PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065441

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065441

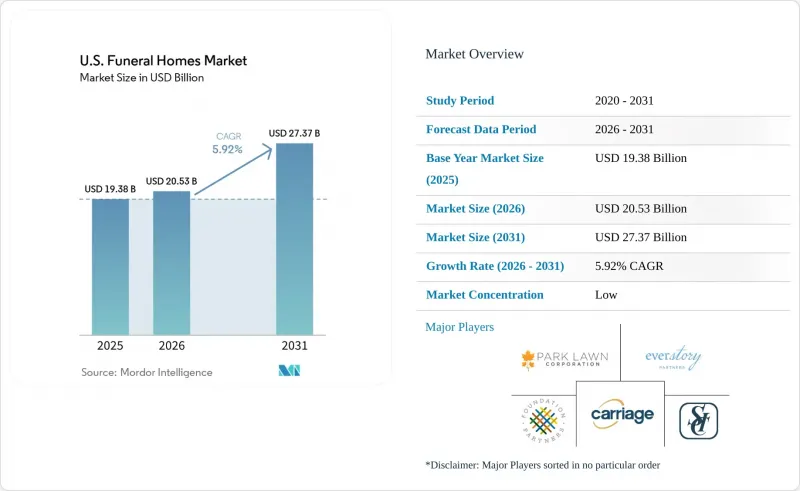

U.S. Funeral Homes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. funeral homes market size was valued at USD 19.38 billion in 2025 and is estimated to grow from USD 20.53 billion in 2026 to reach USD 27.37 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

This report is Segmented by Ownership Model (Family/Independently Owned, Local and Regional Private Chains, Public Consolidators, Nonprofit and Community-Owned), Arrangement Timing (At-Need, Preneed), and Disposition Type (Burial-Centered, Cremation-Centered, Alkaline Hydrolysis, Natural Organic Reduction). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Funeral Homes Market Trends and Insights

Aging Population and Rising Death Volumes Are Transitioning From Projection to Cash Flow

Demographic trends are now shaping the operational landscape of the United States funeral homes market. In 2024, 3,072,666 resident deaths were recorded, with a 3.8% decline in the age-adjusted death rate to 722.1 per 100,000. However, deaths among Americans aged 65 and older rose by 1.3%, highlighting the impact of an aging population. The first Baby Boomers will turn 80 in 2026, and the 75 to 90 age group will expand through the mid-2030s. Projections estimate annual deaths to reach 3.45 million by 2030 and 3.6 million by 2035, signaling sustained demand. Operators investing in staff, preneed sales, and family service systems are positioning for long-term growth. Mortality rates in the 60+ demographic remain consistent with aging trends, supporting a positive operational outlook.

Preneed Contract Growth Exposes a USD 3 Billion Addressable Gap

Preneed planning is driving revenue growth in the United States funeral homes market by improving demand timing and cash flow. In 2024, 535,503 preneed insurance policies were sold, with a gross face value of USD 3.04 billion, reflecting a 3.5% to 4% increase from 2023. Despite this, fewer than 22% of Americans over 55 who passed away had preneed arrangements, leaving over 78% of potential demand untapped. SCI's preneed backlog grew from USD 11.1 billion in 2019 to USD 17.0 billion by 2025, while Carriage Services reported a 27.4% rise in insurance-funded preneed contracts, showcasing the potential for structured sales growth.

Cremation-Led Ticket Compression Is the Primary Per-Case Revenue Headwind

The United States funeral homes market is experiencing revenue pressure due to the shift from traditional burials to cremations. The National Funeral Directors Association (NFDA) projects a cremation rate of 63.4% in 2025, while the Cremation Association of North America (CANA) reported a 2024 rate of 61.8%, with an expected increase to 67.9% by 2029. A median cremation service generates USD 6,280 compared to USD 7,848 for a burial, creating a USD 1,568 gap per case. This gap is challenging to offset as core costs like labor and facilities remain fixed. Operators not offering additional services, such as memorialization or premium options, may see volume growth without corresponding margin increases. The FTC Funeral Rule further limits pricing flexibility by requiring itemized disclosures and restricting bundling.

Other drivers and restraints analyzed in the detailed report include:

- Personalization and Celebration-of-Life Spending Are Redefining Per-Case Revenue

- Succession-Driven Consolidation Is Compressing the Independent Segment's Timeline

- Licensed Labor Scarcity Creates a Structural Capacity Ceiling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, family- and independently owned operators accounted for 75.25% of revenue, maintaining their leadership in the United States funeral homes market despite ongoing consolidation. Their success stems from community trust, generational referrals, and familiarity during critical decisions.

Public consolidators are projected to grow at a 7.28% CAGR through 2031, driven by access to capital, centralized procurement, advanced technology budgets, and resource flexibility. SCI's 2026 capital plan allocated USD 25 million for digital investments, a level unattainable for many independents. Many independents prioritized debt reduction over modernization in 2020-2021, widening the capability gap. This has created a divide between strong independents with local differentiation and weaker operators facing succession pressures, compliance costs, and acquisition offers.

List of Companies Covered in this Report:

- Carriage Services, Inc.

- Casper Funeral & Cremation Services

- Everstory Partners

- Family First Funeral Homes & Cremation Care

- Foundation Partners Group

- Heritage Family

- Indiana Memorial Group

- Jersey Memorial Group

- Memorial Traditions

- Newcomer Funeral Service Group

- Park Lawn Corporation

- Rollings Funeral Service

- Security National Financial Corporation

- Service Corporation International

- Southern Cremations & Funerals

- Turrentine-Jackson-Morrow

- Vertin

- Walker Funeral Homes and Crematory

- Weeks' Funeral Homes

- Wilson-Shook Funeral Homes and Cremation Center

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Death Volumes

- 4.2.2 Preneed Contract Growth

- 4.2.3 Personalization and Celebration-Of-Life Spend

- 4.2.4 Succession-Driven Consolidation

- 4.2.5 Hybrid Online-Offline Arrangement Adoption

- 4.3 Market Restraints

- 4.3.1 Cremation-Led Ticket Compression

- 4.3.2 Licensed Labor Scarcity

- 4.3.3 FTC Price Transparency Enforcement

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Ownership Model

- 5.1.1 Family- and Independently Owned Funeral Homes

- 5.1.2 Local and Regional Private Chains

- 5.1.3 Public Consolidators

- 5.1.4 Nonprofit and Community-Owned Operators

- 5.2 By Arrangement Timing

- 5.2.1 At-Need Services

- 5.2.2 Preneed Services

- 5.3 By Disposition Type

- 5.3.1 Burial-Centered Services

- 5.3.2 Cremation-Centered Services

- 5.3.3 Alkaline Hydrolysis Services

- 5.3.4 Natural Organic Reduction Services

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Carriage Services, Inc.

- 6.3.2 Casper Funeral & Cremation Services

- 6.3.3 Everstory Partners

- 6.3.4 Family First Funeral Homes & Cremation Care

- 6.3.5 Foundation Partners Group

- 6.3.6 Heritage Family

- 6.3.7 Indiana Memorial Group

- 6.3.8 Jersey Memorial Group

- 6.3.9 Memorial Traditions

- 6.3.10 Newcomer Funeral Service Group

- 6.3.11 Park Lawn Corporation

- 6.3.12 Rollings Funeral Service

- 6.3.13 Security National Financial Corporation

- 6.3.14 Service Corporation International

- 6.3.15 Southern Cremations & Funerals

- 6.3.16 Turrentine-Jackson-Morrow

- 6.3.17 Vertin

- 6.3.18 Walker Funeral Homes and Crematory

- 6.3.19 Weeks' Funeral Homes

- 6.3.20 Wilson-Shook Funeral Homes and Cremation Center

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment