PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065433

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065433

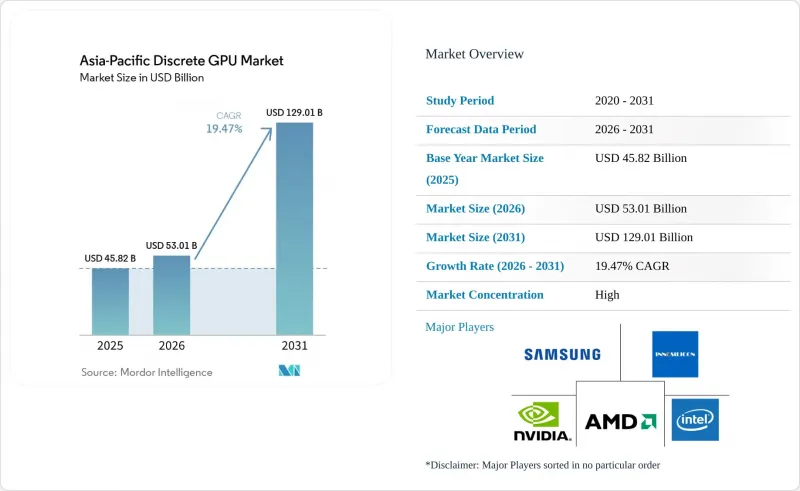

Asia-Pacific Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific discrete GPU market size is expected to grow from USD 45.82 billion in 2025 to USD 53.01 billion in 2026 and is forecast to reach USD 129.01 billion by 2031 at a 19.47% CAGR over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More), and Country (China, Japan, South Korea, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Discrete GPU Market Trends and Insights

Exponential Growth in AI Training and Inference Workloads

Parameter counts on large language models crossed the 1-trillion threshold in 2025, pushing compute density well beyond integrated-graphics capabilities. Meta contracted 6 gigawatts of AMD Instinct MI455X capacity in March 2026, while Oracle ordered 50,000 MI450 devices for its cloud estate. India earmarked USD 1.24 billion for 10,000 GPUs in 2025 and aims to reach 100,000 units by 2027 under its sovereign-compute agenda. Japan and South Korea have each budgeted roughly USD 4 billion to stand up exascale clusters, turning AI infrastructure into a strategic asset. These deployments shorten replacement cycles, front-load capital expenditure, and lift demand for top-tier accelerators featuring HBM3E memory and advanced packaging.

Rapid Expansion of Hyperscale Data Centers Across Asia-Pacific

AWS committed AUD 20 billion (USD 13 billion) to its Australian footprint, Microsoft reserved USD 2.9 billion for Japanese capacity, and Google pledged USD 3 billion for a Maharashtra facility delivering 200 megawatts by 2027. Singapore's 2025 DataCenter-First Framework allocated 200 megawatts but mandates 50% renewable power and a sub-1.3 PUE, effectively requiring liquid-cooled GPU racks that add 15-20% to capex. Tencent Cloud and Alibaba Cloud now package NVIDIA A100 instances with elastic billing, shifting discrete GPU purchases from enterprises to hyperscalers. These investments underpin a dense procurement cycle for H100 and MI300X boards, sustain demand in the Asia-Pacific discrete GPU market, and intensify supply-chain pressure on CoWoS capacity.

Ongoing Supply Chain Volatility for Advanced Process Nodes

By late 2026, TSMC's CoWoS line achieved a milestone of processing wafers monthly. However, NVIDIA secured a dominant share of that output, with AMD trailing, creating a tight squeeze for potential new entrants. H100 lead times stretched to 52 weeks in mid-2025, forcing customers into 18-24-month preorder windows that erode budgeting flexibility. Export-control ceilings of 4,800 H100 units per month for China diverted buyers to gray-market boards priced up to 60% above list or to lower-performance A800 variants requiring licenses. HBM supply remains tight as SK Hynix allocates 80% of HBM3E volume to NVIDIA, prompting a USD 13 billion expansion plan announced in March 2026, but relief arrives only after 2028. These bottlenecks weigh on the Asia-Pacific discrete GPU market by delaying deployments and inflating costs.

Other drivers and restraints analyzed in the detailed report include:

- National Initiatives for Domestic GPU Manufacturing in China and India

- Rising Popularity of AAA PC and Mobile Gaming Titles

- Intensifying Price Competition from Integrated GPUs in Entry-Level Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators generated 40.10% of 2025 revenue, underscoring the outsized role of AI training clusters built by hyperscalers and sovereign clouds. The Asia-Pacific discrete GPU market is projected to expand at a 19.73% CAGR through 2031 as enterprises repatriate inference from public clouds to cost-optimized on-premises racks. NVIDIA H100 and AMD MI300X boards, priced near USD 30,000 per unit, dominate new capacity even though unit volumes trail those of consumer cards. Workstation GPUs remain important for creators using CUDA and ROCm pipelines, while console demand stays stable on the back of Nintendo's expected late-2026 launch. Automotive adoption is nascent, yet Chinese EV makers such as BYD evaluate discrete modules for immersive cabin displays. Edge-industrial devices are a quiet growth pocket, pairing low-power boards with machine-vision workloads that CPUs cannot service.

Mainstream PC and notebook demand faces margin compression as integrated GPUs reach 80-90% of discrete performance at zero incremental bill-of-materials cost. Nevertheless, professional visualization rigs still prefer discrete cards for Adobe Premiere and Blender rendering. Gaming handhelds with hybrid architectures spur incremental volume, while research clusters in academia adopt surplus consumer cards when datacenter stockouts persist. The segment's blend of price-elastic consumer sales and inelastic datacenter buys helps stabilize overall revenue, even as shipment mix shifts toward accelerators. As policy mandates tighten data sovereignty, regional system integrators bundle turnkey racks with 700-watt GPUs, liquid cooling, and renewable-energy sourcing agreements, reinforcing long-run growth.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- ASUSTeK Computer Inc.

- Gigabyte Technology Co., Ltd.

- Micro-Star International Co., Ltd.

- Colorful Technology Company Limited

- Leadtek Research Inc.

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Innosilicon Technology (Shanghai) Co., Ltd.

- Biren Technology Co., Ltd.

- Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- Shanghai Tianshu Zhixin Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Asia Pacific Discrete GPU Market

- 4.2.2 Exponential Growth in AI Training and Inference Workloads

- 4.2.3 Rising Popularity of AAA PC and Mobile Gaming Titles

- 4.2.4 National Initiatives for Domestic GPU Manufacturing in China and India

- 4.2.5 Rapid Expansion of Hyperscale Data Centers Across Asia-Pacific

- 4.2.6 Integration of Discrete GPUs into Next-Gen Augmented Reality Glasses

- 4.2.7 Bundled GPU-as-a-Service Offerings by Regional Cloud Providers

- 4.3 Market Restraints

- 4.3.1 Ongoing Supply Chain Volatility for Advanced Process Nodes

- 4.3.2 Intensifying Price Competition from Integrated GPUs in Entry-Level Devices

- 4.3.3 Escalating Regional Energy Tariffs Hitting Datacenter GPU TCO

- 4.3.4 Cooling Infrastructure Limits in Dense Urban Datacenters

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 South Korea

- 5.4.4 India

- 5.4.5 Southeast Asia

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 ASUSTeK Computer Inc.

- 6.4.7 Gigabyte Technology Co., Ltd.

- 6.4.8 Micro-Star International Co., Ltd.

- 6.4.9 Colorful Technology Company Limited

- 6.4.10 Leadtek Research Inc.

- 6.4.11 Sapphire Technology Limited

- 6.4.12 Palit Microsystems Ltd.

- 6.4.13 Innosilicon Technology (Shanghai) Co., Ltd.

- 6.4.14 Biren Technology Co., Ltd.

- 6.4.15 Moore Threads Intelligent Technology (Beijing) Co., Ltd.

- 6.4.16 Shanghai Tianshu Zhixin Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment