PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064442

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064442

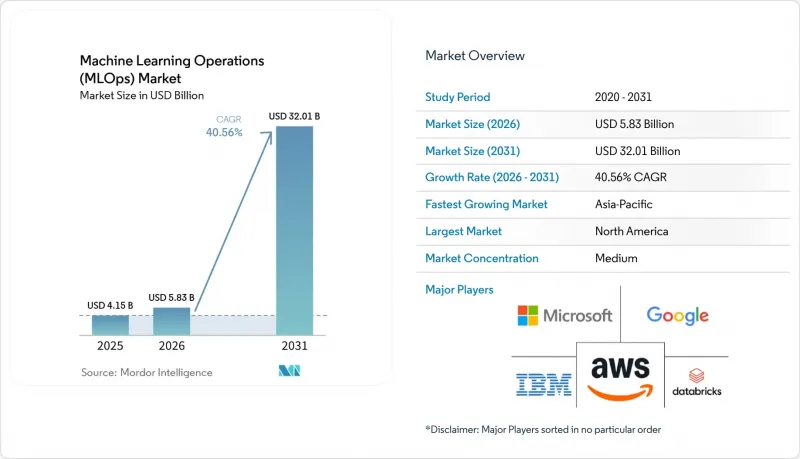

Machine Learning Operations (MLOps) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the machine learning operations (MLOps) market size is projected to expand from USD 4.15 billion in 2025 and USD 5.83 billion in 2026 to USD 32.01 billion by 2031, registering a CAGR of 40.56% between 2026 to 2031.

This report is Segmented by Component (Platform, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, IT and Telecom, Retail and E-Commerce, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Machine Learning Operations (MLOps) Market Trends and Insights

Scaling AI from Pilot to Production

The machine learning operations (MLOps) market is being lifted by a basic enterprise problem, many organizations can build models, but far fewer can move them into stable production with repeatable controls. Once model counts rise across departments, manual promotion, version tracking, rollback, and retraining quickly become operational bottlenecks that slow value capture and increase release risk. This pressure is pushing buyers toward platforms that standardize handoffs across development, validation, deployment, and monitoring, rather than relying on separate point tools and custom scripts. Amazon SageMaker AI added serverless MLflow in December 2025, which shows how vendors are trying to reduce setup work and shorten the path from experimentation to managed deployment. Microsoft Fabric also introduced cross-workspace logging for MLflow in April 2026, which supports cleaner separation across development, test, and production environments without breaking workflow continuity. As a result, the MLOps market is gaining from enterprise demand for operating discipline as much as it is gaining from demand for new AI features.

Rising Need for Model Monitoring and Drift Management

The MLOps market is also expanding because production models do not stay reliable without continuous oversight after deployment. Performance decay, changing data patterns, latency shifts, and policy failures can emerge gradually, and these issues are harder to detect in customer-facing generative systems than in traditional prediction workloads. Databricks addressed this shift in June 2025 with MLflow 3.0, which added production-scale tracing, prompt tracking, and LLM judges to support evaluation and observability across generative AI workflows. Amazon SageMaker AI integrated MLflow 3.10 in May 2026 with tracing for multi-turn workflows and built-in evaluation and dashboarding for latency, token use, and quality, which reflects growing demand for operational visibility after release. Arize AI also added native support for NVIDIA NIM in March 2026 so teams could monitor and evaluate models deployed through that runtime inside the same observability layer. These shifts are making monitoring a central buying criterion in the machine learning operations (MLOps) market, especially as agentic systems introduce longer decision chains and more failure points.

Shortage of Cross-Functional MLOps Talent

The machine learning operations (MLOps) market still faces a real adoption constraint because production AI requires combined skills in data engineering, software delivery, governance, and model operations, and that blend is scarce in most organizations. Many enterprises can fund AI tools, but they still struggle to staff teams that can maintain release pipelines, monitor live systems, manage rollback processes, and document controls for regulated use cases. This shortage is especially visible when organizations move from a few isolated models to broader portfolios that demand standardized release practices and shared governance processes across business units. Platform vendors are responding by building more automation into experiment tracking, deployment templates, and managed workflow tooling, which reduces the amount of specialist labor required for basic operations. Microsoft Fabric's MLflow logging across separate workspaces also reflects this push toward reducing coordination friction for teams that do not have large dedicated platform engineering groups. Even so, the machine learning operations (MLOps) market cannot fully convert strong software demand into production adoption unless buyers can close the gap between tooling access and operational expertise.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud-Native AI Infrastructure

- LLMOps and AgentOps Convergence Raising Lifecycle Complexity

- Fragmented Toolchains And Integration Debt

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms held 64.23% of revenue in 2025, which means the platform layer remained the core spending center across the machine learning operations (MLOps) market. Platforms held 64% of the machine learning operations (MLOps) market share in 2025 because enterprises increasingly preferred one control plane for experiment tracking, model registry, deployment, monitoring, and governance. That preference reflects a broader buyer shift away from stitching together separate lifecycle tools, especially when teams need clear lineage across model releases and policy decisions. Databricks strengthened this model in June 2025 by extending MLflow 3.0 across traditional machine learning and generative AI workflows with tracing, evaluation, and deployment controls on one platform. Amazon SageMaker AI also added serverless MLflow in December 2025, which shows that large vendors see control plane simplification as a direct route to wider production adoption.

Services are forecast to expand at a 41.34% CAGR through 2031, which keeps the service layer highly relevant even in a platform-led revenue structure. The machine learning operations (MLOps) market is not shifting away from human support, because many organizations still need outside help for architecture design, workflow migration, governance setup, and operating model changes. This is especially true when AI programs move into LLMOps and AgentOps, where deployment patterns are less standardized and the cost of poor release design is higher. Microsoft Fabric's cross-workspace logging update in April 2026 illustrates how platform features can reduce complexity, but it also highlights how enterprises still need implementation support to align process, permissions, and production controls across teams. In practice, the MLOps market is moving toward blended delivery models where software and services are purchased together to shorten deployment time and reduce internal operating strain.

Cloud accounted for 53.44% share of the machine learning operations (MLOps) market size in 2025, and it is also the fastest-growing deployment mode with a 40.87% CAGR through 2031. The cloud lead reflects the scale advantages of managed infrastructure, faster environment setup, and tighter integration between compute, orchestration, monitoring, and governance services. Amazon Web Services continued to reinforce this direction in June 2025 by outlining ways to lower GPU training and inference costs, which directly supports cloud-based production AI economics. Google Cloud added orchestration improvements to Managed Asia-Pacifiche Airflow in May 2026, which helps teams run data and AI workloads with less custom engineering overhead. These developments show why the machine learning operations (MLOps) market continues to concentrate a large share of new deployment activity in cloud environments.

On-premises deployment still matters because data residency, sovereign AI requirements, and internal control needs remain strong in regulated and security-sensitive settings. Hybrid architectures are therefore gaining weight, not because cloud growth is slowing, but because many enterprises now need one operating model across cloud, private infrastructure, and edge nodes. Amazon Web Services reflected this broader shift in May 2026 when it made the AWS MCP Server and Agent Toolkit generally available with IAM guardrails and CloudTrail logging, underscoring how secure integration across services has become part of the deployment conversation. Teradata also launched its Autonomous Knowledge Platform in May 2026 for cloud, on-premises, and hybrid environments, which points to sustained demand for deployment consistency across different runtime locations. The MLOps market is therefore likely to remain cloud-led on revenue while becoming more hybrid in operating design over the forecast period.

Geography Analysis

North America held 34.22% of the machine learning operations (MLOps) market share in 2025, which kept it as the largest regional contributor to the machine learning operations (MLOps) market. The region benefits from dense cloud infrastructure, large enterprise AI budgets, a deep vendor base, and a strong concentration of experienced platform and data engineering talent. Amazon said in November 2025 that it would invest up to USD 50 billion to expand AI and supercomputing infrastructure for U.S. government agencies, which supports long-run demand for production-grade MLOps in federal and defense-related environments. Canada is also strengthening its role through new AI and cloud infrastructure commitments that support enterprise adoption and public sector implementation over 2025 and 2026. The United States remains the main regional growth engine because it combines hyperscaler strength, software vendor density, and earlier enterprise adoption patterns than most other markets.

Asia-Pacific is the fastest-growing regional segment at a 41.63% CAGR through 2031, and this keeps it central to the longer-term expansion path of the machine learning operations (MLOps) market. Growth across the region is supported by a rising base of enterprise AI adoption, stronger policy attention, and more demand for cloud-native platforms that can be deployed quickly. Japan stands out for corporate API adoption, with OpenAI reporting the largest number of corporate API customers outside the United States, which suggests strong demand conditions for downstream operational tooling. China contributes significant volume through large-scale enterprise AI deployment and stronger interest in sovereign and on-premises operating models. Singapore is also influencing regional adoption patterns because governance-led AI programs in finance, healthcare, and advanced manufacturing are raising expectations around auditability and lifecycle control across Southeast Asia.

Europe remained the third-largest regional block, with Germany, the United Kingdom, and France accounting for much of regional spending in the machine learning operations (MLOps) market. Regulatory pressure is a major regional factor, because buyers in regulated sectors are placing greater emphasis on technical documentation, event logging, and human oversight in production AI systems. The appliedAI Initiative in Germany works with 23 of the 40 DAX corporations and treats AI governance as part of the operating model itself, which reflects how compliance is being built directly into MLOps practice. South America, the Middle East, and Africa remain smaller in aggregate, but sovereign AI priorities, public sector programs, and financial services digitization still create targeted opportunities for vendors that can support in-country, hybrid, or tightly governed deployment architectures.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- IBM Corporation

- Databricks, Inc.

- DataRobot, Inc.

- Domino Data Lab, Inc.

- Dataiku SAS

- H2O.ai, Inc.

- Cloudera, Inc.

- Hewlett Packard Enterprise Company

- SAS Institute Inc.

- Snowflake Inc.

- Teradata Corporation

- Seldon Technologies Ltd.

- ClearML Inc.

- Weights & Biases, Inc.

- Neptune Labs Sp. z o.o.

- Fiddler AI, Inc.

- ModelOp, Inc.

- Arize AI, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Scaling AI From Pilot to Production

- 4.2.2 Rising Need for Model Monitoring and Drift Management

- 4.2.3 Expansion of Cloud-Native AI Infrastructure

- 4.2.4 Tightening AI Governance and Auditability Requirements

- 4.2.5 LLMOps and AgentOps Convergence Raising Lifecycle Complexity

- 4.2.6 GPU FinOps and Inference Cost Control Becoming a Platform Priority

- 4.3 Market Restraints

- 4.3.1 Shortage of Cross-Functional MLOps Talent

- 4.3.2 Fragmented Toolchains and Integration Debt

- 4.3.3 Sovereign AI and Data Localization Rules Fragmenting Deployment Architectures

- 4.3.4 Security Exposure Across Model Registries, Feature Stores, and CI/CD Supply Chains

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.4.1 Enterprise IT Budget Prioritization

- 4.4.2 GPU and Accelerated Compute Cost Inflation

- 4.4.3 Cloud Cost Optimization and FinOps Pressure

- 4.4.4 Trade Policy and Semiconductor Supply Exposure

- 4.5 Industry Value Chain Analysis

- 4.5.1 Data Ingestion and Labeling

- 4.5.2 Feature Engineering and Feature Store Management

- 4.5.3 Model Development and Experimentation

- 4.5.4 Validation and Responsible AI Controls

- 4.5.5 Deployment and Serving

- 4.5.6 Monitoring, Observability, and Retraining

- 4.5.7 Integration, Support, and Managed Services

- 4.6 Regulatory Landscape

- 4.6.1 AI Governance and Model Risk Management Rules

- 4.6.2 Data Privacy and Cross-Border Data Transfer Requirements

- 4.6.3 Sector-Specific Compliance for BFSI, Healthcare, and Public Sector Deployments

- 4.6.4 Copyright, Provenance, and Foundation Model Usage Controls

- 4.7 Technological Outlook

- 4.7.1 Unified MLOps and LLMOps Control Planes

- 4.7.2 Multi-Cloud and Hybrid Orchestration

- 4.7.3 Feature Stores, Vector Stores, and Metadata Layers

- 4.7.4 Automated Evaluation, Guardrails, and Policy-as-Code

- 4.7.5 Edge and Real-Time Model Serving

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.1.1 Experiment Tracking and Collaboration

- 5.1.1.2 Pipeline Orchestration and CI/CD

- 5.1.1.3 Feature Store and Data Lineage

- 5.1.1.4 Model Registry and Versioning

- 5.1.1.5 Deployment and Serving

- 5.1.1.6 Monitoring and Observability

- 5.1.1.7 Governance and Responsible AI

- 5.1.2 Services

- 5.1.2.1 Consulting and Strategy

- 5.1.2.2 Implementation and Integration

- 5.1.2.3 Training and Enablement

- 5.1.2.4 Managed Services

- 5.1.2.5 Support and Maintenance

- 5.1.1 Platform

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 IT and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Media and Entertainment

- 5.4.9 Transportation and Logistics

- 5.4.10 Education and Research

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Singapore

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Kenya

- 5.5.6.5 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC

- 6.4.4 IBM Corporation

- 6.4.5 Databricks, Inc.

- 6.4.6 DataRobot, Inc.

- 6.4.7 Domino Data Lab, Inc.

- 6.4.8 Dataiku SAS

- 6.4.9 H2O.ai, Inc.

- 6.4.10 Cloudera, Inc.

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 SAS Institute Inc.

- 6.4.13 Snowflake Inc.

- 6.4.14 Teradata Corporation

- 6.4.15 Seldon Technologies Ltd.

- 6.4.16 ClearML Inc.

- 6.4.17 Weights & Biases, Inc.

- 6.4.18 Neptune Labs Sp. z o.o.

- 6.4.19 Fiddler AI, Inc.

- 6.4.20 ModelOp, Inc.

- 6.4.21 Arize AI, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Future Outlook