PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065547

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065547

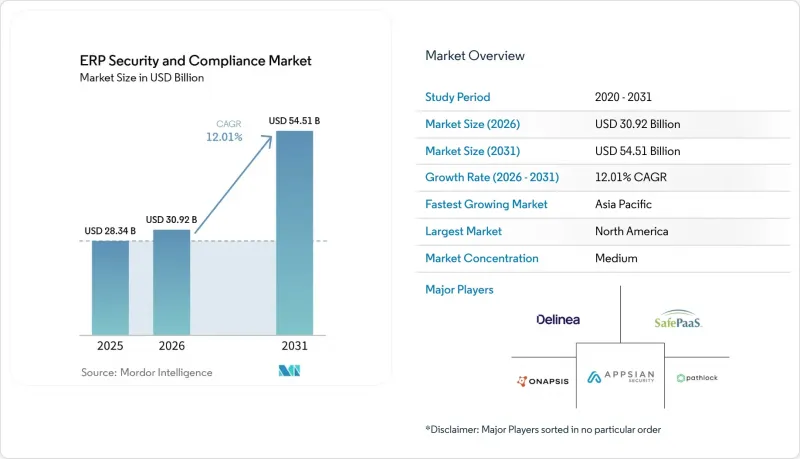

ERP Security And Compliance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the eRP security and compliance market size is projected to expand from USD 28.34 billion in 2025 and USD 30.92 billion in 2026 to USD 54.51 billion by 2031, registering a CAGR of 12.01% between 2026 and 2031.

This report is Segmented by Component (Software and Services), Deployment Mode (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises and SMEs), End-Use Industry (Manufacturing, Banking, Financial Services and Insurance, Healthcare, Retail and E-Commerce, Government and Public Sector, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global ERP Security And Compliance Market Trends and Insights

Proliferation of Cloud-Based ERP Deployments

Three out of four enterprises ran at least one cloud ERP instance in 2025, but the shared-responsibility model blurs accountability between vendor and customer for access governance. Multi-tenant architectures expose application programming interfaces that adversaries weaponize, while voice-phishing accounted for 23% of cloud compromises in 2025. The U.S. Securities and Exchange Commission now compels public companies to disclose material cyber incidents within four business days, forcing boards to scrutinize ERP role design and SoD hygiene. Continuous monitoring that ingests user-behavior telemetry and flags privilege escalations in real time is emerging as a board-level requirement. Vendors that automate the mapping of roles to business-process risk scenarios gain purchase precedence because they cut audit preparation from weeks to hours.

Escalating Regulatory Compliance Requirements Across Industries

PCI DSS v4.0 became compulsory in March 2025, adding 64 new requirements that strengthen authentication and require quarterly penetration testing in ERP-linked cardholder environments. Europe's Corporate Sustainability Reporting Directive extends oversight to non-financial data, obliging finance teams to reconcile ESG metrics with general ledger entries. Banks' face Basel III operational resilience proofs that map critical business services to ERP modules, creating steady demand for automated evidence generation. Auditors in North America are increasingly rejecting manual SoD attestations and moving toward continuous digital substantiation. Together, the multifaceted mandates ensure sustained purchasing momentum for the ERP security and compliance market as firms seek to unify controls across financial and sustainability disclosures.

Integration of AI-Driven Behavioral Analytics

AI-based anomaly engines now parse millions of ERP transactions per hour, correlating unusual posting times, location anomalies, and peer-group deviations to generate real-time risk scores. Early adopters in North America and Europe cite a 60% reduction in false-positive alerts relative to rule-centric systems, freeing analysts to investigate high-fidelity threats. Onapsis's Agentic Gateway showcases large-language-model summarization that turns forensic signals into plain-English incident narratives, enabling finance and audit staff to validate alerts without cybersecurity jargon. AI explainability is also moving up the regulatory agenda, with European watchdogs exploring guidance that requires clear audit trails for machine-generated access decisions, further boosting investment in transparent behavioral engines.

Other drivers and restraints analyzed in the detailed report include:

- Rising Incidence of Insider Threats and Data Breaches

- Growing Need for Centralized SoD Management

- Demand for Continuous Controls Monitoring Linked to ESG Assurance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software dominated the ERP security and compliance market in 2025, yet the narrative is shifting. Enterprises have already purchased core SoD engines and continuous controls dashboards; now they crave the expertise to operationalize them. Services revenue, consulting, implementation, and managed detection, grows at 16.80% CAGR, reflecting this pivot. Advisory engagements increasingly incorporate business-process reengineering to ensure SoD enforcement aligns with ISO 27001:2022 risk-based principles, while managed-service subscriptions bundle 24/7 alert triage and quarterly access attestations.

Software vendors, meanwhile, race to lower the total cost of ownership through low-code API orchestration. Pathlock's August 2025 link-up with Microsoft Sentinel demonstrates how ERP-centric anomalies can feed directly into existing security operations workflows, eliminating the need for separate SIEM dashboards. Over the forecast horizon, platform vendors will embed AI-assisted configuration that guides customers through context-aware role definitions, further closing the skills gap and sustaining software renewal momentum inside the ERP security and compliance market.

Cloud deployments accounted for 58.50% of 2025 revenue and continue to outpace alternatives as financial-management, supply-chain, and human-capital-management suites migrate to Oracle Fusion Cloud, SAP S/4HANA Cloud, and Microsoft Dynamics 365. The ERP security and compliance market size tied to cloud instances is forecast to increase at an 18.30% CAGR through 2031 as SaaS ERP becomes the default choice for greenfield installations. FedRAMP's 325-control moderate baseline serves as a benchmark well beyond U.S. federal agencies, prompting private enterprises to insist on equivalent coverage. Continuous API log ingestion, serverless agents, and in-memory analytics deliver minute-level anomaly detection, collapsing mean-time-to-detect from days to minutes.

On-premises estates persist in the defense and critical infrastructure sectors, where data sovereignty rules and air-gapped networks require local hosting. Maintenance costs escalate as vendors funnel research and development toward cloud-native feature sets. Hybrid deployments, which splice on-premise financial modules with cloud-based talent systems, introduce cross-identity complexities that force security teams to manage entitlements across at least two directories. Unified dashboards that consolidate risk postures across modes are now table stakes in request-for-proposal scoring.

Geography Analysis

North America remains the largest regional slice at 34.10% in 2025, anchored by Sarbanes-Oxley audits, deep cybersecurity vendor benches, and aggressive cloud ERP adoption among Fortune 500 companies. Artificial-intelligence anomaly engines gain traction first in this region, producing lighthouse implementations that global subsidiaries later replicate. Mergers and acquisitions among mid-cap players spark new ERP instances and consolidation efforts, both of which require fresh SoD review.

Asia-Pacific posts the fastest 17.20% CAGR, driven by Japan's spike in credential-stuffing incidents, India's data-protection statute, and Singapore's amended Personal Data Protection Act that levies fines of SGD 1 million (USD 750,000) for delayed breach notifications. Chinese data-localization rules compel multinationals to deploy in-country ERP stacks, in which local CSPs partner with international security vendors to satisfy dual compliance requirements. Skill shortages are acute, so managed service providers fill gaps, accelerating SaaS security adoption.

Europe grows steadily as GDPR fines escalate, crossing EUR 2.1 billion (USD 2.3 billion) in 2025. The NIS2 directive widens the definition of critical infrastructure to include digital service providers, adding transportation and logistics to the compliance roster. South America's trajectory reflects the influence of Brazil's Lei Geral de Protecao de Dados and Argentina's consent-centric data-protection law. The Middle East and Africa trail in spend but experience double-digit growth as sovereign-cloud initiatives and National Institute of Standards and Technology model-led frameworks require ERP-layer controls merged with national cyber-defense strategies.

- Pathlock Inc.

- Appsian Security Inc.

- SafePaaS Inc.

- Onapsis Inc.

- Delinea Inc.

- Fastpath Solutions LLC

- Soterion Ltd.

- MTC Skopos AG

- Access Informer Pty Ltd

- Dynaflow Compliance Solutions Inc.

- ERP Armor LLC

- Saviynt Inc.

- Security Weaver LLC

- CSI Tools NV

- SmartERP Solutions Inc.

- ERP Maestro Inc.

- SailPoint Technologies Holdings Inc.

- Netwrix Corporation

- Kainos Group plc

- IBS Schreiber GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Cloud-based ERP Deployments

- 4.2.2 Escalating Regulatory Compliance Requirements Across Industries

- 4.2.3 Rising Incidence of Insider Threats and Data Breaches in ERP Environments

- 4.2.4 Growing Need for Centralized SoD Management in Multi-ERP Landscapes

- 4.2.5 Integration of AI-Driven Behavioral Analytics for Real-Time Risk Scoring

- 4.2.6 Demand for Continuous Controls Monitoring Tied to ESG Assurance

- 4.3 Market Restraints

- 4.3.1 High Initial Integration and Implementation Costs

- 4.3.2 Shortage of Skilled ERP Security Professionals

- 4.3.3 Overlapping IGA and PAM Toolsets Creating Purchase Decision Paralysis

- 4.3.4 Vendor Consolidation Limiting Best-of-Breed Options for Niche Compliance Needs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-use Industry

- 5.4.1 Manufacturing

- 5.4.2 Banking, Financial Services and Insurance

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Government and Public Sector

- 5.4.6 IT and Telecom

- 5.4.7 Other End-use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia-Pacific

- 5.5.5 Middle East

- 5.5.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pathlock Inc.

- 6.4.2 Appsian Security Inc.

- 6.4.3 SafePaaS Inc.

- 6.4.4 Onapsis Inc.

- 6.4.5 Delinea Inc.

- 6.4.6 Fastpath Solutions LLC

- 6.4.7 Soterion Ltd.

- 6.4.8 MTC Skopos AG

- 6.4.9 Access Informer Pty Ltd

- 6.4.10 Dynaflow Compliance Solutions Inc.

- 6.4.11 ERP Armor LLC

- 6.4.12 Saviynt Inc.

- 6.4.13 Security Weaver LLC

- 6.4.14 CSI Tools NV

- 6.4.15 SmartERP Solutions Inc.

- 6.4.16 ERP Maestro Inc.

- 6.4.17 SailPoint Technologies Holdings Inc.

- 6.4.18 Netwrix Corporation

- 6.4.19 Kainos Group plc

- 6.4.20 IBS Schreiber GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment