PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064508

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064508

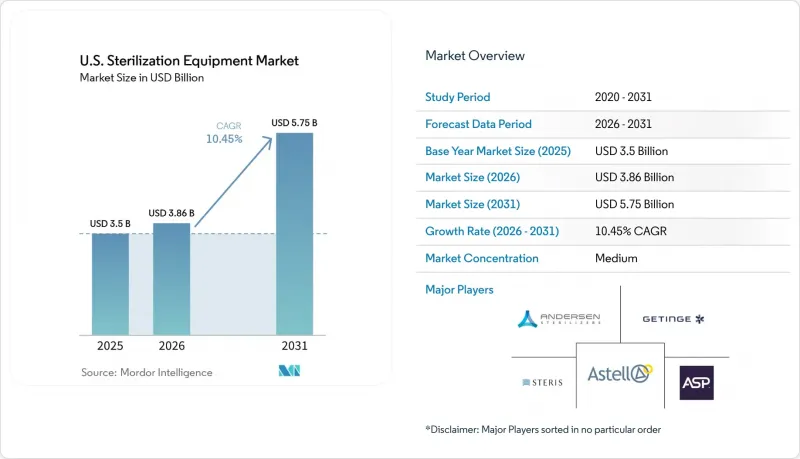

U.S. Sterilization Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. sterilization equipment market size was valued at USD 3.5 billion in 2025 and is estimated to grow from USD 3.86 billion in 2026 to reach USD 5.75 billion by 2031, at a CAGR of 10.45% during the forecast period (2026-2031).

This report is Segmented by Equipment (High-Temp, Low-Temp, Filtration, Ionizing Radiation), End User (Hospitals, Ascs, Specialty Clinics, Pharma/Biopharma, Device Manufacturers and CDMOs, Others), Application (Surgical Instrument Reprocessing, Endoscope Reprocessing, Heat-Sensitive Device, Terminal Sterilization, Aseptic Processing, Lab Waste), and Geography (United States). Forecasts in Value (USD).

U.S. Sterilization Equipment Market Trends and Insights

Rising Procedure Volumes and Instrument Complexity Redefine Sterilization Throughput Requirements

The United States sterilization equipment market is evolving due to increasing surgical volumes and complexity in inpatient and outpatient settings. In 2025, the American Hospital Association reported a 20% higher survival rate for hospitalized surgical patients in early 2024 compared to pre-pandemic benchmarks, reflecting stricter sterility protocols. Higher acuity cases now require advanced instruments like robotic arms and multi-lumen devices, which demand more time and precision for reprocessing. Additionally, a 9.8% rise in outpatient visits in 2025 has increased instrument turnover, driving demand for high-throughput equipment and efficient workflows to optimize space and turnaround times.

HAI Prevention and Reprocessing Compliance Intensity Sustain Baseline Investment

Infection prevention requirements continue to sustain demand for sterilization equipment in the United States. CDC data showed healthcare-associated infections in acute care hospitals dropped from 132,913 in 2023 to 123,204 in 2024, indicating progress but highlighting the need for ongoing investment. Hospitals must maintain improved infection outcomes, increasing the focus on monitoring, validation, and audit readiness. Updated AAMI guidance in 2025 raised standards for chemical and EtO sterilization, making outdated systems harder to justify during quality reviews and driving replacement demand.

High Capital, Validation, and Utility Retrofit Burden

High acquisition costs remain a significant challenge for providers requiring advanced sterilization platforms but operating with limited capital budgets. Large capacity low-temperature systems and automated CSSD lines often necessitate extensive validation, installation modifications, and utility upgrades, adding to the overall expense. Community hospitals and independent ASCs face additional burdens, such as prolonged revalidation, staff retraining, and workflow redesign.

Other drivers and restraints analyzed in the detailed report include:

- ASC Expansion and Compact Sterilizer Demand Reshape Market Geography

- EtO Transition Driving Low-Temperature Equipment Upgrades

- EtO Permitting and Compliance-Driven Downtime Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, high-temperature sterilization held a 48.45% share of the United States sterilization equipment market, maintaining its position as the largest segment. Steam systems remained the preferred choice for heat-tolerant instruments, wrapped goods, and large surgical tray volumes due to their scalability and integration into central sterile workflows. However, their growth is steady rather than accelerating, as more instruments now include components incompatible with traditional steam cycles.

Low-temperature sterilization is the fastest-growing segment, projected to expand at an 11.28% CAGR through 2031 in the United States market. This growth is driven by the increasing use of robotic instruments, flexible scopes, and heat-sensitive devices requiring validated processing. Getinge's introduction of the Poladus 150 VHP sterilizer and the expanded capacity of its GSS67N steam platform in 2026 reflect a shift toward addressing throughput and space efficiency needs.

List of Companies Covered in this Report:

- Advanced Sterilization Products, Inc.

- Andersen Products, LLC

- Astell Scientific Ltd

- BMM Weston

- BMT USA, LLC

- Cisa Group

- Consolidated Sterilizer Systems

- De Lama S.p.A.

- Fedegari Autoclavi

- Getinge

- LTE Scientific Ltd

- MATACHANA Group

- MMM Group

- Noxilizer

- Priorclave North America

- SteelcoBelimed

- Steriflow

- STERIS

- Systec GmbH & Co. KG

- Tuttnauer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Procedure Volumes and Instrument Complexity

- 4.2.2 HAI Prevention and Reprocessing Compliance Intensity

- 4.2.3 ASC Expansion and Compact Sterilizer Demand

- 4.2.4 Eto Transition Driving Low-Temperature Upgrades

- 4.2.5 CSSD Automation and Traceability Investments

- 4.3 Market Restraints

- 4.3.1 High Capital, Validation, and Utility Retrofit Burden

- 4.3.2 Eto Permitting and Compliance-Driven Downtime Risk

- 4.3.3 Single-Use Substitution Reducing In-House Reprocessing Load

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining power of suppliers

- 4.7.2 Bargaining power of buyers

- 4.7.3 Threat of new entrants

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Equipment

- 5.1.1 High-temperature Sterilization

- 5.1.1.1 Wet/Steam Sterilization

- 5.1.1.2 Dry Heat Sterilization

- 5.1.2 Low-temperature Sterilization

- 5.1.2.1 Ethylene Oxide (ETO)

- 5.1.2.2 Hydrogen Peroxide Plasma

- 5.1.2.3 Ozone

- 5.1.2.4 Other Low-temperature Methods

- 5.1.3 Filtration Sterilization

- 5.1.4 Ionizing Radiation Sterilization

- 5.1.4.1 E-beam

- 5.1.4.2 Gamma

- 5.1.4.3 Other Ionizing Technologies

- 5.1.1 High-temperature Sterilization

- 5.2 By End User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Ambulatory Surgery Centers

- 5.2.3 Specialty Clinics And Office-Based Care

- 5.2.4 Pharmaceutical And Biopharmaceutical Manufacturers

- 5.2.5 Medical Device Manufacturers And CDMOs

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Surgical Instrument Reprocessing

- 5.3.2 Flexible Endoscope Reprocessing And Sterilization

- 5.3.3 Heat-Sensitive Device Sterilization

- 5.3.4 Terminal Sterilization Of Finished Medical Devices

- 5.3.5 Aseptic Processing Support And Sterile Transfer

- 5.3.6 Biohazard, Media, And Lab Waste Sterilization

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Sterilization Products, Inc.

- 6.3.2 Andersen Products, LLC

- 6.3.3 Astell Scientific Ltd

- 6.3.4 BMM Weston Ltd

- 6.3.5 BMT USA, LLC

- 6.3.6 Cisa Group

- 6.3.7 Consolidated Sterilizer Systems

- 6.3.8 De Lama S.p.A.

- 6.3.9 Fedegari Autoclavi S.p.A.

- 6.3.10 Getinge AB

- 6.3.11 LTE Scientific Ltd

- 6.3.12 MATACHANA Group

- 6.3.13 MMM Group

- 6.3.14 Noxilizer, Inc.

- 6.3.15 Priorclave North America

- 6.3.16 SteelcoBelimed

- 6.3.17 Steriflow

- 6.3.18 STERIS plc

- 6.3.19 Systec GmbH & Co. KG

- 6.3.20 Tuttnauer

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment