PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064480

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064480

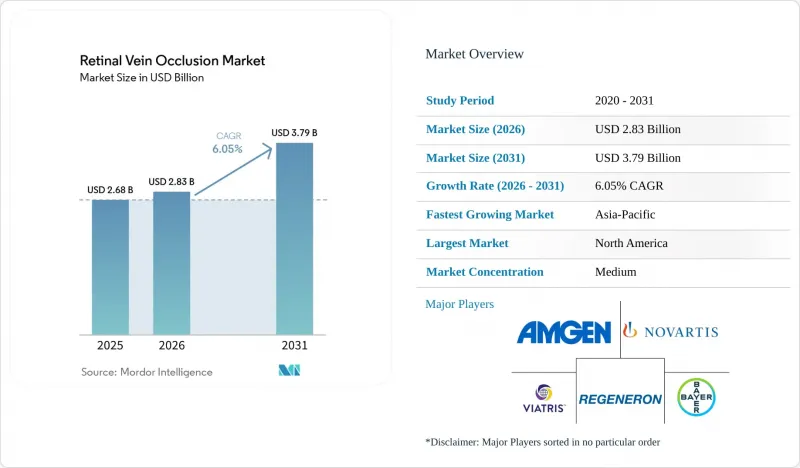

Retinal Vein Occlusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the retinal vein occlusion market size is projected to expand from USD 2.68 billion in 2025 and USD 2.83 billion in 2026 to USD 3.79 billion by 2031, registering a CAGR of 6.05% between 2026 to 2031.

This report is Segmented by Disease Type (BRVO, CRVO, Hemiretinal), Condition (Ischemic, Non-Ischemic), Treatment Modality (Anti-VEGF, Corticosteroid, Laser, Combination), End User (Hospitals, Ophthalmology Clinics and Retina Centers, Ascs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Retinal Vein Occlusion Market Trends and Insights

Aging-Related and Cardio-Metabolic Risk Expansion

Population aging and the rise of cardiometabolic disease are creating a structural increase in the at-risk pool for the retinal vein occlusion market. RVO incidence doubled after age 50 and reached 4.6 per 1,000 in people older than 80 years, which was a 20-fold increase over the 40 to 49 cohort. In East Asian populations, hypertension carried an odds ratio of 4.11 and chronic kidney disease carried an odds ratio of 4.14 for RVO. The 2025 Gutenberg Health Study also showed that CRVO patients faced a 3.83-fold elevated mortality risk independent of traditional cardiovascular factors. This is widening screening and referral activity beyond ophthalmology and bringing more patients into earlier retinal evaluation.

Anti-VEGF Standard-Of-Care Persistence

Anti-VEGF therapy kept its central role in the retinal vein occlusion market because the 2024 American Academy of Ophthalmology Preferred Practice Pattern continued to place intravitreal anti-VEGF agents at the front of care for macular edema secondary to RVO. The clinical need behind this position is durable, since up to 70% of eyes in the LEAVO trial showed persistent or recurrent macular fluid over 100 weeks. That pattern means repeat dosing remains necessary for a large share of patients even after the initial response phase. Price competition can change product mix, but it does not remove the underlying need for ongoing injections when fluid persists. This gives the segment a durable demand floor even as therapy choice becomes more varied.

High Branded Biologic Cost and Repeat Injection Burden

High biologic cost and repeat intravitreal dosing still limit full treatment conversion in the retinal vein occlusion market. The chronic-care profile of anti-VEGF means many eyes need ongoing retreatment rather than a short fixed course, and persistent or recurrent macular fluid remained present in up to 70% of eyes over 100 weeks in LEAVO. By contrast, the Phase IV YANGTZE study reported a mean of 2.3 dexamethasone implant injections over 12 months in Chinese RVO patients, which helps explain why lower-procedure options remain relevant when visit burden is high. The gap between frequent retreatment need and patient capacity creates discontinuation risk in both self-pay and reimbursed settings. For that reason, pricing pressure and dosing burden remain linked restraints even when treatment efficacy is well established.

Other drivers and restraints analyzed in the detailed report include:

- New Approvals and Durability-Led Regimen Expansion

- OCT and OCTA-Led Earlier Detection and Monitoring

- Retina-Clinic Capacity Constraints and Poor Persistence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Branch retinal vein occlusion retained 46.37% of the retinal vein occlusion market share in 2025. BRVO leads because it is 4 times more prevalent than CRVO globally, with risk clustering at the superotemporal crossing, where arterial compression is common in hypertensive patients. A pooled BRVO prevalence of 4.42 per 1,000 translates into a large clinical pool across treated and untreated patients. That structural case volume gives the retinal vein occlusion market a durable base in diagnosis, monitoring, and repeat therapy.

Central retinal vein occlusion is the fastest-growing disease subtype in the retinal vein occlusion market, with an 8.23% CAGR from 2026 to 2031. Growth is being supported by OCTA-based ischemia markers such as foveal avascular zone perimeter, which identified ischemic conversion with 88.9% sensitivity. This matters because previously missed or undertreated CRVO cases are now more likely to be escalated before neovascular complications appear. Hemiretinal vein occlusion remains the smallest segment, but its clearer recognition in clinical protocols is gradually improving diagnostic coding and treatment uptake.

Ischemic RVO accounted for 37.51% of the retinal vein occlusion market size in 2025. Its higher value weight reflects the greater treatment intensity that often comes with neovascular complications, where anti-VEGF, pan-retinal photocoagulation, and corticosteroids can be used together. Non-ischemic retinal vein occlusion is the fastest-growing condition subtype at a 7.93% CAGR through 2031. The larger non-ischemic patient pool is supported by the approximate 3:7 ischemic-to-non-ischemic presentation split and by the steady rise in older at-risk populations.

The retinal vein occlusion market is also changing because imaging can now separate ischemic and non-ischemic presentations earlier in the care pathway. DRIL and the prominent middle-limiting membrane sign differentiated ischemic from non-ischemic RVO in 57% and 58% of cases, respectively. These markers are useful in settings where fluorescein angiography is not always practical. Better triage can move higher-risk patients toward faster escalation when ischemic features are present.

Geography Analysis

North America accounted for 36.43% of the retinal vein occlusion market share in 2025. The region benefits from established retina specialist networks, strong adoption of AAO-guided anti-VEGF care, and broad access to advanced imaging. Canada widened public access in 2025 when faricimab reimbursement expanded in Ontario and Quebec. That expansion extends access beyond private insurance and supports treatment continuity for RVO-related macular edema. North America therefore remains the reference market for high-value biologic use and structured follow-up care.

Europe held the second-largest share of the retinal vein occlusion market in 2025. Access is being shaped by national reimbursement pathways rather than a single regional decision, which creates uneven but expanding uptake. France issued a positive faricimab reimbursement decision, and Spain published a therapeutic positioning report that recognized faricimab as an equivalent first-line alternative to ranibizumab and aflibercept. This mix of national assessments is likely to sustain differences in treatment access and pricing across the region.

Asia-Pacific is projected to record the fastest growth in the retinal vein occlusion market, with a 9.18% CAGR through 2031. Growth is supported by a large future patient base in Asia, by China's expanding retinal care pathway, and by Japan's evidence that delayed anti-VEGF initiation beyond 28 days can worsen long-term vision outcomes. The Phase IV YANGTZE study also showed strong 12-month follow-up completion in Chinese patients on dexamethasone implant therapy, which points to strengthening treatment infrastructure in hospital-based ophthalmology. Middle East, Africa, and South America remain smaller contributors, but government-led retinal screening in GCC systems and Mexico's public assessment of aflibercept point to a gradual build-out of access models outside the largest regions.

- Abbvie

- Alcon

- Amgen

- Annexin Pharmaceuticals AB

- Bayer

- Biocon Biologics Ltd.

- Biogen

- Chugai Pharmaceutical

- EyePoint Pharmaceuticals, Inc.

- F. Hoffmann-La Roche Ltd / Genentech

- Formycon AG

- Kodiak Sciences Inc.

- Novartis

- Outlook Therapeutics, Inc.

- Regeneron Pharmaceuticals

- Samsung Bioepis Co., Ltd.

- Sandoz Group AG

- Santen Pharmaceuticals

- Taiwan Liposome Company, Ltd.

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-Related and Cardio-Metabolic Risk Expansion

- 4.2.2 Anti-VEGF Standard-Of-Care Persistence

- 4.2.3 New Approvals and Durability-Led Regimen Expansion

- 4.2.4 OCT and OCTA-Led Earlier Detection and Monitoring

- 4.2.5 Retina-Clinic Throughput Gains from Extended-Interval Therapy

- 4.2.6 Teleophthalmology And Community OCT Triage Adoption

- 4.3 Market Restraints

- 4.3.1 High Branded Biologic Cost and Repeat Injection Burden

- 4.3.2 Steroid-Related Cataract and Intraocular Pressure Risks

- 4.3.3 Retina-Clinic Capacity Constraints and Poor Persistence

- 4.3.4 AI And OCT Workflow Interoperability Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Disease Type

- 5.1.1 Branch Retinal Vein Occlusion

- 5.1.2 Central Retinal Vein Occlusion

- 5.1.3 Hemiretinal Vein Occlusion

- 5.2 By Condition

- 5.2.1 Ischemic Retinal Vein Occlusion

- 5.2.2 Non-ischemic Retinal Vein Occlusion

- 5.3 By Treatment Modality

- 5.3.1 Anti-VEGF Therapy

- 5.3.1.1 Aflibercept

- 5.3.1.2 Faricimab

- 5.3.1.3 Ranibizumab

- 5.3.1.4 Bevacizumab

- 5.3.1.5 Biosimilar Ranibizumab

- 5.3.1.6 Biosimilar Aflibercept

- 5.3.2 Corticosteroid Therapy

- 5.3.2.1 Dexamethasone Intravitreal Implant

- 5.3.2.2 Intravitreal Triamcinolone

- 5.3.3 Laser Therapy

- 5.3.3.1 Grid Laser Photocoagulation

- 5.3.3.2 Scatter Panretinal Photocoagulation

- 5.3.4 Combination Therapy

- 5.3.1 Anti-VEGF Therapy

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ophthalmology Clinics and Retina Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Alcon Inc.

- 6.3.3 Amgen Inc.

- 6.3.4 Annexin Pharmaceuticals AB

- 6.3.5 Bayer AG

- 6.3.6 Biocon Biologics Ltd.

- 6.3.7 Biogen Inc.

- 6.3.8 Chugai Pharmaceutical Co., Ltd.

- 6.3.9 EyePoint Pharmaceuticals, Inc.

- 6.3.10 F. Hoffmann-La Roche Ltd / Genentech

- 6.3.11 Formycon AG

- 6.3.12 Kodiak Sciences Inc.

- 6.3.13 Novartis AG

- 6.3.14 Outlook Therapeutics, Inc.

- 6.3.15 Regeneron Pharmaceuticals, Inc.

- 6.3.16 Samsung Bioepis Co., Ltd.

- 6.3.17 Sandoz Group AG

- 6.3.18 Santen Pharmaceutical Co., Ltd.

- 6.3.19 Taiwan Liposome Company, Ltd.

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment