PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065503

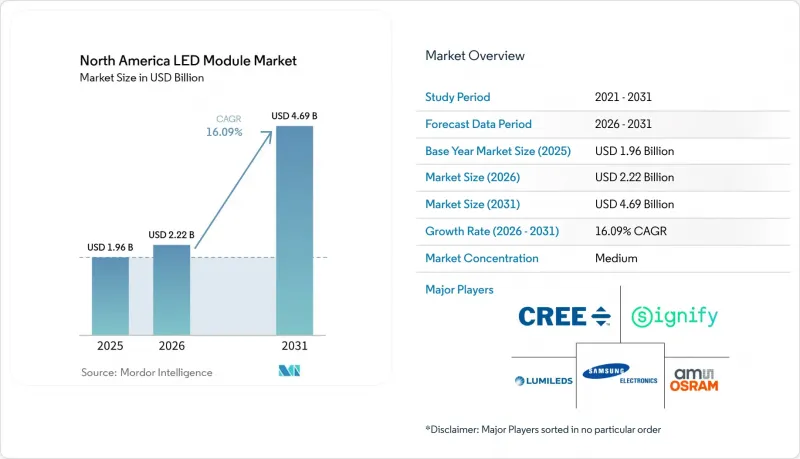

North America LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america lED module market size is projected to expand from USD 1.96 billion in 2025 and USD 2.22 billion in 2026 to USD 4.69 billion by 2031, registering a CAGR of 16.09% between 2026 to 2031.

This report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid, and Flexible). The Market Forecasts are Provided in Terms of Value (USD).

North America LED Module Market Trends and Insights

Surge in Ultraviolet-C LED Modules for Disinfection Systems

The U.S. Environmental Protection Agency's 2024 guidance recognized UV-C LEDs for 4-log virus inactivation in water treatment, removing a longstanding regulatory hurdle. As a result, municipalities in Arizona, Florida, and British Columbia issued tenders in 2025 that specify mercury-free UV-C arrays, displacing low-pressure mercury lamps in new installations. LG Innotek and Seoul Viosys each launched 100 milliwatt single-chip emitters capable of 10,000-hour L70 performance, enabling compact point-of-use purifiers. Although radiant-flux efficacy remains below 5%, rapid ASP declines and form-factor flexibility have attracted venture funding into U.S. start-ups focusing on HVAC airstream sanitization. Suppliers with verified LM-80 test data and NSF-61 listings command price premiums above visible-spectrum products, lifting overall margin mix for the North America LED module market.

Automaker Shift to LED Headlamps Across Mid-range Vehicle Lines

National Highway Traffic Safety Administration approval of adaptive driving beams in 2024 unlocked LED matrix headlamp deployments across mid-priced sedans and crossovers. Magna's FlecsForm mini-LED module, introduced in 2025, reduces package height by 15 millimeters, enabling automakers to restyle front fascias without compromising pedestrian-impact compliance. Concurrently, Tianma and Innolux showcased mini-LED head-up displays hitting 12,000 nits, a performance level requiring high-power backlight boards with micro-optics for glare control. The migration downstream from luxury trims expands annual unit demand for automotive-grade modules rated to survive 125 °C junction temperatures and AEC-Q102 shock standards. Flexible interior ambient strips using RGBW arrays are now specified in pickup trucks retailing below USD 40,000, further widening volume opportunities.

Thermal Management Challenges in High-Power Modules

Outdoor area lighting and industrial high-bays now exceed 30 watts per board, intensifying junction temperatures beyond 115 °C under summer peak loads. DLC V6.0 demands L70 to 50,000 hours and, for the Premium tier, L90 to 36,000 hours, forcing suppliers to adopt liquid-cooling plates or phase-change housings. Getian's 2025 liquid-cooled modules dissipate 100-watt loads yet raise fixture BOM by 30%. Passive alternatives like CooliBlade phase-change fins lower junctions but enlarge luminaire envelopes, clashing with slim-line architectural aesthetics. Without robust thermal models and on-board sensors, warranty claims escalate, eroding brand equity.

Other drivers and restraints analyzed in the detailed report include:

- IoT-Enabled Smart-Building Codes Mandating Connected Luminaires

- Expanding Utility Rebates Accelerating LED Retrofit Projects

- Price Volatility of GaN and Sapphire Substrates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD boards captured 31.29% of the North America LED module market share in 2025, supported by mass-manufactured troffers, downlights, and strip fixtures. SMD's low profile and reflow-solder economy align with contract manufacturing across Mexico and the southern United States. In contrast, LED backlight modules are forecast to post a 16.57% CAGR, fueled by mini-LED and micro-LED panels that pack more than 200,000 dimming zones. The North America LED module market size tied to premium television backlights is expanding as panel makers localize assembly to sidestep semiconductor tariffs. Two hundred square-inch automotive displays, each requiring upwards of 5,000 mini-LEDs, are pulling specialty suppliers into long-term vehicle platforms.

Contention between COB and advanced SMD continues: COB downlights reach 155 lumens per watt, but high-density SMD arrays now pass 181 lumens per watt, leveraging flip-chip packages. Flexible strips built on copper-polyimide laminates occupy a niche for curved dashboards and retail accent lighting, commanding ASPs 2-3 times those of rigid FR-4 boards. DLC listing pathways for modular products make it easier for luminaire brands to qualify families built around common SMD engines, reinforcing SMD's incumbent momentum while specialty backlight boards deliver the highest growth delta.

General lighting maintained 44.68% of 2025 revenue, reflecting decades-deep retrofit activity and code compliance in offices, warehouses, and streetscapes. The segment benefits from standardized utility incentives and bundled sensor packages that streamline payback modeling. Yet display and backlighting is projected to expand at 16.78% CAGR, a pace nearly 2 percentage points above the overall North America LED module market. Television OEMs are upgrading 65-inch and larger sets to mini-LED, boosting individual panel demand to 10,000-plus emitters. Automotive cockpits adopt curved mini-LED HUDs rated at 12,000 nits, tightening tolerances on chromaticity and uniformity.

Horticulture, UV, and automotive adaptive systems round out smaller, high-margin slices. Hospitals specify UV-C downlights for occupied-room disinfection cycles, while vertical farmers invest in red-blue-far-red spectra tuned to lettuce and micro-greens. These specialized modules deliver gross margins north of 35%, double those of commodity troffer engines, a dynamic that helps offset pricing erosion in the general lighting core.

List of Companies Covered in this Report:

- Lumileds Holding B.V.

- Cree, Inc.

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Osram GmbH

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Signify N.V.

- Bridgelux, Inc.

- Acuity Brands, Inc.

- Eaton Corporation plc (Cooper Lighting Solutions)

- GE Current, a Daintree company

- Citizen Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Panasonic Holdings Corporation

- Toshiba Corporation

- Sharp Corporation

- Lextar Electronics Corporation

- Lumens Co., Ltd.

- Delta Electronics, Inc.

- Toyoda Gosei Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Utility Rebates Accelerating LED Retrofit Projects

- 4.2.2 Surge in Ultraviolet-C LED Modules for Disinfection Systems

- 4.2.3 Automaker Shift to LED Headlamps Across Mid-range Vehicle Lines

- 4.2.4 IoT-Enabled Smart-Building Codes Mandating Connected Luminaires

- 4.2.5 Rapid Growth of Indoor Vertical-Farming Driving Horticulture Lighting

- 4.2.6 Next-Gen Mini- and Micro-LED Backlights in Consumer Displays

- 4.3 Market Restraints

- 4.3.1 Price Volatility of GaN and Sapphire Substrates

- 4.3.2 Thermal Management Challenges in High-Power Modules

- 4.3.3 Supply-Chain Concentration in Asia-Pacific Creating Lead-Time Risks

- 4.3.4 Complexity of North American UL and DLC Certification Pathways

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Linear LED Modules

- 5.1.4 LED Backlight Modules

- 5.1.5 High-Power LED Modules

- 5.1.6 Others, Module Type (Flexible Modules, Mini Modules, Custom Assemblies)

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.1.3 Industrial

- 5.2.2 Automotive Lighting

- 5.2.3 Display and Backlighting

- 5.2.4 Signage and Advertising

- 5.2.5 Others, Application (Architectural, Horticulture, UV, Specialty Lighting)

- 5.2.1 General Lighting

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED Modules

- 5.4.2 Flexible LED Modules

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Lumileds Holding B.V.

- 6.4.2 Cree, Inc.

- 6.4.3 Nichia Corporation

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Osram GmbH

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 Signify N.V.

- 6.4.9 Bridgelux, Inc.

- 6.4.10 Acuity Brands, Inc.

- 6.4.11 Eaton Corporation plc (Cooper Lighting Solutions)

- 6.4.12 GE Current, a Daintree company

- 6.4.13 Citizen Electronics Co., Ltd.

- 6.4.14 Everlight Electronics Co., Ltd.

- 6.4.15 Panasonic Holdings Corporation

- 6.4.16 Toshiba Corporation

- 6.4.17 Sharp Corporation

- 6.4.18 Lextar Electronics Corporation

- 6.4.19 Lumens Co., Ltd.

- 6.4.20 Delta Electronics, Inc.

- 6.4.21 Toyoda Gosei Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment