PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065574

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065574

ERP Implementation Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

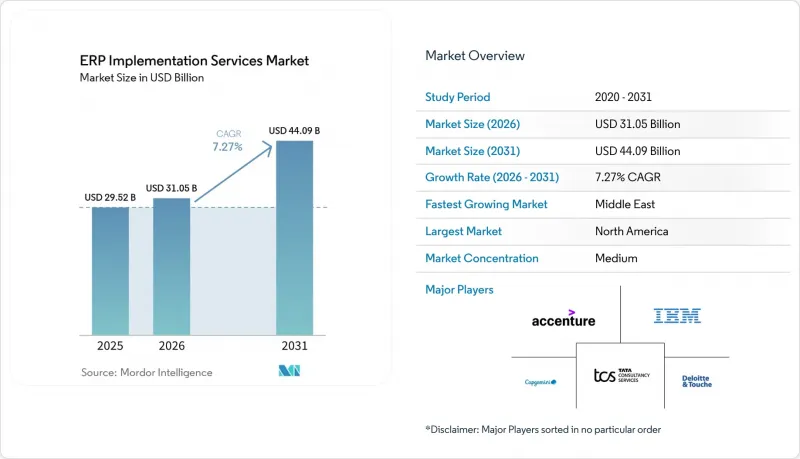

According to Mordor Intelligence, the eRP implementation services market size expanded from USD 29.52 billion in 2025 to USD 31.05 billion in 2026 and is projected to reach USD 44.09 billion by 2031, registering a 7.27% CAGR over 2026-2031.

This report is Segmented by Deployment Model (On-Premises, Cloud, and Hybrid), Organization Size (Small and Medium Enterprises and Large Enterprises), End-Use Industry (Manufacturing, Retail and E-Commerce, Banking, Financial Services, and Insurance, Healthcare, Government and Public Sector, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global ERP Implementation Services Market Trends and Insights

Cloud-First Digital Transformation Mandates

Governments have tied modernization budgets to certified cloud adoption, compressing purchasing cycles and steering public-sector spending toward hyperscaler-hosted ERP. The United States Office of Management and Budget's 2024 cloud directive and the European Union's Digital Decade program are propelling migrations, while Saudi Arabia's 2025 National Cloud Computing Framework bans new on-premises ERP purchases. Integrators are grappling with a skills gap because 40% of consultants still lack multi-tenant SaaS expertise.

Surge in Real-Time Data-Driven Decision Making

Manufacturers now embed ERP systems within operational technology networks to re-plan production the moment supply-chain anomalies surface. Siemens integrated SAP S/4HANA with its MindSphere IoT suite across 15 factories in 2025, reducing inventory holding costs by 18%. Automotive OEMs and large retailers are echoing the model, linking demand forecasts to supplier lines and point-of-sale feeds, respectively, thereby reducing monthly close cycles from 10 days to 3 days.

High Total Cost of Ownership for Brownfield Integrations

Surveys show that 68% of SAP ECC customers have more than 500 custom objects, ballooning refactoring budgets by 40-60% during migration to S/4HANA. Similar challenges plague Oracle E-Business Suite customers whose bespoke forms lack direct upgrade paths to Oracle Cloud ERP. Integration of dozens of bolt-on applications often consumes 30-40% of project spend, prompting 34% of mid-market manufacturers to extend on-premises support contracts instead of moving to the cloud.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Subscription-Based ERP Uptake Among SMEs

- Compliance-Induced ERP Modernization in Regulated Sectors

- Shortage of Skilled ERP Functional Consultants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments captured 17.8% CAGR during 2026-2031, the fastest pace among models, as banks, healthcare chains, and defense contractors hold master data behind the firewall while routing analytics to public cloud. Cloud configurations still accounted for 58% of 2025 revenue, primarily from digital-native firms and SMEs that treat infrastructure as a utility, whereas on-premises estates contracted but persisted in air-gapped defense networks. Sovereign cloud variants introduced by SAP and Oracle in 2025 keep data within national borders and command 25-35% price premiums, illustrating how sovereignty adds complexity but also value. Integrators monetize the intricacy by selling governance frameworks that trim post-go-live incidents 40%, thereby reinforcing recurring revenue streams tied to managed services.

Enterprises that lean on hybrid models increasingly blend event-streaming platforms with ERP cores, enabling manufacturing plants to process telemetry locally while still pushing aggregated insights to cloud lakes for advanced analytics. The dual-stack approach expands the ERP implementation services market by requiring system integrators to design secure network overlays, latency-aware data pipelines, and standardized integration patterns. By 2031, hybrid architectures are expected to underpin compliance in sectors dealing with personally identifiable information, national security data, and regulated financial records, reinforcing their role as a long-term bridge between legacy investments and full-cloud aspirations.

Geography Analysis

North America generated 37% of 2025 revenue, supported by compliance-driven refresh cycles in financial services and healthcare, and by the 2024 U.S. federal cloud mandate, which channels USD 3.5 billion per year into cloud ERP. Canada is consolidating provincial systems to cut operating costs, and Mexico's automotive exporters are modernizing their ERPs to meet United States-Mexico-Canada Agreement traceability requirements. Implementation partners with FedRAMP accreditation both dominate federal work and cross-sell similar governance frameworks to regulated private sectors.

The Middle East is the fastest-growing region, charting a 16% CAGR over 2026-2031. Saudi Arabia's Vision 2030 and the UAE's cloud-first federal policy have banned fresh on-premises ERP purchases for government agencies, funneling USD 1.2 billion annually into local hyperscaler regions. Projects such as NEOM showcase integrated ERP platforms managing construction, utilities, and municipal services for an eventual population of 1 million, providing a marquee reference for Gulf Cooperation Council smart-city initiatives.

Asia-Pacific is bifurcated. China's Data Security Law forces state-owned manufacturers onto domestic ERP stacks, raising integration complexity and cost, while India's Digital India subsidies encourage SMEs to adopt global cloud platforms. Japan leverages ERP-IoT fusion to offset labor shortages, and Australia's public sector pursues cloud ERP to bolster transparency. Europe is focusing on embedding sustainability and cyber-resilience metrics into ERP systems to comply with the Corporate Sustainability Reporting Directive. South America and Africa remain nascent but show pockets of activity in Brazil, Argentina, South Africa, and Nigeria, where electronic invoicing and core banking upgrades anchor demand.

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- International Business Machines Corporation

- Capgemini SE

- Infosys Limited

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- SAP SE

- Oracle Corporation

- Tech Mahindra Limited

- HCL Technologies Limited

- DXC Technology Company

- CGI Inc.

- NTT DATA Corporation

- Atos SE

- PricewaterhouseCoopers International Limited

- KPMG International Limited

- Fujitsu Limited

- Hitachi Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition * Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Digital Transformation Mandates

- 4.2.2 Surge in Real-Time Data-Driven Decision Making

- 4.2.3 Rapid Subscription-Based ERP Uptake Among SMEs

- 4.2.4 Compliance-Induced ERP Modernisation in Regulated Sectors

- 4.2.5 AI-Enabled Automated Configuration and Testing (under-reported)

- 4.2.6 Vertical-Specific Composable Micro-Service Frameworks (under-reported)

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Brownfield Integrations

- 4.3.2 Shortage of Skilled ERP Functional Consultants

- 4.3.3 Data Sovereignty Barriers in Multi-Tenant Environments (under-reported)

- 4.3.4 Vendor Lock-In Risks with Low-Code Extension Platforms (under-reported)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By End-Use Industry

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-Commerce

- 5.3.3 Banking, Financial Services and Insurance

- 5.3.4 Healthcare

- 5.3.5 Government and Public Sector

- 5.3.6 IT and Telecom

- 5.3.7 Other End-Use Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 International Business Machines Corporation

- 6.4.4 Capgemini SE

- 6.4.5 Infosys Limited

- 6.4.6 Tata Consultancy Services Limited

- 6.4.7 Wipro Limited

- 6.4.8 Cognizant Technology Solutions Corporation

- 6.4.9 SAP SE

- 6.4.10 Oracle Corporation

- 6.4.11 Tech Mahindra Limited

- 6.4.12 HCL Technologies Limited

- 6.4.13 DXC Technology Company

- 6.4.14 CGI Inc.

- 6.4.15 NTT DATA Corporation

- 6.4.16 Atos SE

- 6.4.17 PricewaterhouseCoopers International Limited

- 6.4.18 KPMG International Limited

- 6.4.19 Fujitsu Limited

- 6.4.20 Hitachi Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment