PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065454

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065454

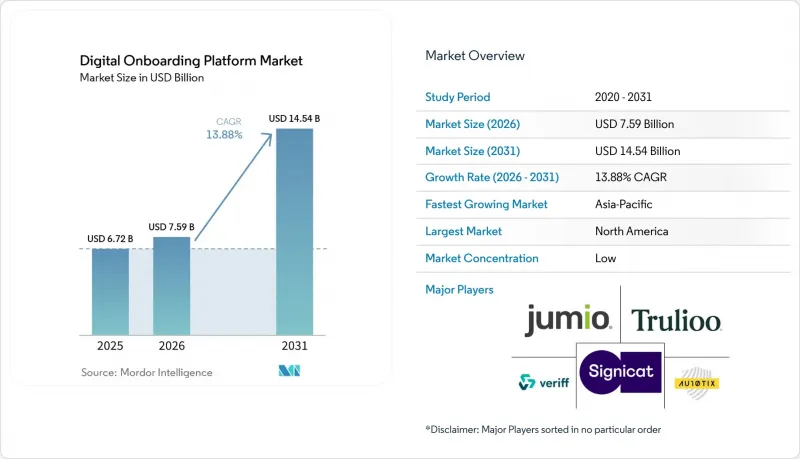

Digital Onboarding Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the digital onboarding platform market size is projected to be USD 6.72 billion in 2025, USD 7.59 billion in 2026, and reach USD 14.54 billion by 2031, growing at a CAGR of 13.88% from 2026 to 2031.

This report is Segmented by Component (Software Platforms, and Services), Deployment Model (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Onboarding Process Type (Customer Onboarding, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Onboarding Platform Market Trends and Insights

Acceleration of Remote and Mobile-First Account Opening

Remote onboarding is now judged by completion speed as much as by control strength in the digital onboarding platform market. That shift is spreading beyond banking, as Aetna launched a digital-first benefits onboarding experience for 4 million members in February 2026. Jumio expanded its reusable identity solution to include selfies across South America in April 2026, which shows vendor investment in repeat verification journeys with less friction for returning users. Interac also moved to strengthen national digital onboarding flows in Canada in May 2026 through a collaboration with Incode that adds deepfake and injection-attack defenses. Mobile users are less willing to tolerate long review queues, so providers are redesigning onboarding journeys for fast capture, low friction, and immediate routing. As more enrollment journeys begin on phones, completion rates are increasingly tied to account growth, enrollment volume, and service activation.

Other drivers and restraints analyzed in the detailed report include:

- Tightening KYC, AML, and Customer Due Diligence Mandates

- Rising Synthetic Identity, Deepfake, and Account Opening Fraud

- Shift to Cloud-Native and API-First Onboarding Orchestration

- Regulatory Fragmentation and Biometric Privacy Compliance Burden

- Legacy Core-System Integration Complexity and Implementation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment captured 71.29% of the digital onboarding platform market share in 2025, making it the leading deployment model. Buyers favored cloud because it lowers upfront infrastructure needs and shortens the path to live verification. The cloud model also enables vendors to distribute model updates for liveness checks, fraud detection, and document verification to many customers simultaneously. That matters in environments where attack methods are changing more quickly than traditional software release cycles. It also helps explain why cloud deployment remained attractive even for institutions that still maintain large legacy estates elsewhere.

Hybrid deployment is projected to expand at a 14.73% CAGR through 2031, showing that many buyers are building bridges rather than making full exits from on-premises systems. That pattern is strongest where institutions need cloud speed but must keep sensitive identity data, encryption controls, or approval records within local boundaries. IBM's May 2026 launch of IBM Sovereign Core highlights how suppliers are trying to support that middle path with jurisdiction-bound cloud operations. In the digital onboarding platform market, hybrid is becoming a strategic operating model rather than a temporary compromise. On-premises deployment still holds niche relevance for high-security use cases, but most growth is now centered on architectures that mix cloud orchestration with controlled local data handling.

Large enterprises accounted for 63.41% of the market in 2025, making them the largest spending cohort in the digital onboarding platform market. Their lead came from larger contract values, multi-country compliance requirements, and more complex onboarding volumes across employees, customers, and third parties. Large organizations were also earlier adopters because they had the budget and governance structures needed to justify formal identity orchestration projects. Their deployments often span several workflows, which makes vendor relationships broader and harder to displace. That helps explain why enterprise accounts still account for a large share of revenue, even as newer buyer groups enter the market.

SMEs are projected to grow at a 16.87% CAGR through 2031, showing that identity orchestration is moving downmarket within the digital onboarding platform market. This shift is tied to embedded finance, partner onboarding, and software-led distribution of compliance tasks that smaller firms did not previously handle themselves. Modern Treasury and Persona announced a partnership in April 2026 to strengthen business onboarding and compliance, reflecting the need for easier API-based KYB workflows in payment operations. Veriff's February 2026 acquisition of Vespia also supports this direction by expanding from individual verification into real-time business verification across more than 300 jurisdictions. As regulated services spread through vertical software and platform ecosystems, smaller businesses are becoming meaningful buyers rather than edge cases in the digital onboarding platform market.

Geography Analysis

North America held 39.73% of the digital onboarding platform market share in 2025, keeping it as the largest regional segment. The United States remained central because it combined regulated financial institutions, enterprise HR software demand, and a deep vendor base in identity verification and fraud detection. FinCEN's April 2026 AML and CFT reform proposal is pushing institutions to review whether legacy onboarding controls can meet a more outcome-focused standard of risk-based effectiveness. In Canada, Interac announced a May 2026 collaboration with Incode to add iBeta Level 3-validated liveness, deepfake detection, and injection-attack defense to Interac Verified solutions, signaling national-level investment in stronger digital onboarding infrastructure.

Asia-Pacific is projected to grow at a 19.13% CAGR through 2031, making it the fastest-growing regional segment in the digital onboarding platform market. Growth is being supported by mobile-first users, expanding fintech ecosystems, and stronger links between digital identity infrastructure and commercial onboarding flows. In Japan, LIQUID eKYC supported Seven Bank's foreign account opening process through IC chip-based identity verification, reducing dependence on manual document capture for some user groups. That combination of mobile use, identity infrastructure, and platform-led service delivery continues to make Asia-Pacific one of the most active regions for the adoption of new onboarding models.

Europe held a significant share of the market in 2025, with Germany and the United Kingdom as major sub-markets. Germany advanced its legal framework for the European Digital Identity Wallet in 2026 through the Digitales-Identitaten-Gesetz, supporting the next phase of national wallet deployment. The broader European Digital Identity framework is also shaping how onboarding platforms prepare for wallet-based identity exchange and interoperable trust services. South America is gaining relevance as reusable identity models spread, with Jumio extending selfie across the region in April 2026. The Middle East and Africa remained smaller in absolute terms, but adoption continued to improve as vendors localized their products and governments expanded digital identity efforts.

- Jumio Corporation

- Trulioo Information Services Inc.

- Signicat AS

- Veriff OU

- Au10tix Ltd.

- IDnow GmbH

- Sum and Substance Ltd.

- Shufti Pro Limited

- Persona Identities, Inc.

- Socure Inc.

- First Mile Group, Inc. d/b/a Alloy

- Mitek Systems, Inc.

- Ondato UAB

- UAB iDenfy

- PXL Vision AG

- Innovatrics, s.r.o.

- Incode Technologies, Inc.

- ID.me, LLC

- Intellicheck, Inc.

- HyperVerge Technologies Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening KYC, AML, and Customer Due Diligence Mandates

- 4.2.2 Acceleration of Remote and Mobile-First Account Opening

- 4.2.3 Rising Synthetic Identity, Deepfake, and Account Opening Fraud

- 4.2.4 Shift to Cloud-Native and API-First Onboarding Orchestration

- 4.2.5 Emergence of Reusable Digital Identity Wallets and Verifiable Credentials

- 4.2.6 Embedded Finance and Platform-Led Multi-Party Onboarding Demand

- 4.3 Market Restraints

- 4.3.1 Regulatory Fragmentation and Biometric Privacy Compliance Burden

- 4.3.2 Legacy Core-System Integration Complexity and Implementation Cost

- 4.3.3 Gray-Zone Review Queues From AI Spoof Edge Cases and Model Governance

- 4.3.4 Data Localization and Sovereign Cloud Requirements

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Onboarding Process Type

- 5.4.1 Customer Onboarding

- 5.4.2 Employee Onboarding

- 5.4.3 Vendor and Supplier Onboarding

- 5.4.4 Partner and Merchant Onboarding

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Jumio Corporation

- 6.4.2 Trulioo Information Services Inc.

- 6.4.3 Signicat AS

- 6.4.4 Veriff OU

- 6.4.5 Au10tix Ltd.

- 6.4.6 IDnow GmbH

- 6.4.7 Sum and Substance Ltd.

- 6.4.8 Shufti Pro Limited

- 6.4.9 Persona Identities, Inc.

- 6.4.10 Socure Inc.

- 6.4.11 First Mile Group, Inc. d/b/a Alloy

- 6.4.12 Mitek Systems, Inc.

- 6.4.13 Ondato UAB

- 6.4.14 UAB iDenfy

- 6.4.15 PXL Vision AG

- 6.4.16 Innovatrics, s.r.o.

- 6.4.17 Incode Technologies, Inc.

- 6.4.18 ID.me, LLC

- 6.4.19 Intellicheck, Inc.

- 6.4.20 HyperVerge Technologies Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment