PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064436

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064436

Crypto Wallet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

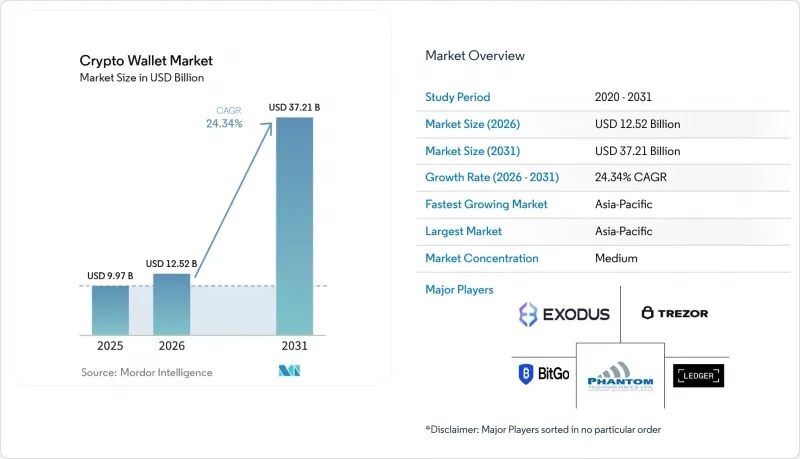

According to Mordor Intelligence, the crypto wallet market size is projected to be USD 9.97 billion in 2025, USD 12.52 billion in 2026, and reach USD 37.21 billion by 2031, growing at a CAGR of 24.34% from 2026 to 2031.

This report is Segmented by Wallet Type (Hot Wallets, and Cold Wallets), Application (Trading, Peer-To-Peer Payments, Remittance, Merchant Payments and E-Commerce, and DeFi and Web3 Access), End-User (Individual Users, Enterprises, Crypto-Native Institutions, Financial Institutions and Fintechs, Merchants and Payment Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Crypto Wallet Market Trends and Insights

Expanding DeFi and Web3 Participation

DeFi has become a major structural driver of demand for the crypto wallet market, as wallets are now the primary interfaces for swaps, staking, liquidity provision, and access to tokenized assets. Activity is no longer concentrated in experimental retail use, as wallet-linked execution is increasingly tied to broader on-chain financial activity and a wider set of applications. Embedded swap activity via wallet providers rose meaningfully in 2025, reinforcing the wallet's role as a transaction layer rather than a passive storage tool. Tokenized real-world assets also expanded sharply by 2025, underscoring the need for custody interfaces that support compliant ownership, auditable movement, and direct user control. As more users interact with DeFi directly from wallet environments, the crypto wallet market is seeing stronger monetization opportunities through swaps, routing, and premium security features. This is why the crypto wallet market continues to benefit when wallet-native execution gains share relative to exchange-native execution.

Rising Institutional and Treasury Adoption

Institutional buying has become a major driver of the crypto wallet market because treasury use requires stronger controls than consumer trading. Public company participation widened further by 2026, and Strategy Inc. alone held 818,869 BTC as of May 11, 2026, which illustrates how treasury-scale adoption can reshape wallet demand and custody architecture. A Coinbase institutional survey released in 2025 found that more than 75% of respondents planned to increase their digital asset allocations in 2025, and 84% were already using or considering stablecoins, pointing to broader demand for regulated wallet infrastructure. The institutional requirement is moving beyond simple hot-and-cold separation toward multi-party computation, policy controls, and regulated settlement connectivity, which raises the value of enterprise wallet platforms. U.S. accounting and custody changes also widened the addressable base for banks and licensed providers, which supports a larger long-term opportunity for the crypto wallet market. As these buyers enter, the crypto wallet market is becoming more service-led and compliance-led, not only feature-led.

Private Key and Seed Phrase Complexity

Private key and seed phrase management remains a basic friction point for the crypto wallet market because fund recovery still depends on user behavior that feels unfamiliar to most consumers. The risk is not only technical difficulty but also the permanent loss scenario that can result from a simple mistake or poor backup practices. ThreatFabric disclosed the Crocodilus Android malware in 2025, and the attack used fake urgent backup prompts to trick users into revealing wallet phrases directly on compromised devices. In response, the crypto wallet market is moving toward account abstraction, smart wallets, and recovery models that reduce direct phrase handling, and Ethereum.org reported more than 26 million ERC-4337 smart wallet deployments with over 170 million UserOperations by April 2026. Even so, migration takes time because existing users must be re-educated while new users must learn a different security model from the start. Until that transition becomes more standard, the crypto wallet market will continue to face a usability ceiling among less experienced users.

Other drivers and restraints analyzed in the detailed report include:

- Stablecoin-Based Remittance and Payments Utility

- Mobile-First Onboarding and Fiat-to-Crypto Rails Expansion

- Rising Phishing, Drainers, and Wallet Exploits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hot wallets accounted for 56.23% of revenue in 2025, keeping them at the center of the crypto wallet market as the most practical option for daily trading, DeFi access, and frequent swaps. Their lead reflects the continued preference for internet-connected wallets when users need immediate execution, dApp connectivity, and simple portfolio movement. Mobile, web, and desktop hot wallets each still serve distinct user groups, with mobile favored for daily transfers and browser-linked setups preferred for deeper DeFi activity. The convenience advantage remains strong, which is why hot wallets have maintained the broadest commercial reach in the crypto wallet industry. Hot wallets also benefit from wallet-native transaction growth, as users can now swap, bridge, and interact with protocols without returning to centralized exchange interfaces.

Cold wallets are the fastest-growing type, with the crypto wallet market size for cold wallets projected to expand at a 25.74% CAGR through 2031. That growth reflects institutional treasury buying, higher sensitivity to counterparty risk, and stronger demand from users holding larger balances for longer periods. Strategy Inc.'s treasury position highlights why large holders increasingly depend on cold storage architecture for asset segregation and approval control. Hardware providers responded with more advanced products in 2025, including Ledger Nano Gen5 and Trezor Safe 7, both of which pushed security and usability improvements further into the mainstream. A hybrid model is now common, in which software wallets handle daily activity and hardware signers protect reserve balances, reshaping how the crypto wallet market is monetized across device and software layers. Paper wallets remain a minor and declining niche because they offer limited verification, poor usability, and little alignment with current compliance expectations.

Geography Analysis

Asia-Pacific held 36.81% of the crypto wallet market share in 2025 and is also the fastest-growing region, with a 25.24% CAGR through 2031. That combination shows that the crypto wallet market in Asia-Pacific is not growing from a small base, but from deep and broad user demand. India remained the global leader in crypto adoption through 2025, and the country also recorded USD 338 billion in on-chain transaction volume, which supported its leading position. Japan and South Korea added a different layer of demand, with regulatory progress, high trading intensity, and stronger stablecoin usage supporting regional wallet activity. Pakistan and Vietnam also moved toward more formal policy recognition in 2025, which supports the next wave of regional wallet adoption in remittance-heavy and mobile-first markets. This mix keeps Asia-Pacific at the center of the crypto wallet market across both retail and professional use.

North America and Europe remained the main poles of institutional demand in the crypto wallet market during 2025 and 2026. In North America, the United States benefited from clearer, more stable direction on stablecoins and market structure, which reduced some of the hesitation around custody integration and regulated access. Strategy Inc.'s May 2026 filing noted that major banks, including Morgan Stanley, Goldman Sachs, and Citigroup, had announced bitcoin trading, custody, and lending services, reflecting a more normalized institutional environment. In Europe, full MiCA enforcement in 2026 and related reporting rules raised the operating bar for providers by increasing authorization, record-keeping, and disclosure requirements. That favors larg, nd better-capitalized firms gradually reshaping the crypto wallet market in Europe toward fewer providers with stronger compliance capacity.

South America, the Middle East, and Africa added a different demand profile to the crypto wallet market, with stablecoins playing a more functional role in treasury preservation, merchant settlement, and cross-border transfers. South American adoption is supported by local-currency pressure, and a consortium study showed that Colombian companies using USD-pegged stablecoins materially reduced inflation losses on treasury funds, while USDC captured a large share of stablecoin volume in Argentina. Brazil also improved the operating environment in 2025 through secondary rules under its Virtual Assets Law, which enabled wallet providers to gain greater market participation. In the Middle East and Africa, the UAE is positioning itself as a premium institutional hub, while sub-Saharan Africa recorded more than 50% year-over-year growth in on-chain transaction volumes in 2025, led by retail transfers below USD 10,000. Together, these regions are expanding the crypto wallet market through practical payment use cases rather than solely on trading demand.

- Ledger SAS

- Trezor Company s.r.o.

- Exodus Movement, Inc.

- Zengo Ltd.

- Phantom Technologies, Inc.

- ARGENT LABS LIMITED

- Zerion, Inc.

- SafePal LTD

- Tangem AG

- Shift Crypto AG

- Coinkite Inc.

- CoolBitX Ltd.

- ELLIPAL LIMITED

- Horkos, Inc.

- IoTrust Co., Ltd.

- ONEKEY LIMITED

- Yanssie HK Limited

- BitGo, Inc.

- Fireblocks Inc.

- Cobo Global Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding DeFi and Web3 Participation

- 4.2.2 Rising Institutional and Treasury Adoption

- 4.2.3 Stablecoin-Based Remittance and Payments Utility

- 4.2.4 Mobile-First Onboarding and Fiat-to-Crypto Rails Expansion

- 4.2.5 Account Abstraction and Seedless Recovery Reducing User Friction

- 4.2.6 AI-Agent and Machine-Wallet Demand

- 4.3 Market Restraints

- 4.3.1 Private Key and Seed Phrase Complexity

- 4.3.2 Rising Phishing, Drainers, and Wallet Exploits

- 4.3.3 Fragmented Self-Custody Compliance and Travel Rule Burden

- 4.3.4 Hardware Wallet Cost Inflation and Secure-Element Supply Risk

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wallet Type

- 5.1.1 Hot Wallets

- 5.1.2 Cold Wallets

- 5.2 By Application

- 5.2.1 Trading

- 5.2.2 Peer-To-Peer Payments

- 5.2.3 Remittance

- 5.2.4 Merchant Payments and E-Commerce

- 5.2.5 DeFi and Web3 Access

- 5.3 By End-User

- 5.3.1 Individual Users

- 5.3.2 Enterprises

- 5.3.3 Crypto-Native Institutions

- 5.3.4 Financial Institutions and Fintechs

- 5.3.5 Merchants and Payment Providers

- 5.3.6 Web3 Studios and Developers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ledger SAS

- 6.4.2 Trezor Company s.r.o.

- 6.4.3 Exodus Movement, Inc.

- 6.4.4 Zengo Ltd.

- 6.4.5 Phantom Technologies, Inc.

- 6.4.6 ARGENT LABS LIMITED

- 6.4.7 Zerion, Inc.

- 6.4.8 SafePal LTD

- 6.4.9 Tangem AG

- 6.4.10 Shift Crypto AG

- 6.4.11 Coinkite Inc.

- 6.4.12 CoolBitX Ltd.

- 6.4.13 ELLIPAL LIMITED

- 6.4.14 Horkos, Inc.

- 6.4.15 IoTrust Co., Ltd.

- 6.4.16 ONEKEY LIMITED

- 6.4.17 Yanssie HK Limited

- 6.4.18 BitGo, Inc.

- 6.4.19 Fireblocks Inc.

- 6.4.20 Cobo Global Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment