PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065504

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065504

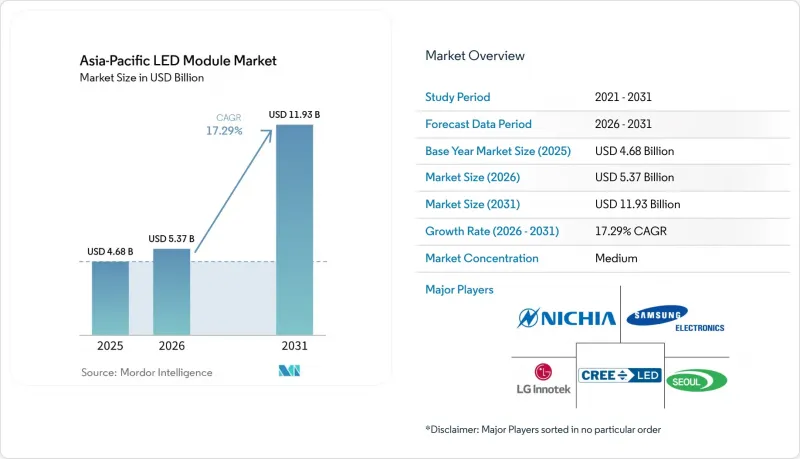

Asia-Pacific LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific lED module market size is expected to increase from USD 4.68 billion in 2025 to USD 5.37 billion in 2026 and reach USD 11.93 billion by 2031, growing at a CAGR of 17.29% over 2026-2031.

This report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid, and Flexible), and Country (China, Japan, India and Rest of Asia- Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific LED Module Market Trends and Insights

Rapid Decline in High-Power LED Cost per Lumen

Wafer-scale yields jumping from 25% to 75% pushed package cost per kilolumen down by 95% between 2003 and 2020. Recent chip-on-board (COB) portfolio upgrades lifted luminous flux 5-8% at unchanged prices, further shrinking dollar per lumen metrics. These savings unlock use cases once blocked by payback hurdles, such as 100,000-lumen stadium floods and 3.0 µmol J-1 horticulture fixtures. Chinese chip fabs drove module-level cost drops near 40% in 2025 on sub-P1.0 fine-pitch displays, hitting 99.99% die-transfer yields. Legacy suppliers must now pivot toward adaptive driving beam headlamps or micro-LED cinema screens to escape price wars.

Expansion of Smart Lighting Ecosystems in Commercial Buildings

Asia-Pacific building-automation investments are expanding at double-digit rates, and smart lighting sits at the heart of occupancy sensing and daylight harvesting strategies. Demonstrated energy savings of 40-60% in wired or wireless retrofits have convinced property owners in Singapore, Shanghai, and Mumbai to specify controllable Asia-Pacific LED module market SKUs. Municipal pilots like Taoyuan's 6,000-pole project validate large-scale deployments using DALI-2 and Bluetooth mesh. Module vendors embedding radios and sensors enjoy a systems-level premium while partnering with building-management integrators to guarantee compliance with India's code requirements.

Supply-Chain Concentration of Key Phosphor Materials

China refines more than 80% of global lanthanum, yttrium, europium, and cerium feedstock, and its October 2025 export license mechanism extends lead times by 45 days. Phosphor powders jumped 30% in late 2025, trimming gross margin by up to three points for buyers lacking long contracts. Inventories have ballooned to 90-120 days, locking working capital and heightening obsolescence risk if RGB COB stacks mature. Mining projects in Australia and Vietnam will not materially diversify supply before 2028.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Mini-LED Backlighting for High-End Displays

- Accelerating Phase-Out of Fluorescent Lighting Mandates

- Persistent Thermal Management Challenges in High-Power Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD boards captured 31.29% of the Asia-Pacific LED module market share in 2025, supported by mass-manufactured troffers, downlights, and strip fixtures. Shipment trends confirm that the Asia-Pacific LED module market remains anchored in SMD architectures, which accounted for one-third of 2025 regional revenue. SMD arrays dissipate heat across multiple junctions, tolerate automated high-speed placement exceeding 50,000 components per hour, and meet efficacy targets up to 181 lm W-1 without active cooling. The Asia-Pacific LED module market size, attributed to backlight modules, is expanding fastest, propelled by mini-LED television orders and double-digit growth in automotive cockpits. Chip-on-board entries, although still a minority, offer flux densities up to 8,000 lumens from a single emitter, ideal for museum spots, adaptive headlamps, and cinema projection.

Competitive positioning is diverging. SMD providers face commodity erosion as new Chinese entrants match performance at lower costs, whereas COB specialists shield margins through proprietary ceramic substrates and reflective coatings. Linear replacement boards remain resilient in commercial retrofits, while flexible strips migrate toward ambient lighting and curved signage duties. Suppliers that invest in no-wire interconnects and high-thermal conductivity composites are winning design-ins for next-generation automotive arrays.

General lighting still supplied 44.68% of 2025 demand across residential, commercial, and industrial premises, but its growth decelerates as household penetration in tier-1 cities surpasses 60%. The Asia-Pacific LED module market share weighted to display backlighting is climbing at a 17.58% CAGR, reflecting premium television diffusion and instrument-cluster upgrades in electric vehicles. Industrial buyers pursue high-bay modules with >140 lm W-1 efficacy and 100,000-hour lifetimes to curb maintenance at 10-m ceiling heights. Automotive lighting expands briskly thanks to pixelated headlamps and animated exterior signals that require millisecond response times.

Smart-ready commercial luminaires bundle Bluetooth mesh or Zigbee radios, tilting the specification in favor of vendors with embedded driver and sensing know-how. Fine-pitch digital signage drops below P1.0 mm, allowing outdoor billboards and in-store kiosks to rival LCD video walls in perceived resolution. Module makers differentiating through optical films and spectrum-tuning algorithms can lock in sticky revenues as retailers demand high color rendering for merchandise illumination.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED, a Smart Global Holdings Company

- Lumileds Holding B.V.

- Osram GmbH

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Lite-On Technology Corporation

- Stanley Electric Co., Ltd.

- Sharp Corporation

- Citizen Electronics Co., Ltd.

- Lextar Electronics Corporation

- Toyoda Gosei Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- MLS Co., Ltd.

- Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Phase-Out of Fluorescent Lighting Mandates

- 4.2.2 Rapid Decline in High-Power LED Cost per Lumen

- 4.2.3 Expansion of Smart Lighting Ecosystems in Commercial Buildings

- 4.2.4 Surge in Mini-LED Backlighting for High-End Displays

- 4.2.5 Localization Incentives Under China's Five-Year Plan

- 4.2.6 Growing VC Funding for Horticulture-Specific LED Modules

- 4.3 Market Restraints

- 4.3.1 Persistent Thermal Management Challenges in High-Power Modules

- 4.3.2 Supply-Chain Concentration of Key Phosphor Materials

- 4.3.3 Stringent Automotive EMC Compliance Costs

- 4.3.4 Plateauing Retrofit Demand in Tier-1 Cities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB (Chip-on-Board) LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Linear LED Modules

- 5.1.4 LED Backlight Modules

- 5.1.5 High-Power LED Modules

- 5.1.6 Others, Module Type

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.1.3 Industrial

- 5.2.2 Automotive Lighting

- 5.2.3 Display and Backlighting

- 5.2.4 Signage and Advertising

- 5.2.5 Others, Application

- 5.2.1 General Lighting

- 5.3 By Power Range

- 5.3.1 Low Power (less than or equal to 5 W)

- 5.3.2 Mid Power (greater than 5 W to less than or equal to 30 W)

- 5.3.3 High Power (greater than 30 W)

- 5.4 By Form Factor

- 5.4.1 Rigid LED Modules

- 5.4.2 Flexible LED Modules

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 LG Innotek Co., Ltd.

- 6.4.5 Cree LED, a Smart Global Holdings Company

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Osram GmbH

- 6.4.8 Bridgelux, Inc.

- 6.4.9 Everlight Electronics Co., Ltd.

- 6.4.10 Lite-On Technology Corporation

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Sharp Corporation

- 6.4.13 Citizen Electronics Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 Toyoda Gosei Co., Ltd.

- 6.4.16 Nationstar Optoelectronics Co., Ltd.

- 6.4.17 Hongli Zhihui Group Co., Ltd.

- 6.4.18 Dominant Opto Technologies Sdn. Bhd.

- 6.4.19 MLS Co., Ltd.

- 6.4.20 Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment