PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065537

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065537

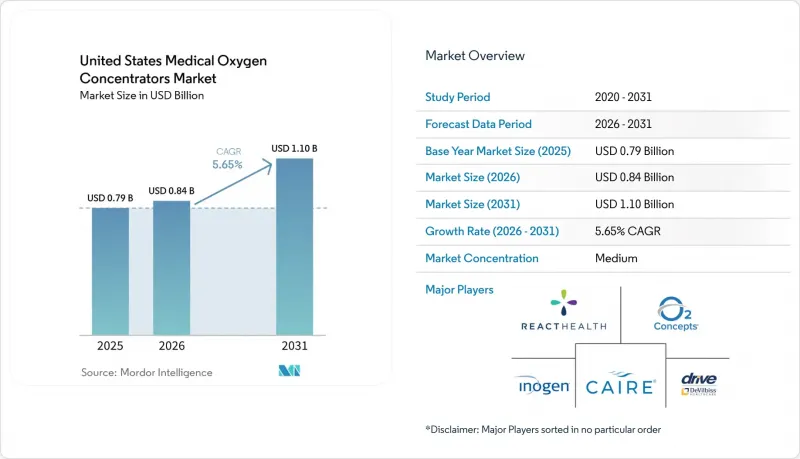

United States Medical Oxygen Concentrators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states medical oxygen concentrators market size was valued at USD 0.79 billion in 2025 and is estimated to grow from USD 0.84 billion in 2026 to reach USD 1.10 billion by 2031, at a CAGR of 5.65% during the forecast period (2026-2031).

This report is Segmented by Product Type (Portable, Stationary), Technology (Continuous Flow, Pulse Flow), Care Setting (Home Care, Hospitals and Health Systems, Long-Term Care and SNFs, Ambulatory Transport), Indication (COPD, Asthma, Sleep Apnea and Sleep-Related Hypoxemia, Others). The Market Forecasts are Provided in Terms of Value (USD).

United States Medical Oxygen Concentrators Market Trends and Insights

COPD Burden and Aging LTOT Population

The market has a stable volume base in COPD, but the stronger growth driver is disease severity in older adults rather than new incidence. COPD was the fifth leading cause of death in the United States in 2023, with 141,733 deaths, and it generated annual medical costs of USD 24 billion among adults aged 45 and older. The age pattern is sharp, with prevalence rising from 0.4% in adults aged 18 to 24 to 10.5% in adults aged 75 and older, which helps explain why older Medicare patients account for a large share of continuous-flow prescriptions and long-duration use. As the Baby Boom population moves further into the 75+ bracket, the United States medical oxygen concentrators market will continue to see demand clustered in patients who need higher-capacity stationary systems for overnight and sustained daytime support. This concentration in older patients also increases dependence on Medicare reimbursement rules, because providers tend to narrow product choice when payment rates do not keep pace with device, service, and delivery costs. The result is a market where volume is dependable, but product mix can still be constrained by the economics of serving a large aging LTOT population.

Shift Toward Home-Based Oxygen Therapy

The United States medical oxygen concentrators market continues to benefit from the move toward home-based oxygen therapy, which is now tied as much to discharge planning as to patient preference. CMS National Coverage Determination 240.2 remains the key federal coverage framework for home oxygen, and the CY 2026 Home Health final rule also finalized supplier-related changes that affect how home oxygen is provided and managed. CAIRE's January 2025 launch of IntenOxy 5 was positioned directly around this setting shift, with a power draw below 350 W and a weight of 34.2 lbs, both of which support lower service and deployment costs in the home. Geographic demand reinforces the same direction, because COPD prevalence in the Midwest and South was 4.2% in each region in 2023, above the national 3.8% rate, and many of these patients live in areas where hospital access is more limited. Rural smoking patterns and slower smoking cessation in those areas further support a wide patient pool that is better served by home-ready oxygen systems than by repeated facility-based care. This keeps the United States medical oxygen concentrators market centered on residential delivery models and on products built for lower servicing cost per patient.

High Upfront Device and Battery Ownership Cost

Ownership cost remains a real barrier in the United States medical oxygen concentrators market for patients who buy devices directly rather than rent them. Premium portable oxygen concentrators retail at USD 2,000 to USD 4,500, and extended battery packs add USD 200 to USD 600 per unit, which places a full portable setup beyond reach for many lower-income patients. The cost burden is more important because COPD prevalence reaches 8.2% among adults near the federal poverty level, which means financial strain and clinical need often overlap in the same patient group. The rental model softens some of that burden, but it does not eliminate it for long-term users. Inogen reported that capped patients accounted for 17.6% of its total patients on service in 2025, which shows the size of the cohort that can move into a post-cap period without a strong structural coverage pathway for ongoing device-related costs. Unless broader maintenance or supplemental coverage options become more common, this cost barrier will continue to limit direct ownership demand even as portable products improve.

Other drivers and restraints analyzed in the detailed report include:

- Portable Concentrator Adoption and Mobility Demand

- Reimbursement and Access Reform Momentum

- Reimbursement Bias Toward Basic Stationary Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Portable medical oxygen concentrators commanded 54.31% of the United States medical oxygen concentrators market share in 2025, and they are also the fastest-growing product type with a CAGR of 7.38% through 2031. That mix of current leadership and future growth is unusual and shows how decisively the United States medical oxygen concentrators market has moved toward ambulatory care. Demand is being supported by an aging but still active patient base, by FAA-compatible travel use, and by a broader patient preference for systems that fit daily movement rather than fixed-room use. Newer pulse-dose architectures have also improved the clinical standing of portable devices, which has narrowed the credibility gap that once favored stationary units in a much larger share of cases. CAIRE's autoSAT platform, supported by a 2025 Georgia State University study published in Pulmonary Therapy, showed stable FiO2 performance during higher breathing rates, which strengthens the case for portable use in more active patients.

Stationary medical oxygen concentrators still keep a meaningful installed base in home care, long-term care, and skilled nursing facilities because many patients need higher continuous-flow support, especially during overnight therapy. In the United States medical oxygen concentrators industry, that base remains important because high-flow home use, structured facility management, and limited patient mobility still favor stationary platforms. Inogen's 2025 move into stationary devices through the Yuwell-developed Voxi 5, backed by a USD 27.2 million equity investment, showed that even the leading portable specialist sees room for stationary therapy in the United States medical oxygen concentrators market. Philips' withdrawal from oxygen products has added to the stationary replacement cycle, because providers with legacy fleets need alternatives that can be deployed quickly. Drive Medical's 555 Compact, positioned as the first U.S.-assembled unit in the relaunched DeVilbiss by Drive line, was engineered for shipping efficiency with 36 units per pallet compared with 27 for the prior model, which matters in a category where freight and service costs are tightly managed.

Continuous flow technology retained 61.24% of the United States medical oxygen concentrators market share in 2025, while pulse flow is projected to grow faster at a CAGR of 6.22% through 2031. Continuous flow remains the clinical standard for moderate-to-severe COPD and for overnight use because it delivers uninterrupted oxygen without depending on breath detection. That matters during sleep, when irregular breathing patterns and lower respiratory rates can make pulse-based delivery less reliable in some patients. The strength of continuous flow also reflects how much of the United States medical oxygen concentrators market still serves patients with higher acuity and more sustained oxygen need. At the same time, pulse flow continues to gain ground as ambulatory home use expands and as smaller devices deliver better battery life and lower carrying weight.

The more important technology shift is not flow mode alone, but the intelligence added to pulse delivery and to remote fleet oversight. CAIRE's UltraSense and autoDOSE functions in the FreeStyle Comfort deliver oxygen even when no breath is detected, which directly addresses a core clinical concern around frail or shallow-breathing patients. GCE Healthcare's Clarity Connected Care platform adds remote visibility into oxygen purity, battery status, and usage history for Zen-O and Zen-O Lite devices, which turns the device category into a more service-driven proposition for DME providers. This makes technology competition in the United States medical oxygen concentrators market less about headline flow rate alone and more about how consistently delivery, adherence, and fleet monitoring can be managed over time. As a result, the growth of pulse flow is tied not only to mobility demand, but also to smarter delivery systems that reduce the clinical tradeoff once associated with portable use.

List of Companies Covered in this Report:

- 3B Medical

- AirSep (Chart Industries)

- ARYA BioMed Corp.

- Belluscura Health

- Caire

- Compass Health

- Drive DeVilbiss Healthcare

- GCE Healthcare

- Inogen

- MedaCure Inc.

- Nidek Medical Products, Inc.

- O2 Concepts, LLC

- Philips Respironics

- Precision Medical

- React Health

- Rhythm Healthcare

- Roscoe Medical

- Sunset Healthcare Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 COPD Burden and Aging LTOT Population

- 4.2.2 Shift Toward Home-Based Oxygen Therapy

- 4.2.3 Portable Concentrator Adoption and Mobility Demand

- 4.2.4 Reimbursement and Access Reform Momentum

- 4.2.5 Philips Exit-Driven Replacement Cycle

- 4.2.6 Connected DME Fleet Management and Telehealth Integration

- 4.3 Market Restraints

- 4.3.1 High Upfront Device and Battery Ownership Cost

- 4.3.2 Reimbursement Bias Toward Basic Stationary Units

- 4.3.3 Post-Recall Regulatory Scrutiny and Supplier Qualification Delays

- 4.3.4 Portable Clinical Limits for High-Flow and Nocturnal Patients

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Portable Medical Oxygen Concentrators

- 5.1.2 Stationary Medical Oxygen Concentrators

- 5.2 By Technology

- 5.2.1 Continuous Flow

- 5.2.2 Pulse Flow

- 5.3 By Care Setting

- 5.3.1 Home Care

- 5.3.2 Hospitals and Health Systems

- 5.3.3 Long-Term Care and Skilled Nursing Facilities

- 5.3.4 Ambulatory Transport and Transitional Care

- 5.4 By Indication

- 5.4.1 Chronic Obstructive Pulmonary Disease

- 5.4.2 Asthma

- 5.4.3 Sleep Apnea and Sleep-Related Hypoxemia

- 5.4.4 Other Indications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 3B Medical

- 6.3.2 AirSep (Chart Industries)

- 6.3.3 ARYA BioMed Corp.

- 6.3.4 Belluscura Health

- 6.3.5 CAIRE Inc.

- 6.3.6 Compass Health Brands

- 6.3.7 Drive DeVilbiss Healthcare

- 6.3.8 GCE Healthcare

- 6.3.9 Inogen, Inc.

- 6.3.10 MedaCure Inc.

- 6.3.11 Nidek Medical Products, Inc.

- 6.3.12 O2 Concepts, LLC

- 6.3.13 Philips Respironics

- 6.3.14 Precision Medical, Inc.

- 6.3.15 React Health

- 6.3.16 Rhythm Healthcare

- 6.3.17 Roscoe Medical

- 6.3.18 Sunset Healthcare Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment