PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064470

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064470

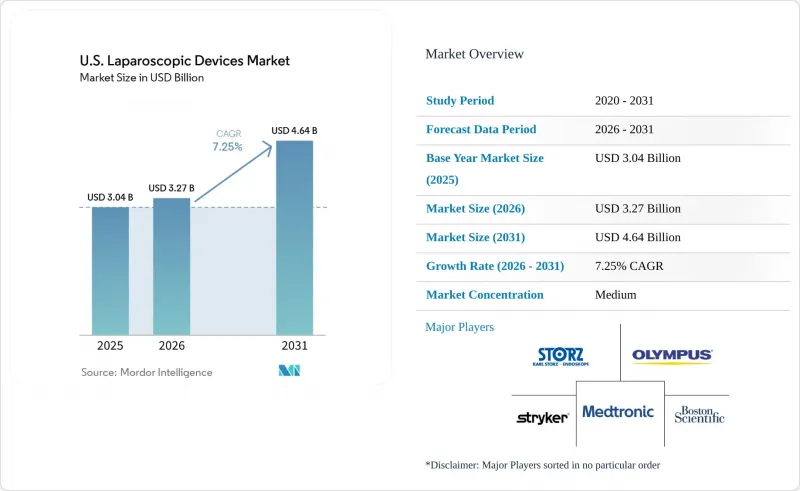

U.S. Laparoscopic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. laparoscopic devices market size is projected to expand from USD 3.04 billion in 2025 and USD 3.27 billion in 2026 to USD 4.64 billion by 2031, registering a CAGR of 7.25% between 2026 to 2031.

This report is Segmented by Product (Visualization Systems, Access Devices, Insufflation and Smoke Management, Hand Instruments, Energy Devices, Closure and Stapling, Retrieval Devices, Robotic-Assisted Platforms), Application (General, Bariatric, Gynecological, and More), and End User (Hospitals, Ascs, Specialty Clinics, Others). Market Forecasts are Provided in Terms of Value (USD).

U.S. Laparoscopic Devices Market Trends and Insights

Hospital and ASC Migration Rewriting Capital Equipment Cycles

In 2026, the CMS OPPS and ASC final rule added 547 codes to the ASC Covered Procedures List, expanding the range of reimbursable procedures in ambulatory settings. Additionally, CMS began a three-year phaseout of the Inpatient-Only list, removing 285 services in 2026, further shifting surgical volumes to cost-effective outpatient sites. This transition is reshaping the United States laparoscopic devices market, as ASCs prioritize compact systems, simpler setups, and faster room turnovers over traditional inpatient OR configurations. Medtronic's Hugo robotic-assisted surgery system reflects this shift with its modular architecture, adaptable to outpatient environments.

Robotic-Enabled Surgery Reshaping the High-Value Instrument Tier

The rise of robotic surgery is driving the United States laparoscopic devices market toward premium instruments and accessories, focusing on recurring use rather than one-time capital investments. Intuitive reported a 17% increase in da Vinci procedures in Q4 2025 and USD 1.69 billion in instruments and accessories revenue in Q1 2026, reflecting a 23% year-over-year growth. Each robotic procedure requires compatible devices, often replacing traditional laparoscopic tools. Medtronic's Hugo and Johnson & Johnson's OTTAVA platforms signal growing competition, with market dynamics now centered on capital access, OR footprint, and robust instrument ecosystems rather than platform availability alone.

Capital Cost Concentration Limiting Platform Penetration in Community Settings

High capital costs significantly limit the adoption of laparoscopic platforms in the United States market. Intuitive reported that the standard sale or lease of a da Vinci system costs between USD 0.6 million and USD 3.1 million, with annual service fees ranging from USD 95,000 to USD 225,000 and per-procedure costs between USD 900 and USD 3,700. While large academic institutions and major health networks can absorb these costs, community hospitals and smaller surgical centers with limited budgets face challenges. This cost disparity slows the adoption of robotic technology in smaller facilities, creating a divided demand where some providers invest in advanced robotics while others opt for cost-effective disposables and incremental upgrades. Modular systems from newer entrants may address this gap over time, but current pricing remains a barrier to faster growth.

Other drivers and restraints analyzed in the detailed report include:

- OR Staffing Constraints Driving Demand for Integrated Workflow Platforms

- Energy and Stapling Premiumization Expanding Per-Procedure Revenue

- CMS Reimbursement Compression Narrowing Margin Headroom for Common Procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Energy Devices held a 29.45% share of the United States laparoscopic devices market, leading the product category. This reflects a shift from traditional electrosurgical methods to advanced vessel-sealing and tissue-management technologies, streamlining minimally invasive procedures. These devices are widely used in general surgery, gynecology, colorectal treatments, and bariatric surgery, ensuring consistent demand.

Hand Instruments, Closure and Stapling Devices, Access Devices, and Visualization Systems remain essential but are evolving with a focus on disposables, integrated workflows, and enhanced imaging. Single-use access products simplify logistics in outpatient settings, while advanced visualization stacks gain traction for their 3D, 4K, or fluorescence capabilities. Robotic-Assisted Laparoscopy Platforms and Instruments are projected to grow at an 8.12% CAGR through 2031, driven by Medtronic's Hugo, Johnson & Johnson's OTTAVA, and Intuitive's expanding installed base.

List of Companies Covered in this Report:

- Aesculap

- Applied Medical Resources

- Asensus Surgical US, Inc.

- Beckton Dickinson

- Boston Scientific

- Conmed

- The Cooper Companies

- ERBE USA, Inc.

- Ethicon, Inc.

- Intuitive Surgical, Inc.

- KARL STORZ Endoscopy-America, Inc.

- LivsMed USA Inc.

- Mediflex Surgical Products Corporation

- Medtronic

- Olympus

- Richard Wolf Medical Instruments Corporation

- Smiths Group

- Stryker

- Teleflex

- Virtual Incision Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hospital Outpatient and ASC Migration for Routine Laparoscopy

- 4.2.2 High Obesity Burden Sustaining Bariatric and General Surgery Demand

- 4.2.3 Premiumization of Energy, Powered Stapling, and 4K/3D Imaging

- 4.2.4 Robotic-Enabled Minimally Invasive Surgery Expansion in General Surgery

- 4.2.5 OR Staffing Variability Favoring Integrated Workflow Platforms

- 4.2.6 Smoke Evacuation and Stable Low-Pressure Insufflation Adoption

- 4.3 Market Restraints

- 4.3.1 High Capital and Disposable Cost Burden

- 4.3.2 Robotic Substitution of Conventional Laparoscopic Categories

- 4.3.3 Reimbursement Compression in Common Laparoscopic Procedures

- 4.3.4 FDA Quality and Supply Chain Scrutiny on Device Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Visualization Systems and Laparoscopes

- 5.1.1.1 Rigid Laparoscopes

- 5.1.1.2 Flexible / Deflectable Laparoscopes

- 5.1.1.3 Camera Heads and Video Processors

- 5.1.1.4 Light Sources

- 5.1.1.5 3D / 4K / Fluorescence Imaging Platforms

- 5.1.2 Access Devices

- 5.1.2.1 Trocars and Cannulas

- 5.1.2.2 Veress Needles

- 5.1.2.3 Others

- 5.1.3 Insufflation and Smoke Management

- 5.1.3.1 Insufflators

- 5.1.3.2 Tubing Sets

- 5.1.3.3 Smoke Evacuation Systems

- 5.1.4 Hand Instruments

- 5.1.4.1 Graspers

- 5.1.4.2 Dissectors

- 5.1.4.3 Scissors

- 5.1.4.4 Needle Holders

- 5.1.4.5 Retractors

- 5.1.4.6 Others

- 5.1.5 Energy Devices

- 5.1.5.1 Advanced Bipolar Vessel Sealing

- 5.1.5.2 Ultrasonic Energy Devices

- 5.1.5.3 Others

- 5.1.6 Closure and Stapling Devices

- 5.1.6.1 Endoscopic Linear Staplers

- 5.1.6.2 Circular Staplers Used in Laparoscopic Procedures

- 5.1.6.3 Reloads and Buttressing Materials

- 5.1.6.4 Sutures and Ligation Clips

- 5.1.7 Suction, Irrigation, and Retrieval Devices

- 5.1.7.1 Suction-Irrigation Systems

- 5.1.7.2 Specimen Retrieval Bags

- 5.1.7.3 Cholangiography and Ancillary Devices

- 5.1.8 Robotic-Assisted Laparoscopy Platforms and Accessories

- 5.1.8.1 Multiport Robotic Platforms

- 5.1.8.2 Miniaturized / Table-Mounted Robotic Platforms

- 5.1.8.3 Robotic-Compatible Access and Insufflation Accessories

- 5.1.8.4 Robotic Stapling and Energy Instruments

- 5.1.1 Visualization Systems and Laparoscopes

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Bariatric Surgery

- 5.2.3 Gynecological Surgery

- 5.2.4 Urological Surgery

- 5.2.5 Colorectal Surgery

- 5.2.6 Thoracic and Other Laparoscopic-Adjacent MIS Procedures

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics and Office-Based Surgical Centers

- 5.3.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aesculap, Inc.

- 6.3.2 Applied Medical Resources Corporation

- 6.3.3 Asensus Surgical US, Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Boston Scientific Corporation

- 6.3.6 CONMED Corporation

- 6.3.7 CooperSurgical, Inc.

- 6.3.8 ERBE USA, Inc.

- 6.3.9 Ethicon, Inc.

- 6.3.10 Intuitive Surgical, Inc.

- 6.3.11 KARL STORZ Endoscopy-America, Inc.

- 6.3.12 LivsMed USA Inc.

- 6.3.13 Mediflex Surgical Products Corporation

- 6.3.14 Medtronic plc

- 6.3.15 Olympus Corporation

- 6.3.16 Richard Wolf Medical Instruments Corporation

- 6.3.17 Smith & Nephew plc

- 6.3.18 Stryker Corporation

- 6.3.19 Teleflex Incorporated

- 6.3.20 Virtual Incision Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment