PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065525

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065525

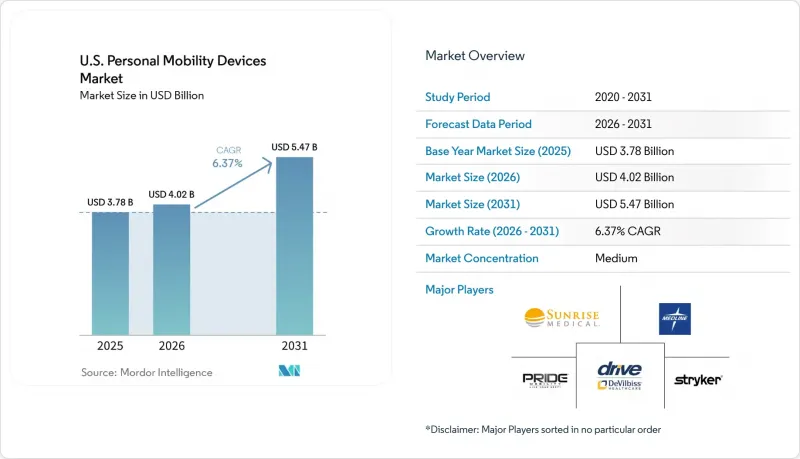

U.S. Personal Mobility Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. personal mobility devices market size is projected to expand from USD 3.78 billion in 2025 and USD 4.02 billion in 2026 to USD 5.47 billion by 2031, registering a CAGR of 6.37% between 2026 to 2031.

This report is Segmented by Product Type (Wheelchairs, Mobility Scooters, Walking Aids, Power-Assist Add-Ons), Technology (Manual, Powered, Power-Assist and Hybrid, Smart and Connected), End User (Personal Users, Hospitals, Rehab Centers, Long-Term Care, Home Healthcare and DME Rental), and Distribution Channel (Offline, E-Commerce). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Personal Mobility Devices Market Trends and Insights

Aging U.S. Population and Rising Mobility-Loss Years Lived

Motor function impairments among older Americans show a steep age-related pattern. Chair-stand impairments are significant in the 65 to 69 age group, while gait-speed issues dominate among those aged 90 and above. The next wave of retirees carries heavier disability burdens from middle age, leading to earlier adoption of mobility aids. Rising musculoskeletal disorders and fall-related mortalities among adults aged 65 and older indicate increasing reliance on powered support. This trend sustains replacement demand and ties the United States personal mobility devices market to demographic shifts rather than short-term care cycles.

High Disability and Arthritis Burden Expanding Addressable Users

Stroke and osteoarthritis are key drivers of wheelchair and scooter use in the United States, broadening the user base across age groups and care settings. A 2024 study of 64.1 million adults with arthritis found that age over 70, severe pain, and comorbidities significantly limit physical functioning, creating a large pool of intermittent and permanent device users. The disability share of the United States population rose to 14.14% in 2024, marking a second consecutive year of increase. This growing user base favors lightweight, foldable, and mid-range devices, positioning suppliers with diverse inventories to capture market growth.

High Out-of-Pocket Burden for Advanced Powered Devices

Advanced complex rehabilitative power wheelchairs often exceed USD 30,000, with Medicare covering only a portion of the cost and secondary insurance varying widely. A 2025 disability-rights survey revealed that Medicare users faced partial reimbursements, delays, and significant out-of-pocket expenses, leading to increased pain, reduced activity, and social isolation. In 2024, the poverty rate for working-age adults with disabilities was 24.8%, compared to 11.1% for non-disabled adults, highlighting financial barriers to accessing premium devices.

Other drivers and restraints analyzed in the detailed report include:

- Medicare Coverage Breadth and Seat-Elevation Reimbursement Update

- Shift to Lighter, Foldable, Connected Power Mobility Platforms

- Safety Recalls & Rising Litigation on Lithium-ion Fire Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, wheelchairs accounted for 45.21% of the United States personal mobility devices market, driven by established reimbursement pathways and urgent clinical needs. Manual and complex rehabilitative power wheelchairs remain key, while power wheelchairs are gaining traction due to expanded coverage and improved designs. Mobility scooters, with a projected CAGR of 6.66% from 2026 to 2031, cater to ambulatory users needing enhanced community and outdoor mobility. Walking aids, including canes, crutches, walkers, and rollators, maintain steady demand due to affordability and ease of purchase. The category mix is evolving as buyers increasingly opt for power-assist and positioning add-ons instead of transitioning directly to powered chairs. Sunrise Medical's Empulse M90 enables cost-effective upgrades to manual chairs with motorized propulsion.

Manual devices accounted for 50.45% of the technology split in 2025, reflecting the widespread use of manual wheelchairs, walkers, and rollators. Powered devices, projected to grow at a 7.12% CAGR from 2026 to 2031, are gaining popularity due to reduced self-propulsion ability, better reimbursement support, and higher comfort expectations. Power-assist and hybrid systems bridge the gap, offering motorized support without requiring a full transition to premium powered frames.

Advanced features are increasingly moving from specialized rehabilitation products to standard configurations. Sunrise Medical introduced Dynamic Controls LiNX controls in the QUICKIE Q300 M Mini, narrowing the gap between premium and mid-market products.

List of Companies Covered in this Report:

- Amigo Mobility International, Inc.

- Briggs Healthcare

- Carex

- Drive DeVilbiss Healthcare

- GF Health Products, Inc.

- Golden Technologies

- Hoveround Corporation

- Karman Healthcare

- Kaye Products, Inc.

- Medline Industries

- Merits Health Products, Inc.

- NOVA Medical Products

- Ottobock

- Performance Health

- Permobil

- Pride Mobility Products Corporation

- Rollz International B.V.

- Stryker

- Sunrise Medical

- WHILL, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging U.S. Population and Rising Mobility-Loss Years Lived

- 4.2.2 High Disability and Arthritis Burden Expanding Addressable Users

- 4.2.3 Medicare Coverage Breadth and Seat-Elevation Reimbursement Upgrades

- 4.2.4 Shift to Lighter, Foldable, Connected Power Mobility Platforms

- 4.2.5 Airline Liability Reforms Improving Travel Confidence for Device Users

- 4.2.6 Rapid E-Commerce Penetration in DME (Durable Medical Equipment) Retail

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Burden for Advanced Powered Devices

- 4.3.2 Medicare Home-Use Test and Documentation Friction Limiting Approvals

- 4.3.3 Repair Downtime, Battery/Caster Failures, and Weak Service Density

- 4.3.4 Safety Recalls & Rising Litigation on Lithium-Ion Fire Risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory & Reimbursement Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Wheelchairs

- 5.1.1.1 Manual Wheelchairs

- 5.1.1.2 Powered Wheelchairs

- 5.1.1.3 Robotic/Autonomous Wheelchairs

- 5.1.2 Mobility Scooters

- 5.1.2.1 3-Wheel Scooters

- 5.1.2.2 4-Wheel Scooters

- 5.1.2.3 Foldable and Portable Scooters

- 5.1.3 Walking Aids

- 5.1.3.1 Canes & Crutches

- 5.1.3.2 Walkers & Rollators

- 5.1.4 Power-Assist and Positioning Add-ons

- 5.1.5 Transfer and Accessibility Mobility Devices

- 5.1.1 Wheelchairs

- 5.2 By Technology

- 5.2.1 Manual Devices

- 5.2.2 Powered Devices

- 5.2.3 Power-Assist and Hybrid Devices

- 5.2.4 Smart and Connected Devices

- 5.3 By End User

- 5.3.1 Personal Users and Households

- 5.3.2 Hospitals and Clinics

- 5.3.3 Rehabilitation Centers

- 5.3.4 Long-Term Care and Assisted Living Facilities

- 5.3.5 Home Healthcare and DME Rental Providers

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 E-Commerce

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amigo Mobility International, Inc.

- 6.3.2 Briggs Healthcare

- 6.3.3 Carex Health Brands

- 6.3.4 Drive DeVilbiss Healthcare

- 6.3.5 GF Health Products, Inc.

- 6.3.6 Golden Technologies

- 6.3.7 Hoveround Corporation

- 6.3.8 Karman Healthcare

- 6.3.9 Kaye Products, Inc.

- 6.3.10 Medline Industries, LP

- 6.3.11 Merits Health Products, Inc.

- 6.3.12 NOVA Medical Products

- 6.3.13 Ottobock SE & Co. KGaA

- 6.3.14 Performance Health

- 6.3.15 Permobil

- 6.3.16 Pride Mobility Products Corporation

- 6.3.17 Rollz International B.V.

- 6.3.18 Stryker Corporation

- 6.3.19 Sunrise Medical LLC

- 6.3.20 WHILL, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment