PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064527

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064527

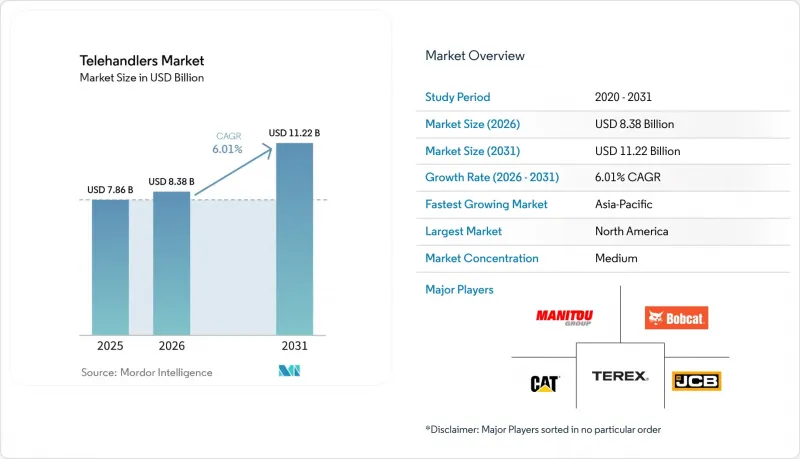

Telehandlers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the telehandlers market size was valued at USD 7.86 billion in 2025 and is estimated to grow from USD 8.38 billion in 2026 to reach USD 11.22 billion by 2031, at a CAGR of 6.01% during the forecast period 2026-2031.

This report is Segmented by Product Type (Compact Telehandlers, High-Reach Telehandlers, and Heavy-Lift Telehandlers), Lift Height (Below 6 Meters, 6-10 Meters, and More), Power Source (Diesel, Hybrid, and More), Application (Construction, Agriculture, Mining and Quarries, and Logistics and Industrial Material Handling), and Geography(North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Telehandlers Market Trends and Insights

Rental Fleet Expansion Across Construction and Agriculture

The telehandlers market is being shaped in a major way by rental companies that now treat telehandlers as core fleet assets rather than occasional additions. This is especially visible in North America and Europe, where fleet operators rely on telematics to track utilization, schedule maintenance, and keep machines in active circulation for longer periods. That model helps large buyers place repeat orders with more predictable replacement cycles, which gives OEMs better production visibility and steadier factory loading. The telehandlers market also benefits because rental fleets often favor better-specified units with stronger uptime tools, which raises the value of each sale even when unit growth moderates. Attachment flexibility adds to this effect, since rental customers want machines that can shift between forks, buckets, work platforms, and handling tools without losing productivity. CanLift Equipment's USD 10 million fleet expansion with JLG in May 2025 showed how telematics and fleet diagnostics are now part of the buying decision, not just an added feature.

Infrastructure and Industrial Project Execution Demand

The telehandlers market continues to draw support from large project pipelines that need repeated lifting, placement, and material positioning over long execution periods. Demand is no longer centered only on conventional building construction, because industrial facilities, logistics parks, grid projects, and large public works all create sustained machine use. Asia-Pacific remains central to this pattern, with China and India supporting volume demand through transport, logistics, and urban development programs. The telehandlers market also gains when contractors need fewer machine changes on site, which increases interest in rotating units and higher-reach models that can cover more tasks during the same project cycle. This demand profile is helping above 10 m machines grow faster, since high-rise work, turbine servicing, and industrial shutdown activity all need greater reach and positioning capability. The result is a more value-focused order mix, where buyers place more weight on reach, stability, and jobsite versatility than on basic lifting performance alone.

High Acquisition and Lifecycle Service Costs

The telehandlers market still faces a clear barrier where upfront equipment cost is high relative to operator cash flow, especially among smaller contractors and family-run farms. Compact entry models remain more accessible, but advanced 5-6 ton units and high-reach machines require much larger capital commitments that many smaller buyers cannot absorb easily. This pushes a larger share of the telehandlers market toward rental channels and delays replacement cycles in direct ownership segments. Compliance engineering also adds cost, since newer diesel platforms need more complex after-treatment systems and service requirements under modern emissions rules.At the same time, the used-equipment market is adjusting to the pace of electrification, which makes residual values harder to read for smaller operators and finance providers. Supply pressure on hydraulics, structural steel, and boom components adds another layer of risk, because cost volatility can narrow margins for OEMs and keep selling prices elevated.

Other drivers and restraints analyzed in the detailed report include:

- Agricultural Mechanization and Labor Substitution

- Electric Telehandler Adoption in Emission-Sensitive Sites

- Skilled Operator and Safety Compliance Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Compact telehandlers held 41.68% of the telehandlers market share in 2025, making them the volume leader within the telehandlers market because they fit the widest range of jobsite and farm conditions. Their smaller footprint suits dense urban sites, narrow farm lanes, indoor-adjacent work areas, and facilities where overhead clearance is limited. This broad usability gives compact machines a durable installed base across construction, agriculture, and mixed rental fleets. The telehandlers industry also favors this segment because rental companies can place compact units across more customer profiles without narrowing the use case too much. In France, compact and agricultural positioning remained strong for established brands, with Manitou accounting for 31.1% of agricultural telehandler registrations in 2025 and Manitou plus JCB together reaching 57.4% of that market.

High-reach and heavy-lift machines serve a smaller base in unit terms, but they carry higher revenue per machine and are often selected for rental-grade work where the duty cycle is more intense. That makes them important to the telehandlers market even when their absolute volume is lower than that of compact models. Rotating telehandlers are the fastest-growing product category and are forecast to expand at 7.24% CAGR through 2031. Demand is rising because contractors want one machine to cover more lifting and access functions on a busy site, which helps reduce equipment coordination and improve utilization. The telehandlers market is therefore shifting toward more feature-rich rotating models, especially where attachment ecosystems, telematics, and higher reach can support premium rental pricing. Compact leadership should remain intact over the near term because the installed use base is broad and replacement demand is recurring. Even so, the balance of value creation in the telehandlers market is moving gradually toward rotating platforms, where customers are more willing to pay for multifunction capability and site efficiency. This mix change matters because it supports revenue growth even if the volume shift remains measured.

The 6-10 m segment accounted for 38.84% of the telehandlers market size in 2025, which made it the broadest volume band in the telehandlers market. That range covers routine residential and commercial construction work, standard stacking tasks on farms, and warehouse replenishment needs that do not require crane-level reach. Rental fleets favor this class because it can serve the largest variety of users without creating major transport or site-access issues. Machines below 6 m hold a smaller but steady role in constrained spaces, indoor-adjacent work, heritage structures, underground repair, and greenhouse settings. The telehandlers market continues to rely on this mid-range specification because it balances reach, versatility, and fleet productivity better than any other height band.

Above 10 m units are forecast to grow at 7.87% CAGR through 2031, which makes them the fastest-growing lift-height segment in the telehandlers market. Their use is expanding in high-rise construction, wind-energy service work, industrial shutdowns, and other applications where reach and stable placement matter more than simple load movement. OEM development activity follows that demand. JCB's November 2025 launch of the Loadall 546-70 and 555-70 expanded its 7 m range to 5.5-ton capacity and added load-sensing hydraulics and automated boom controls, showing how manufacturers are lifting capability within higher-value specifications. The telehandlers industry is using this segment to improve margin quality, since higher-reach units normally support stronger pricing and more specialized fleet demand. This part of the telehandlers market is also where electrification and advanced controls are likely to become more visible over time, especially in urban and indoor-sensitive projects. While volume remains centered in the 6-10 m range, the value mix is moving upward as contractors seek machines that can replace more specialized lifting equipment in selected tasks.

Geography Analysis

North America held 31.58% share in 2025, while Asia-Pacific is expected to post the fastest regional CAGR at 7.18% through 2031. China and India anchor demand because both countries continue to create equipment needs across construction, logistics, and public works. The telehandlers market is also gaining from rising penetration in Southeast Asia, where urban growth and agricultural modernization are widening the addressable user base. Compact units fit many of these use cases well because they suit dense work zones and mixed farm operations. Japan and South Korea remain more mature markets, with stronger mechanization levels and a clearer preference for cleaner and more technically advanced fleets.

Europe remains the most technically mature region in the telehandlers market, with emissions compliance, fleet renewal, and electrification moving faster than in most other regions. EU Stage V pushed buyers toward newer machine generations, while EU Regulation 2025/14 added a more harmonized framework for non-road mobile machinery that circulates on public roads. France, the UK, Germany, and Italy remain central markets in the region. France registered 4,791 agricultural telehandlers in 2025, and the strongest movement came from heavier and taller agricultural units, which points to ongoing mechanization and higher machine capability on farms. North America also remains a large and structurally important part of the telehandlers market because rental penetration is high and newer projects increasingly demand better-specified fleets.

South America, the Middle East, and Africa remain important frontier zones for the telehandlers market, though each is at a different stage of adoption. South America draws support from agribusiness investment and selected mining and infrastructure activity, while the Middle East is driven more by large construction programs and long-duration project work. Saudi Arabia and the UAE are central to that regional demand because large sites need heavy material positioning at height across wide project footprints. Africa is still earlier in its development cycle, but South Africa, Egypt, and Nigeria are creating a latent base for telehandlers as mining, infrastructure, and urbanization expand. The telehandlers market could deepen more quickly in these regions if OEMs strengthen local service coverage, parts availability, and operator support.

- J C Bamford Excavators Ltd.

- Manitou BF SA

- Caterpillar Inc.

- Bobcat Company

- Terex Corporation

- JLG Industries, Inc.

- Merlo S.p.A.

- Dieci s.r.l.

- Liebherr-International AG

- Wacker Neuson SE

- Kramer-Werke GmbH

- CNH Industrial N.V.

- CLAAS KGaA mbH

- Magni Telescopic Handlers S.r.l.

- Faresin Industries SpA

- Xuzhou Construction Machinery Group Co., Ltd.

- AUSA Center, S.L.U.

- SANY Heavy Industry Co., Ltd.

- Action Construction Equipment Ltd.

- Lingong Heavy Machinery (LGMG)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rental Fleet Expansion Across Construction and Agriculture

- 4.3.2 Infrastructure and Industrial Project Execution Demand

- 4.3.3 Agricultural Mechanization and Labor Substitution

- 4.3.4 Electric Telehandler Adoption in Emission-Sensitive Sites

- 4.3.5 Rotating Telehandler Uptake for Crane Substitution

- 4.3.6 Attachment-Led Multi-Use Utilization Gains

- 4.4 Market Restraints

- 4.4.1 High Acquisition and Lifecycle Service Costs

- 4.4.2 Skilled Operator and Safety Compliance Constraints

- 4.4.3 Residual Value Volatility During Fleet Electrification

- 4.4.4 Hydraulic Component and Boom Steel Supply Risk

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Compact Telehandlers

- 5.1.2 High-Reach Telehandlers

- 5.1.3 Heavy-Lift Telehandlers

- 5.2 By Lift Height

- 5.2.1 Below 6 Meters

- 5.2.2 6-10 Meters

- 5.2.3 Above 10 Meters

- 5.3 By Power Source

- 5.3.1 Diesel

- 5.3.2 Hybrid

- 5.3.3 Electric

- 5.4 By Application

- 5.4.1 Construction

- 5.4.1.1 Building Construction

- 5.4.1.2 Infrastructure and Civil Works

- 5.4.2 Agriculture

- 5.4.2.1 Livestock and Dairy

- 5.4.2.2 Crop and Bulk Material Handling

- 5.4.3 Mining and Quarries

- 5.4.4 Logistics and Industrial Material Handling

- 5.4.1 Construction

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 J C Bamford Excavators Ltd.

- 6.4.2 Manitou BF SA

- 6.4.3 Caterpillar Inc.

- 6.4.4 Bobcat Company

- 6.4.5 Terex Corporation

- 6.4.6 JLG Industries, Inc.

- 6.4.7 Merlo S.p.A.

- 6.4.8 Dieci s.r.l.

- 6.4.9 Liebherr-International AG

- 6.4.10 Wacker Neuson SE

- 6.4.11 Kramer-Werke GmbH

- 6.4.12 CNH Industrial N.V.

- 6.4.13 CLAAS KGaA mbH

- 6.4.14 Magni Telescopic Handlers S.r.l.

- 6.4.15 Faresin Industries SpA

- 6.4.16 Xuzhou Construction Machinery Group Co., Ltd.

- 6.4.17 AUSA Center, S.L.U.

- 6.4.18 SANY Heavy Industry Co., Ltd.

- 6.4.19 Action Construction Equipment Ltd.

- 6.4.20 Lingong Heavy Machinery (LGMG)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment