3.13 Quanta Dialysis Technologies

- 6.3.14 Rockwell Medical, Inc.

- 6.3.15 Satellite Healthcare

- 6.3.16 The Rogosin Institute

- 6.3.17 U.S. Renal Care, Inc.

- 6.3.18 Vantive Health LLC

- 6.3.19 W. L. Gore & Associates, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment