PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064466

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064466

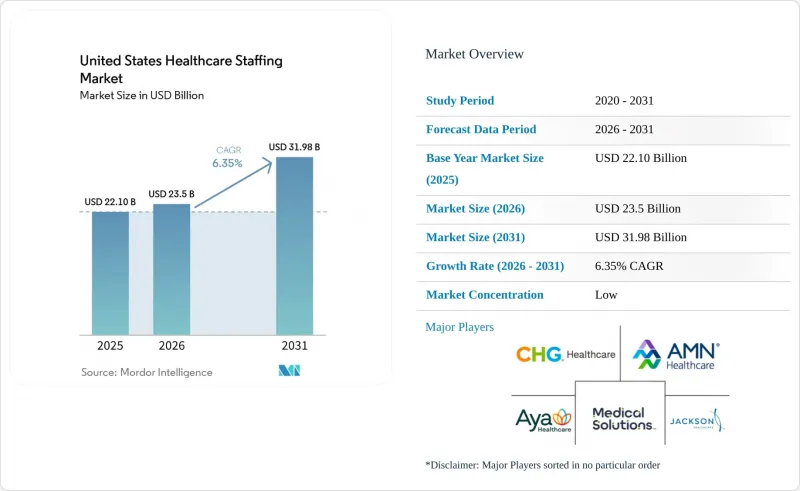

United States Healthcare Staffing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states healthcare staffing market size is expected to grow from USD 22.10 billion in 2025 to USD 23.5 billion in 2026 and is forecast to reach USD 31.98 billion by 2031 at 6.35% CAGR over 2026-2031.

This report is Segmented by Service (Travel Nurse, Per Diem Nurse, Locum Tenens, Allied Health, Others), End User (Hospitals, Ascs, Physician Groups, Long-Term Care, Home Health/Hospice/PACE, Others), Profession (Nursing, Physicians & APPs, Allied Health, Non-Clinical), Delivery Mode (On-Site, Remote/Tele-staffing). Market Forecasts are Provided in Terms of Value (USD).

United States Healthcare Staffing Market Trends and Insights

Aging Population and Chronic Disease Burden

The aging of the US population is widening the care burden that providers must absorb across acute care, home health, and post-acute settings in the US healthcare staffing market. The population aged 65 and older is expected to reach 23% of the total population by 2050, or 82 million people, and more than half of this group is expected to develop serious disabilities that require paid long-term services. That shift changes the acuity mix because patients are leaving hospitals sooner and entering home-based and post-acute settings with more complex clinical needs. Those care sites usually do not have deep permanent staffing benches, so they rely more heavily on contingent clinicians to absorb higher-complexity caseloads. Chronic disease management also pushes demand toward specialist locum coverage in cardiology, pulmonology, and behavioral health, which supports stronger revenue per placement even when general travel nurse rates remain under pressure.

Provider Shortages and Burnout-Driven Vacancy Levels

Provider burnout continues to feed vacancy levels in the US healthcare staffing market even though some burnout indicators have improved from their recent peaks. The American Medical Association reported a physician burnout rate of 41.9% in 2025, with emergency medicine at 49.8%, showing that stress remains concentrated in hospital-based specialties that are difficult to staff. Nursing trends show a similar split because 75% of nurses reported career satisfaction, yet 58% said they experience burnout most days and only 39% planned to stay in their current jobs over the next 12 months. That means churn, not only total workforce loss, is driving placement demand as clinicians move into travel work, per diem roles, or early retirement. Replacement pressure remains strong enough that temporary staffing demand can stay elevated even when total system headcount looks stable on paper.

Hospital Margin Pressure and Reimbursement Volatility

Hospital finances remain the main near-term constraint on the US healthcare staffing market. Median operating margin fell to -0.6% in January 2026 from 1.3% in December 2025, while total expenses kept rising faster than revenue. The American Hospital Association reported that hospital expenses rose 7.5% in 2025, with drug costs up 13.6% and supply costs up 9.9%, which leaves procurement teams looking for labor savings even when staffing is not the original source of cost inflation. Medicare reimbursement covered only 83 cents of every dollar of hospital costs in 2024, which keeps the reimbursement gap structural rather than temporary. As a result, clients are consolidating vendors, expanding MSP oversight, and pushing rate compression harder, which narrows room for smaller agencies without proprietary platforms or compliance infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- Flexible Labor Adoption for Cost and Coverage Management

- Expansion of Home Health, Outpatient, and Post-Acute Sites of Care

- Visa and Immigration Bottlenecks for Internationally Trained Clinicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Travel nurse staffing held 42.31% of revenue in 2025, making it the largest service line in the US healthcare staffing market. Its position remains tied to the segment's role as the primary flex-labor buffer for acute-care facilities dealing with census swings and difficult specialty coverage. The segment is becoming more specialty-driven than geography-driven because ICU, emergency medicine, and behavioral health roles still command higher bill rates than general medical-surgical assignments. This means travel nursing is retaining strategic importance even after broad post-pandemic rate normalization. At the same time, locum tenens staffing is the fastest-growing service category and is projected to expand at an 8.38% CAGR through 2031, which shows where the sharpest unmet physician and APP gaps are forming.

Locum tenens growth is being reinforced by changing care models rather than only by temporary vacancy spikes. Advanced practice provider use within the locum tenens segment increased by nearly 25% year over year in the first half of 2024 as scope-of-practice expansion and facility redesign moved more coverage responsibility away from physician-only models. Flexible scheduling supports that pattern because 81% of nurses said schedule flexibility would do the most to improve working conditions. Allied healthcare staffing segment is led by imaging, respiratory care, and surgical support roles, while strike staffing, international nurse staffing, and health-plan staffing give larger operators broader revenue diversification across the US healthcare staffing industry. Other service niches can also produce sharp revenue spikes, as shown by AMN Healthcare's labor disruption events.

Hospitals accounted for 41.24% of revenue in 2025 and remained the largest end-user group in the US healthcare staffing market. They still need large volumes of contingent labor because inpatient care, emergency operations, surgery, and high-acuity units cannot function with narrow staffing buffers. Even so, the fastest demand expansion is coming from home health, hospice, and PACE organizations, which are projected to grow at an 8.52% CAGR through 2031. That shift reflects the movement of Medicare spending and care delivery toward home- and community-based models, especially for dementia, palliative, and chronic disease management. In this part of the US healthcare staffing market size, agencies are increasingly supplying skilled clinical labor rather than only lower-cost support roles.

The friction in home-based care is not only demand growth, but also the inability of providers to create lasting internal workforce stability. High turnover in frontline home health roles and the rising acuity of patients in the home setting make agency-supplied nurses and allied clinicians critical for continuity. Hospitals are also managing two opposing forces at the same time because compliance requirements create a practical floor for contingent staffing, while weak margins keep procurement teams aggressive in contract negotiations. Ambulatory surgical centers, physician groups, and clinics are adding demand as outpatient procedures increase and physician practices struggle with a 129-day average time-to-fill for permanent physician positions. Long-term care and rehabilitation facilities also support steady agency demand because vacancy and turnover remain elevated in licensed practical nursing roles, and compliance-led minimum staffing expectations make shift-by-shift coverage harder to manage with permanent staff alone. This keeps end-user demand broad even as the growth center moves away from traditional hospital-only buying patterns in the US healthcare staffing market.

List of Companies Covered in this Report:

- Amergis Healthcare Staffing

- AMN Healthcare

- Aya Healthcare

- Barton Associates

- CHG Healthcare

- Cross Country Healthcare

- Epic Staffing Group

- Fastaff / U.S. Nursing

- Favorite Healthcare Staffing

- HealthTrust Workforce Solutions

- Ingenovis Health

- Jackson Healthcare

- LocumTenens.com

- Medical Solutions

- Medicus Healthcare Solutions

- ShiftMed

- Supplemental Health Care

- TotalMed

- Travel Nurse Across America

- Triage Staffing

- Trusted Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Chronic Disease Burden

- 4.2.2 Provider Shortages and Burnout-Driven Vacancy Levels

- 4.2.3 Flexible Labor Adoption for Cost and Coverage Management

- 4.2.4 Expansion of Home Health, Outpatient, and Post-Acute Sites of Care

- 4.2.5 Interstate Licensure and Tele-Staffing Accelerating Multi-State Deployment

- 4.2.6 APP-Led Coverage Redesign for Hard-To-Fill Specialties

- 4.3 Market Restraints

- 4.3.1 Hospital Margin Pressure and Reimbursement Volatility

- 4.3.2 Credentialing, Privileging, and Compliance Complexity

- 4.3.3 MSP/VMS Fee Compression and Reduced Vendor Access

- 4.3.4 Visa And Immigration Bottlenecks for Internationally Trained Clinicians

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service

- 5.1.1 Travel Nurse Staffing

- 5.1.2 Per Diem Nurse Staffing

- 5.1.3 Locum Tenens Staffing

- 5.1.4 Allied Healthcare Staffing

- 5.1.5 Other Services

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centers

- 5.2.3 Physician Groups and Clinics

- 5.2.4 Long-term Care and Rehabilitation Facilities

- 5.2.5 Home Health, Hospice, and PACE Organizations

- 5.2.6 Other End Users

- 5.3 By Profession

- 5.3.1 Nursing Professionals

- 5.3.2 Physicians and Advanced Practice Providers

- 5.3.3 Allied Health Professionals

- 5.3.4 Non-clinical and Administrative Professionals

- 5.4 By Delivery Mode

- 5.4.1 On-site Staffing

- 5.4.2 Remote/Tele-staffing

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amergis Healthcare Staffing

- 6.3.2 AMN Healthcare

- 6.3.3 Aya Healthcare

- 6.3.4 Barton Associates

- 6.3.5 CHG Healthcare

- 6.3.6 Cross Country Healthcare

- 6.3.7 Epic Staffing Group

- 6.3.8 Fastaff / U.S. Nursing

- 6.3.9 Favorite Healthcare Staffing

- 6.3.10 HealthTrust Workforce Solutions

- 6.3.11 Ingenovis Health

- 6.3.12 Jackson Healthcare

- 6.3.13 LocumTenens.com

- 6.3.14 Medical Solutions

- 6.3.15 Medicus Healthcare Solutions

- 6.3.16 ShiftMed

- 6.3.17 Supplemental Health Care

- 6.3.18 TotalMed

- 6.3.19 Travel Nurse Across America

- 6.3.20 Triage Staffing

- 6.3.21 Trusted Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment