PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064532

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064532

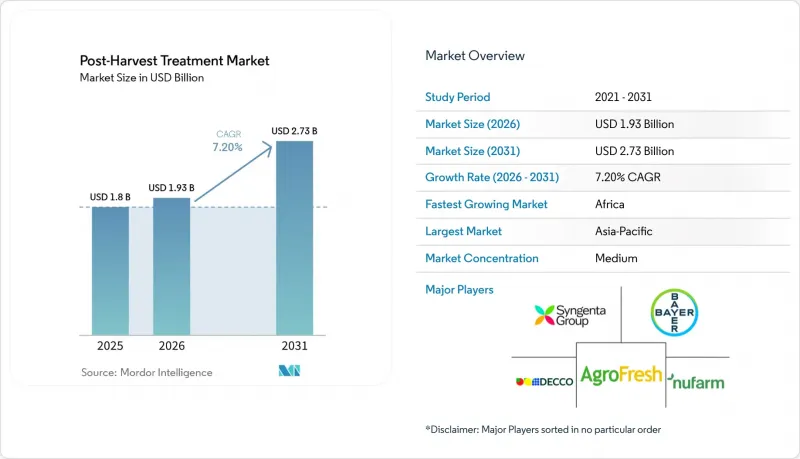

Post-Harvest Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the post-harvest treatment market size was valued at USD 1.80 billion in 2025 and is projected to grow from USD 1.93 billion in 2026 to USD 2.73 billion by 2031, registering a CAGR of 7.20% between 2026 and 2031.

This report is Segmented by Treatment Type (Coatings and Films, Cleaners, Fungicides, Ethylene Blockers, and More), by Formulation (Liquid, Powder, and Gas), by Crop Type (Fruits, Vegetables, Grains, and More), by Origin (Natural and Synthetic), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Post-Harvest Treatment Market Trends and Insights

Cold-chain Expansion in Emerging Markets

Inadequate refrigeration infrastructure continues to result in substantial post-harvest losses, emphasizing the need for cold-chain development. According to the Food and Agriculture Organization (FAO), 526 million metric tons of food, accounting for approximately 12% of global production, are lost due to insufficient refrigeration. This highlights the necessity of investing in cold storage facilities, packhouses, and logistics networks to improve the handling of perishable produce. Such investments also facilitate the adoption of post-harvest treatment solutions, including fungicides, coatings, and ethylene management technologies, thereby driving market demand.

Stringent Supermarket Residue Specifications

Stringent residue specifications in major retail markets are increasing compliance demands on growers and exporters. For instance, the European Commission has reduced the maximum residue level for chlorpropham in potatoes from 0.35 mg/kg to 0.2 mg/kg under Regulation (EU) 2025/1163. This reduction reflects a broader regulatory trend toward stricter food safety standards and lower tolerance levels. Consequently, producers are adopting precision application technologies, residue-compliant fungicides, and bio-based post-harvest treatments to meet retailer requirements, driving growth in the post-harvest treatment market.

Regulatory Tightening on Certain Fungicides

Regulatory scrutiny of synthetic fungicides is increasing as authorities enforce stricter safety and risk mitigation measures. In January 2025, the United States Environmental Protection Agency issued interim registration review decisions for chlorothalonil, thiophanate-methyl, and carbendazim, introducing updated controls to mitigate potential risks to human health and the environment. These measures align with a broader trend of tightening pesticide regulations and reassessing commonly used fungicides. As compliance requirements grow more stringent, manufacturers are investing in safer formulations and alternative solutions, leading to changes in product portfolios and influencing growth patterns in the post-harvest treatment market.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Controlled-Atmosphere Packaging Lines

- Increasing Adoption of Edible Antimicrobial Coatings

- Growing Consumer Resistance to Synthetic Chemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The coatings and films segment accounted for the largest 41.0% of the post-harvest treatment market share in 2025, highlighting their essential role in maintaining freshness and minimizing moisture loss in fruits and vegetables. These solutions are widely utilized due to their compatibility with existing supply chains and compliance with export standards. The growing demand for residue-compliant and bio-based coatings is further reinforcing their market position, particularly in regions with stringent food safety regulations and increasing consumption of organic produce.

The post-harvest treatment market size for the sprout inhibitors segment is projected to grow at the fastest CAGR of 10.8% from 2026 to 2031, driven by increasing demand in storage-intensive crops such as potatoes and onions. Regulatory limitations on traditional chemicals are accelerating the shift toward safer and alternative sprout control methods. Additionally, ethylene blockers and fungicides continue to play a key role in preservation strategies, while cleaners and disinfectants are gaining significance in ensuring hygiene standards across post-harvest handling facilities.

The liquid formulations segment held the largest 58.0% of the post-harvest treatment market share in 2025, driven by their extensive use in spray and dip applications within pack-houses. These formulations are favored for their ease of application, uniform coverage, and compatibility with existing infrastructure. Their versatility across various crop types and treatment methods supports their dominant role in commercial post-harvest operations.

The gas segment is projected to grow at the fastest CAGR of 9.4% from 2026 to 2031, fueled by the increasing adoption of controlled atmosphere storage and ethylene management systems. These formulations allow precise control over ripening and spoilage processes, making them particularly valuable in long-distance trade. Meanwhile, powder formulations continue to see steady demand in grain storage applications, with advancements in delivery mechanisms further improving their efficiency and effectiveness.

Geography Analysis

Asia-Pacific accounted for the largest 33.0% of the post-harvest treatment market share in 2025, driven by expanding agricultural output and increased investment in cold-chain infrastructure. Countries such as China and India are enhancing post-harvest handling systems to minimize food losses and boost export competitiveness. The growing adoption of advanced preservation technologies, such as coatings and controlled atmosphere storage, is further driving regional demand. Additionally, rapid urbanization and rising consumption of fresh produce are fostering the integration of post-harvest treatment solutions across supply chains.

Africa is projected to grow at the fastest CAGR of 9.7% from 2026 to 2031, supported by initiatives to reduce significant post-harvest losses and enhance food security. Governments and international organizations are investing in storage infrastructure and modernizing supply chains. The expansion of horticulture exports and increasing awareness of preservation technologies are contributing to market growth. While infrastructure gaps remain, improved access to cold storage and handling facilities is gradually enabling the adoption of post-harvest treatment solutions across the region.

North America also accounted for a significant share of global revenue in 2025, driven by advanced agricultural practices and strict regulatory frameworks related to food safety. Heightened regulatory focus on pesticide residues and food safety compliance is encouraging growers and distributors to implement more effective preservation solutions. The region's well-structured retail and export-oriented supply chains demand extended shelf life and consistent product quality. This has led to increased adoption of coatings, fungicides, and ethylene management technologies to minimize spoilage, enhance storage efficiency, and meet stringent food safety standards in both domestic and international markets.

- Syngenta AG

- AgroFresh Solutions, Inc.

- Bayer AG

- Decco Post-Harvest Inc. (UPL Limited)

- Nufarm Limited

- John Bean Technologies Corporation

- Xeda International S.A.

- Citrosol, S.A.

- Fomesa Fruitech, S.L.U.

- bio-ferm GmbH (Andermatt Group AG)

- Lytone Enterprise, Inc.

- Janssen PMP (Janssen Pharmaceutica NV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cold-chain expansion in emerging markets

- 4.2.2 Stringent supermarket residue specifications

- 4.2.3 Proliferation of controlled-atmosphere packaging lines

- 4.2.4 Increasing adoption of edible antimicrobial coatings

- 4.2.5 Rise of e-commerce grocery fulfillment centers

- 4.2.6 AI-enabled shelf-life prediction analytics

- 4.3 Market Restraints

- 4.3.1 Regulatory tightening on certain fungicides

- 4.3.2 Growing consumer resistance to synthetic chemicals

- 4.3.3 Price volatility of bio-based raw materials

- 4.3.4 Post-harvest mechanization gaps in developing countries

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Coatings and Films

- 5.1.2 Cleaners

- 5.1.3 Fungicides

- 5.1.4 Ethylene Blockers

- 5.1.5 Sprout Inhibitors

- 5.1.6 Others

- 5.2 By Formulation

- 5.2.1 Liquid

- 5.2.2 Powder

- 5.2.3 Gas

- 5.3 By Crop Type

- 5.3.1 Fruits

- 5.3.2 Vegetables

- 5.3.3 Grains

- 5.3.4 Flowers and Ornamentals

- 5.4 By Origin

- 5.4.1 Natural

- 5.4.2 Synthetic

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta AG

- 6.4.2 AgroFresh Solutions, Inc.

- 6.4.3 Bayer AG

- 6.4.4 Decco Post-Harvest Inc. (UPL Limited)

- 6.4.5 Nufarm Limited

- 6.4.6 John Bean Technologies Corporation

- 6.4.7 Xeda International S.A.

- 6.4.8 Citrosol, S.A.

- 6.4.9 Fomesa Fruitech, S.L.U.

- 6.4.10 bio-ferm GmbH (Andermatt Group AG)

- 6.4.11 Lytone Enterprise, Inc.

- 6.4.12 Janssen PMP (Janssen Pharmaceutica NV)

7 Market Opportunities and Future Outlook