PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065561

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065561

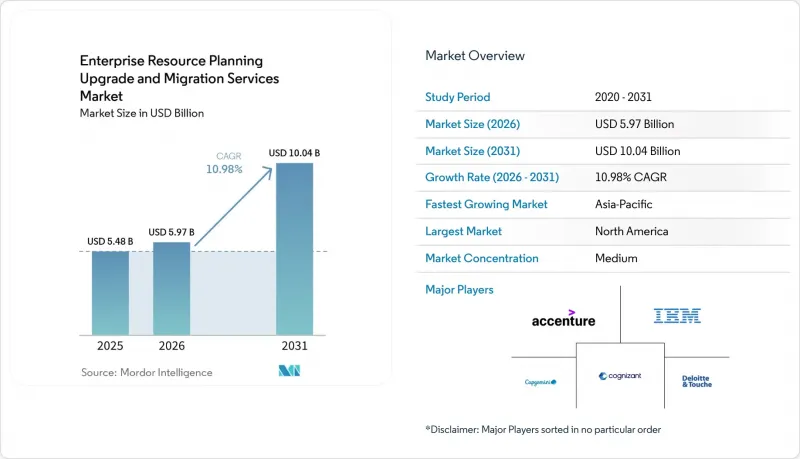

Enterprise Resource Planning Upgrade And Migration Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the eRP upgrade and migration services market size is projected to be USD 5.48 billion in 2025, USD 5.97 billion in 2026, and reach USD 10.04 billion by 2031, growing at a CAGR of 10.98% from 2026 to 2031.

This report is Segmented by Deployment Model (On-Premises, Cloud-Based, and Hybrid), Organization Size (Small and Medium Enterprises and Large Enterprises), Industry Vertical (Manufacturing, Banking, Financial Services and Insurance (BFSI), Healthcare, IT and Telecom, Government and Public Sector, and More), and Geography. Market Forecasts are in Value (USD).

Global Enterprise Resource Planning Upgrade And Migration Services Market Trends and Insights

Rising Demand for Post-Pandemic Digital Resilience

Organizations that endured supply-chain shocks and prolonged remote work between 2020 and 2023 concluded that on-premises ERP lacked the elasticity required for rapid reconfiguration. The imperative for resilience is accelerating cloud uptake, with 70.4% of deployments already cloud-based by 2024. Manufacturing firms are embedding IoT sensors in S/4HANA to predict maintenance needs, while retailers use real-time stock analytics to cut stockouts by 20-30%. Financial institutions are shifting liquidity dashboards to cloud-native cores that integrate seamlessly with payment gateways. North America and Europe lead adoption, yet Asia-Pacific is closing the gap as government incentive programs offset infrastructure costs.

Accelerated Shift to Cloud-First ERP Architectures

Cloud ERP's five-year total cost of ownership is 30-40% lower than comparable on-premises estates when hardware refreshes, database licenses, and internal labor are factored in. SME enthusiasm is high, 70% prefer cloud solutions, and platforms such as Odoo added 13,000 clients per month in 2025. Hybrid designs persist in risk-averse sectors but mainly serve as transition architectures. Asia-Pacific momentum is underpinned by a USD 8 billion Oracle data-center buildout in Japan that guarantees sub-10-millisecond latency for domestic users. Data-sovereignty statutes like GDPR and PDPL make in-country cloud zones a prerequisite for regulated workloads, reinforcing the long-term shift.

High Upfront Capital Expenditure for Large-Scale Upgrades

Project budgets remain front-loaded: midsized migrations cost USD 150,000-USD 750,000 and enterprise programs can exceed USD 50 million. Hidden overruns in data quality and custom code can inflate totals by 30%. SMEs mitigate shock with phased rollouts or modular cloud suites starting below USD 50,000. Currency volatility and limited financing options in Africa and South America further constrain uptake. Compliance add-ons-GDPR hosting, HIPAA controls-consume an extra 10-15% of budgets.

Other drivers and restraints analyzed in the detailed report include:

- Vendor-Induced End-of-Support Deadlines

- Increasing Adoption of Industry-Specific ERP Templates

- Shortage of Certified ERP Migration Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments captured 51% of the ERP upgrade and migration services market share in 2025, and this segment is advancing at a 18.4% CAGR through 2031, making it the structural growth engine of the ERP upgrade and migration services market. Subscription pricing removes data-center capital outlays, and quarterly vendor releases replace costly version-upgrade projects, shifting spend toward value-added extensions. SMEs embrace pure-cloud suites that go live within six months, while large enterprises often start with infrastructure-as-a-service "lift and shift" moves before refactoring to cloud-native designs.

Hybrid models bridge risk-averse organizations to the cloud, keeping finance cores on-premises while offloading analytics or HCM modules. This dual-state architecture complicates data synchronization and raises support costs by 10-15%, but remains preferable to disruptive rip-and-replace tactics. On-premises estates now represent legacy holdouts in sectors such as defense and critical infrastructure, where latency or sovereignty overrides economics. The ERP upgrade and migration services market continues to reward vendors that provide zero-downtime migration tooling and automated regression testing that protect production uptime during cutovers.

Geography Analysis

North America retained 34.5% of 2025 revenue thanks to the world's densest population of legacy SAP and Oracle estates and a mature consulting ecosystem. Growth is propelled by the approaching 2027 SAP ECC deadline, reshoring initiatives in manufacturing, and healthcare consolidation. Canada and Mexico add incremental demand tied to USMCA supply chains, particularly in automotive and agribusiness.

Asia-Pacific is the fastest-growing region at 13.9% CAGR through 2031, driven by Digital India, Made in China 2025, and Japan's Digital Garden City Nation funding that subsidizes municipal cloud ERP upgrades. Oracle's USD 8 billion infrastructure pledge in Japan and SAP partnerships with NTT Data and Fujitsu ensure local data residency, a prerequisite under Japan's privacy statutes. Although state-owned Chinese firms often select domestic vendors for sovereignty reasons, multinationals rely on SAP and Oracle for harmonized global processes.

Europe's trajectory is shaped by GDPR, MiFID II, and medical-device regulations that favor compliance-ready templates. Germany leads spend among Mittelstand manufacturers, followed by the United Kingdom and France. The Middle East, led by Saudi Arabia and the United Arab Emirates, channels oil-diversification funds into large-scale ERP modernization; PDPL data-localization rules stimulate local cloud zones. Africa and South America, though smaller, are leapfrogging on-premises stages by adopting mobile-first cloud ERP in fintech and agriculture, aided by improving broadband coverage and competitive hyperscale pricing.

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- International Business Machines Corporation

- Cognizant Technology Solutions Corporation

- Wipro Limited

- HCL Technologies Limited

- Atos SE

- DXC Technology Company

- Tech Mahindra Limited

- NTT DATA Corporation

- CGI Inc.

- Larsen and Toubro Infotech Ltd (LTI Mindtree)

- EPAM Systems Inc.

- Rackspace Technology Inc.

- Hitachi Consulting Co., Ltd.

- Syntax Systems Ltd.

- Vision33 Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Industry-Specific ERP Modules

- 4.2.2 Acceleration of Cloud-First Digital Transformation Strategies

- 4.2.3 Growing SME Adoption of Subscription-Based ERP Suites

- 4.2.4 Demand for Post-Implementation Hyper-Care Services (Under-the-Radar)

- 4.2.5 Shift Toward Composable ERP Architecture (Under-the-Radar)

- 4.2.6 Increasing Use of Low-Code Platforms for Tailored Workflows (Under-the-Radar)

- 4.3 Market Restraints

- 4.3.1 High Switching Costs Limiting Vendor Migration

- 4.3.2 Shortage of Certified ERP Functional Consultants

- 4.3.3 Rising Concerns Around Data Residency Compliance (Under-the-Radar)

- 4.3.4 Technical Debt From Legacy Customizations (Under-the-Radar)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By End-Use Industry

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-Commerce

- 5.3.3 Banking, Financial Services and Insurance (BFSI)

- 5.3.4 Healthcare

- 5.3.5 Information Technology and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-Use Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Kenya

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 Capgemini SE

- 6.4.4 Tata Consultancy Services Limited

- 6.4.5 Infosys Limited

- 6.4.6 International Business Machines Corporation

- 6.4.7 Cognizant Technology Solutions Corporation

- 6.4.8 Wipro Limited

- 6.4.9 HCL Technologies Limited

- 6.4.10 Atos SE

- 6.4.11 DXC Technology Company

- 6.4.12 Tech Mahindra Limited

- 6.4.13 NTT DATA Corporation

- 6.4.14 CGI Inc.

- 6.4.15 Larsen and Toubro Infotech Ltd (LTI Mindtree)

- 6.4.16 EPAM Systems Inc.

- 6.4.17 Rackspace Technology Inc.

- 6.4.18 Hitachi Consulting Co., Ltd.

- 6.4.19 Syntax Systems Ltd.

- 6.4.20 Vision33 Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment