PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064485

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064485

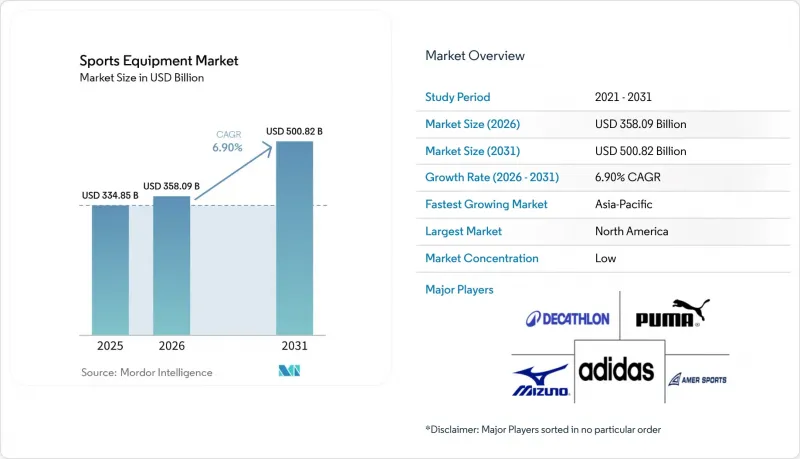

Sports Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sports equipment market is projected to grow from USD 334.85 billion in 2025 to USD 358.09 billion in 2026, reaching USD 500.82 billion by 2031, with a CAGR of 6.90% during 2026-2031.

This report is Segmented by Product Type (Ball Sports, Cycling Sports, Racket Sports, and More), End-User (Male and Female), Application (Personal/Household and Commercial), Distribution Channel (Offline Retail Stores, Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Both Value (USD) and Volume (Tons).

Global Sports Equipment Market Trends and Insights

Rising participation in recreational and professional sports

Rising involvement in fitness activities, competitive sports, and outdoor recreational programs is fueling strong demand for sporting goods, training accessories, and protective equipment. Growing awareness of physical health, active lifestyles, mental wellness, and athletic performance is motivating consumers across various age groups to engage more actively in sports and recreational activities. This trend is leading to consistent purchases of equipment for team sports, individual fitness training, adventure sports, racquet sports, and outdoor recreational activities. For example, according to Statistics Poland, approximately 43.7% of people in Poland participated in sports or recreational activities in 2025, underscoring the increasing consumer engagement in physical and recreational fitness activities . Additionally, the rising popularity of organized tournaments, school athletics, gym memberships, and outdoor recreational participation is driving higher spending on performance-enhancing sports products and fitness equipment.

Growing health and wellness awareness

Increasing health and wellness awareness is driving the growth of the global sports equipment market, as consumers prioritize physical fitness, active lifestyles, and preventive healthcare to enhance overall well-being. Concerns about obesity, cardiovascular diseases, stress management, and sedentary lifestyles are motivating individuals to adopt regular exercise routines, recreational sports, gym training, yoga, cycling, and outdoor fitness activities. This emphasis on physical and mental health is boosting demand for fitness equipment, training accessories, sports gear, and wearable performance products for both household and commercial use. Additionally, awareness campaigns promoting healthy living and participation in physical activities are supporting sustained market growth. The rising adoption of home workouts, digital fitness programs, wellness applications, and sports-based recreational activities is further driving equipment purchases among consumers aiming for healthier lifestyles.

High cost of premium sports equipment

The high cost of premium sports equipment serves as a significant restraint for the global sports equipment market. Advanced sporting goods and high-performance training products are often inaccessible to price-sensitive consumers due to their elevated prices. Equipment made with lightweight composites, smart tracking technologies, impact-resistant materials, and performance-enhancing features typically comes at a higher cost, limiting adoption among recreational users and amateur athletes. Additionally, consumers involved in multiple sports activities may incur substantial expenses for protective gear, accessories, footwear, and maintenance equipment, which can deter frequent product upgrades and replacements. Furthermore, the substantial initial investment required for advanced fitness machines, professional-grade sporting goods, and specialized adventure sports equipment restricts market penetration in cost-conscious consumer segments.

Other drivers and restraints analyzed in the detailed report include:

- Rising popularity of outdoor and adventure sports

- Technological advancements in sports equipment

- Seasonal demand fluctuations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ball sports accounted for 70.89% of market revenues in 2025, driven by widespread participation in organized and recreational sports activities that require consistent use of sporting equipment, accessories, and protective gear. This category benefits from strong engagement across schools, colleges, sports clubs, training academies, and professional competitions, ensuring stable year-round demand for equipment associated with field and court-based games. For example, according to the National Federation of State High School Associations (NFHS), over 921,000 high school students in the United States participated in basketball during 2024-25, underscoring the large-scale participation base supporting equipment demand. The growing emphasis on fitness, teamwork, athletic performance, and youth sports development continues to drive equipment consumption globally at both amateur and professional levels.

Water sports represent the fastest-growing segment in product categorization, with a projected CAGR of 7.56% through 2031. This growth is fueled by increasing global interest in recreational marine activities, adventure tourism, and outdoor fitness participation. Consumer preference for experiential leisure activities such as surfing, kayaking, paddleboarding, jet skiing, snorkeling, and scuba diving is significantly boosting demand for specialized sports equipment and safety gear. Additionally, growing awareness of physical wellness and active lifestyles has encouraged participation in water-based fitness and recreational activities across various age groups. The expansion of water sports training centers, coastal recreational facilities, and organized sporting events further drives demand for equipment such as boards, wetsuits, flotation devices, paddles, and protective accessories.

Male consumers accounted for 66.87% of market revenues in 2025, primarily due to higher participation rates in organized sports, professional athletic competitions, gym-based fitness training, and outdoor recreational activities. Significant engagement in sports such as football, cricket, basketball, cycling, bodybuilding, combat sports, and adventure sports continues to drive demand for sporting goods, protective gear, training accessories, and fitness equipment. This segment benefits from frequent product replacement cycles linked to intensive training routines, competitive sports participation, and the use of performance-focused equipment. Additionally, the growing adoption of fitness-oriented lifestyles, strength training programs, and endurance sports has notably increased demand for technologically advanced and performance-enhancing sports equipment among male consumers.

The female segment is expected to grow at a CAGR of 8.34% during 2026-2031, fueled by rising participation in fitness activities, organized sports, recreational athletics, and outdoor adventure programs. Increased awareness of health, wellness, physical fitness, and active lifestyles has encouraged women to engage in activities such as running, yoga, cycling, gym training, swimming, tennis, and team sports. Enhanced support for women's sports through school programs, professional leagues, fitness communities, and social campaigns is further driving demand for sports equipment, protective gear, and training accessories designed for female consumers. Moreover, improved access to sports facilities, fitness centers, and recreational programs is bolstering long-term participation trends across various age groups.

Geography Analysis

North America is projected to retain its position as the largest regional market with a 38.01% share in 2025. This dominance is attributed to the strong presence of an organized sports culture, widespread participation in both recreational and professional athletic activities, and high consumer engagement in fitness and outdoor sports. The region benefits from extensive sports infrastructure, including stadiums, gyms, training academies, fitness clubs, and educational athletic programs, which consistently drive demand for sporting goods and exercise equipment. Additionally, the strong adoption of technologically advanced fitness products, smart sports equipment, and high-performance training accessories further supports market growth. Increasing participation in school athletics, professional leagues, adventure sports, and home fitness activities continues to bolster equipment consumption across various categories.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 8.09% over the period 2026-2031. This growth is driven by rapidly increasing participation in sports and fitness activities, the expansion of urban recreational culture, and rising investments in sports infrastructure development. The growing popularity of gym memberships, outdoor sports, cycling, water sports, racquet sports, and fitness training among younger consumers is significantly boosting demand for sports equipment in the region. Government initiatives promoting physical fitness, school sports participation, and international sporting events are further encouraging equipment adoption. Additionally, the region is benefiting from the rapid growth of e-commerce platforms, improved accessibility to international sports brands, and rising consumer interest in health and wellness activities.

Europe continues to exhibit strong demand for winter sports equipment, cycling gear, football-related products, and fitness accessories, supported by its well-established sports culture and organized recreational infrastructure. For example, according to Sport England, approximately 298,500 people participated in winter sports activities in England in 2024, reflecting sustained engagement in specialized sports categories that drive equipment demand . South America is witnessing increasing sports participation, driven by its strong football culture, community recreation activities, and expanding fitness awareness. Meanwhile, the Middle East and Africa region is benefiting from growing investments in sports facilities, wellness tourism, and large-scale sporting events, which are encouraging broader adoption of sports equipment and training products.

- adidas AG

- Puma SE

- Decathlon S.A.

- Mizuno Corporation

- Amer Sports, Inc.

- Under Armour, Inc.

- ASICS Corporation

- Nike, Inc.

- Yonex Co., Ltd.

- Topgolf Callaway Brands Corp.

- Acushnet Holdings Corp.

- HEAD N.V.

- Babolat VS S.A.

- Rawlings Sporting Goods Company, Inc.

- Franklin Sports, Inc.

- Technogym S.p.A.

- Johnson Health Tech Co., Ltd.

- Peloton Interactive, Inc.

- Brunswick Corporation

- New Balance Athletics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising participation in recreational and professional sports

- 4.2.2 Growing health and wellness awareness

- 4.2.3 Rising popularity of outdoor and adventure sports

- 4.2.4 Technological advancements in sports equipment

- 4.2.5 Rising influence of international sporting events

- 4.2.6 Growth in youth sports programs and school athletics

- 4.3 Market Restraints

- 4.3.1 High cost of premium sports equipment

- 4.3.2 Seasonal demand fluctuations

- 4.3.3 Risk of injuries associated with sports activities

- 4.3.4 Availability of low-cost counterfeit products

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Ball Sports

- 5.1.2 Cycling Sports

- 5.1.3 Racket Sports

- 5.1.4 Water Sports

- 5.1.5 Winter Sports

- 5.1.6 Other Sports Type

- 5.2 By End-User

- 5.2.1 Male

- 5.2.2 Female

- 5.3 By Application

- 5.3.1 Personal/Houesehold

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 adidas AG

- 6.4.2 Puma SE

- 6.4.3 Decathlon S.A.

- 6.4.4 Mizuno Corporation

- 6.4.5 Amer Sports, Inc.

- 6.4.6 Under Armour, Inc.

- 6.4.7 ASICS Corporation

- 6.4.8 Nike, Inc.

- 6.4.9 Yonex Co., Ltd.

- 6.4.10 Topgolf Callaway Brands Corp.

- 6.4.11 Acushnet Holdings Corp.

- 6.4.12 HEAD N.V.

- 6.4.13 Babolat VS S.A.

- 6.4.14 Rawlings Sporting Goods Company, Inc.

- 6.4.15 Franklin Sports, Inc.

- 6.4.16 Technogym S.p.A.

- 6.4.17 Johnson Health Tech Co., Ltd.

- 6.4.18 Peloton Interactive, Inc.

- 6.4.19 Brunswick Corporation

- 6.4.20 New Balance Athletics, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK