PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065502

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065502

LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

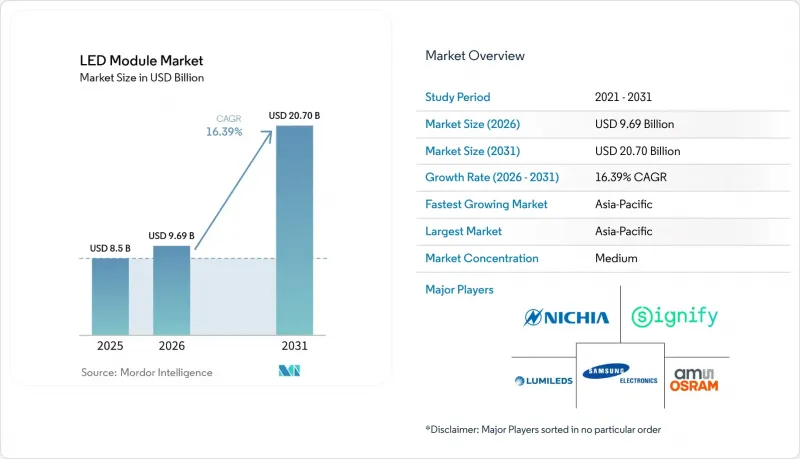

According to Mordor Intelligence, the lED module market size was USD 8.50 billion in 2025 and USD 9.69 billion in 2026, and is expected to reach USD 20.70 billion by 2031, growing at a CAGR of 16.39% over 2026-2031.

This report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), Form Factor (Rigid, and Flexible), and Geography (North America, Europe, and Other Geographies). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Module Market Trends and Insights

Smart-Lighting Integration With IoT-Enabled Building Systems

Commercial construction increasingly embeds networked lighting that treats every LED module as an intelligent edge device collecting occupancy, daylight, and health telemetry. In 2025, sixty percent of new floor space commissioned in North America and Europe funded wireless gateways, sensor arrays, and cloud subscriptions worth more than USD 550 000 per site. Measured savings of 30 to 40 percent on electricity and maintenance deliver sub-three-year paybacks, satisfying CFO hurdle rates. The new Matter protocol unifies Zigbee, Thread, and proprietary meshes, slashing commissioning time and calls. Predictive analytics schedule replacements before outages, lifting tenant satisfaction and landlord valuation premiums.

Government-Mandated Phase-Out of Inefficient Light Sources

Legislators on three continents are compressing compliance timelines, converting what was a voluntary efficiency upgrade into a statutory requirement. The European Union banned most halogen stock-keeping units in 2021 and heightened customs enforcement in 2024, blocking non-compliant imports at ports. California's 2025 Title 24 revision stipulates that 90 percent of installed lighting power in new commercial buildings must originate from LED sources equipped with occupancy sensors and daylight harvesting. China's 2024 roadmap demands public infrastructure luminaires exceeding 130 lumens per watt by 2026. These synchronized decrees guarantee sustained demand for modular LED retrofit kits and integrated ceiling panels.

Thermal Management Challenges in High-Power Modules

High-power modules operating above 30 watts struggle to shed the heat generated by tightly packed emitters, and junction temperatures that drift beyond 125 °C can cut luminous output in half within a few thousand hours. Meeting new IEC 62031:2026 thermal resistance reporting rules forces suppliers to invest in infrared imaging, finite element simulation, and more expensive metal core or ceramic substrates. Passive heat sinks add weight and volume, while active fans raise noise and reliability worries. Horticulture and industrial luminaires feel the impact first because ambient temperatures already sit high, amplifying warranty claims and deterring aggressive overdrive strategies among buyers.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift to LED Headlamps and Interior Modules

- Rapid LED Penetration in Residential and Commercial Retrofits

- Price-Erosion and Margin Pressure Owing to Excess Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED backlight modules are advancing at a 16.81% CAGR from 2026-2031, significantly outpacing overall LED module market growth as Mini-LED technology scales into premium televisions and monitors. SMD modules retained 33.61% of the LED module market share in 2025, buoyed by strong cost-performance in residential and commercial luminaires. Backlight designs tap thousands of Mini-LEDs to achieve greater-than 1,000 local-dimming zones, pushing demand for thin, thermally efficient boards. Meanwhile, chip-on-board (COB) architectures win in automotive headlamps where compact footprints meet 10,000-lumen targets without enlarging reflector housings. Linear modules continue to dominate office troffer retrofits because contractors can replace fluorescent lamps without rewiring, preserving tight project timelines.

The LED module market benefits from new specialty niches: flexible strips illuminate curved signage, and UV-C modules expand into healthcare. COB's monolithic die reduces thermal resistance and elevates color rendering above 90, fitting museum and retail needs. Cree LED's L2 PCBA platform packages this benefit with integrated drivers, thereby trimming luminaire OEM design cycles. As automation lowers Mini-LED cost, backlight modules will progressively steal share from SMD in high-brightness displays, reinforcing a mixed portfolio strategy for suppliers.

General lighting represented 42.59% of the LED module market size in 2025, yet is ceding relative momentum to display and backlighting, forecast to climb at a 16.98% CAGR through 2031. Direct-lit TV and gaming-monitor refresh cycles fuel replacement demand, while HDR-ready panels push local-dimming counts upward, inflating module content per screen. Commercial lighting still absorbs the largest module volume via office, retail, and hospitality retrofits, but energy regulations are flattening growth relative to screen-based segments.

Automotive exterior lighting, especially adaptive headlamps, commands premium pricing due to rigorous photometric testing. Signage and outdoor advertising install high-brightness modules rated above 5,000 nits and protected to IP65, sustaining demand from smart-city projects. Horticulture and UV-C disinfection form high-margin verticals where spectral tuning or germicidal wavelengths offset lower shipment volumes. Each niche enlarges the addressable LED module market even as the bulb segment matures.

Geography Analysis

Asia-Pacific accounted for 67.73% of the LED module market revenue in 2025 and is projected to post a 17.05% CAGR through 2031. China controls more than 70% of global chip capacity and continues to expand; BOE Huacan's RMB 2 billion (USD 280 million) wafer plant in Jiangsu will add 500,000 pieces per month, aimed at automotive and Mini-LED backlights BOE.COM. India is emerging as a secondary hub as public-sector street-light tenders scale into the tens of millions of units. Japan retains leadership in UV and micro-LED specialties, leveraging Nichia's phosphor patents to command price premiums.

North America ranks second by revenue, sustained by regulatory bans on fluorescent ballasts and the accelerating adoption of adaptive LED headlamps. Canada's rising carbon price moved building owners to allocate 40% of retrofit budgets to lighting upgrades, while Mexican states near the U.S. border expanded module-assembly capacity by 25% during 2025 to serve nearshoring OEMs.

Europe's strict Ecodesign thresholds guarantee a steady retrofit cadence, with Germany and the United Kingdom spearheading office and municipal conversions. Middle East and Africa markets concentrate on prestige smart-city districts in the United Arab Emirates and Saudi Arabia, whereas South America and Africa see sporadic demand tied to off-grid solar-LED programs. Across all regions, policy pressure and local manufacturing incentives intersect to keep the LED module market on a high-growth trajectory.

- Signify N.V.

- ams-OSRAM AG

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- Cree LED, Inc.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Acuity Brands, Inc.

- Eaton Corporation plc

- General Electric Company

- Toyoda Gosei Co., Ltd.

- Bridgelux, Inc.

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Epistar Corporation

- Opple Lighting Co., Ltd.

- Hubbell Incorporated

- Dialight plc

- Zhejiang Yankon Group Co., Ltd.

- Edison Opto Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED Penetration in Residential and Commercial Retrofits

- 4.2.2 Smart-Lighting Integration with IoT-Enabled Building Systems

- 4.2.3 Government-Mandated Phase-Out of Inefficient Light Sources

- 4.2.4 Automotive OEM Shift to LED Headlamps and Interior Modules

- 4.2.5 Miniaturised & Flexible Modules Enabling New Form-Factors

- 4.2.6 On-Board Driver IC Adoption Reducing System BOM Cost

- 4.3 Market Restraints

- 4.3.1 Price-Erosion and Margin Pressure Owing to Excess Capacity

- 4.3.2 Thermal Management Challenges in High-Power Modules

- 4.3.3 Semiconductor Supply-Chain Volatility for Key Epitaxy Wafers

- 4.3.4 Absence of Universal Module-Level Safety Standards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB (Chip-on-Board) LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Linear LED Modules

- 5.1.4 LED Backlight Modules

- 5.1.5 High-Power LED Modules

- 5.1.6 Others, Module Type (Flexible, Mini, Custom Assemblies)

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.2 Residential

- 5.2.3 Commercial

- 5.2.4 Industrial

- 5.2.5 Automotive Lighting

- 5.2.6 Display and Backlighting

- 5.2.7 Signage and Advertising

- 5.2.8 Others, Application (Architectural, Horticulture, UV, Specialty)

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED Modules

- 5.4.2 Flexible LED Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East

- 5.5.6 Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 ams-OSRAM AG

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Nichia Corporation

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Cree LED, Inc.

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Acuity Brands, Inc.

- 6.4.10 Eaton Corporation plc

- 6.4.11 General Electric Company

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Citizen Electronics Co., Ltd.

- 6.4.15 Everlight Electronics Co., Ltd.

- 6.4.16 Epistar Corporation

- 6.4.17 Opple Lighting Co., Ltd.

- 6.4.18 Hubbell Incorporated

- 6.4.19 Dialight plc

- 6.4.20 Zhejiang Yankon Group Co., Ltd.

- 6.4.21 Edison Opto Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment