PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065596

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065596

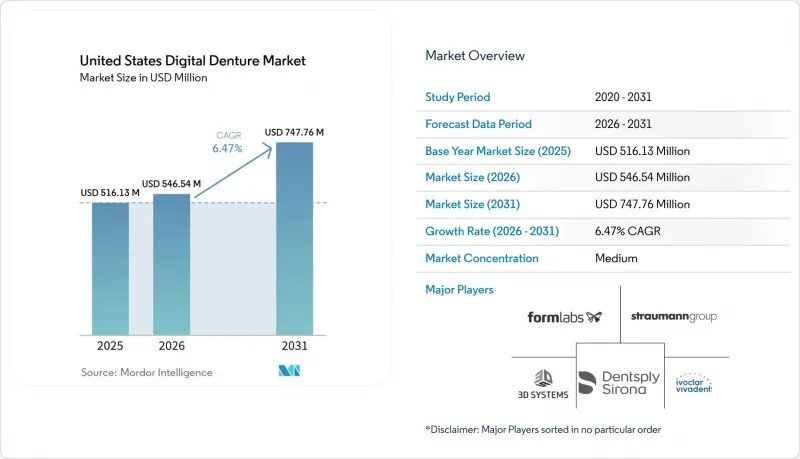

United States Digital Denture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states digital denture market size is projected to expand from USD 516.13 million in 2025 and USD 546.54 million in 2026 to USD 747.76 million by 2031, registering a CAGR of 6.47% between 2026 to 2031.

This report is Segmented by Product Type (Complete, Partial, Implant-Supported, Fixed Hybrid), Manufacturing Route (Milling, Vat Photopolymerization, Material Jetting, Hybrid), Material (PMMA/Acrylic, Composite/Hybrid, Flexible Nylon, Metal Frameworks), Application (Definitive, Immediate, Duplicate, Try-In), and End User (Dental Labs, Clinics, Dsos, Academic Centers). Forecasts are in Value (USD).

United States Digital Denture Market Trends and Insights

CAD/CAM and 3D Printing Adoption Redefines Laboratory Economics

The shift toward digital denture production has moved well beyond an early adoption phase in the U.S. laboratory base, because software-guided design and automated output now change labor use, remake rates, and turnaround times in the same workflow. Commercial laboratories are increasingly using digital case design to standardize tooth setup, preserve archived files, and reduce the variability that traditionally came from hand-built processes. Multi-material jetting is especially important because it turns the denture base and teeth into a single printed structure, which removes a manual bonding stage that often created both labor drag and quality risk. In July 2025, 3D Systems said beta customers using its NextDent 300 MultiJet platform achieved production speeds up to 300% faster than analog workflows and 120% faster than conventional 2-part printing, which shows why throughput has become a major purchase criterion. At the same time, a 2025 meta-analysis in Scientific Reports found that milled PMMA denture bases still showed stronger flexural performance and hardness than many printed alternatives, which means additive workflows still depend heavily on material formulation and post-cure control to narrow the gap. In the digital denture market, that balance between faster output and dependable mechanical performance is pushing vendors to compete on validated systems rather than on printer specifications alone.

Aging Edentulous Senior Base Provides Durable Demand Floor

The aging patient base remains the most durable source of case demand, but its importance goes beyond simple volume because it favors workflows that reduce visits, simplify remakes, and preserve design records over time. The American College of Prosthodontics states that 36 million Americans are fully edentulous, 120 million are missing at least 1 tooth, and 2.5 million Americans receive their first denture each year, which keeps the prosthetic replacement pool structurally large. The same organization also notes that 90% of fully edentulous Americans use dentures, which supports a stable installed base for relines, replacements, and duplicate prostheses. This is where digital archiving becomes commercially important, because older patients, especially those with lower mobility, benefit when an exact-fit backup can be produced without repeating full impression and design steps. Research published in Frontiers in Dental Medicine in 2025 states that the U.S. population aged 65 and older is expected to reach 98 million in coming decades, while access gaps remain significant for low-income, rural, and minority seniors. For the digital denture market, that combination of aging demand and uneven access suggests long-term volume support, with the strongest upside likely where service delivery models improve convenience and affordability at the same time.

High Capital Cost of Scanners, Printers, and Software Limits Independent Practice Adoption

The cost of a full digital setup still slows adoption among smaller operators, because the required investment often includes scanners, design software, printing or milling equipment, and post-processing tools rather than a single purchase. In the user-supplied range, a complete chairside or laboratory system usually requires USD 50,000 to USD 150,000, which places many independent practices and smaller regional laboratories in a wait-and-see position. That cost pressure also changes market structure, because high-throughput production is more likely to concentrate within DSOs and large commercial laboratories that can spread equipment costs across a higher case count. Open-material systems and financing options are easing part of the burden, but software subscriptions, upgrade cycles, depreciation, and material validation costs still make payback harder to judge for lower-volume operators. The Osseointegration Foundation of North America has also described a broader laboratory challenge that includes a shrinking number of U.S. labs, older technician workforces, and weaker training pipelines, all of which make fresh capital commitments harder to justify. In the digital denture market, this means the economic barrier is not only the printer or scanner price itself, but also the uncertainty around staffing, volume, and the time required to build a reliable digital workflow.

Other drivers and restraints analyzed in the detailed report include:

- FDA-Cleared Monolithic and Antimicrobial Denture Materials Expand the Defensible Product Portfolio

- DSO-Led Digitization and Procurement Accelerates Technology Standardization

- Coverage Gaps and Out-Of-Pocket Affordability Suppress Clinical Conversion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Partial Digital Dentures held 52.39% of the segment mix in 2025, while Complete Digital Dentures are projected to record the fastest growth at a 9.28% CAGR from 2026 to 2031. Partial dentures held the larger base because partial tooth loss remains the more common clinical presentation across the broad adult population that enters removable prosthetic care before full edentulism sets in. Laboratories also had a longer runway to digitize partial workflows, which gave this category an earlier commercial foundation than fully digital full-arch cases. Complete digital cases are now gaining speed because they align well with file-based design, repeatable tooth arrangement, and fewer manual production steps once the workflow is set. The 2025 expert consensus published in the International Journal of Oral Science described fully digital complete denture fabrication as clinically sound, more precise, and preferred by patients because it reduces chair time, which supports broader acceptance in routine practice.

These product lines still serve different economic roles inside the digital denture market. Partial dentures continue to anchor present revenue because they address a larger pool of partially edentulous patients and fit comfortably within existing laboratory and clinic habits. Complete dentures are expanding faster because the value of duplicate fabrication, digital storage, and full-arch efficiency becomes more visible once the full denture process is digitized from the start. Implant-Supported Overdentures sit in a more differentiated tier, since they combine removable prosthetics with implant planning and attachment-based workflows that are less exposed to basic price competition. Fixed Hybrid Full-Arch Dentures remain the highest value case type in many digital settings, and they reward laboratories that have already invested in advanced design software, guided planning, and tighter coordination with surgical teams.

Vat Photopolymerization 3D Printing led the route mix with 47.23% in 2025, while Material Jetting and Multi-Material Monolithic Printing are forecast to expand at a 9.92% CAGR through 2031. Vat photopolymerization led the way because SLA, DLP, and related systems had already spread across commercial laboratories, dental schools, and many digital prosthetic workflows before newer monolithic options reached full commercial readiness. Within this route, faster plate throughput and lower energy cost per arch are making DLP and LCD-style production more practical for mid-tier laboratories that need reliable volume without the capital profile of more advanced systems. Subtractive milling still keeps a meaningful role because mechanical performance remains a major concern in definitive prosthetics and premium applications. The 2025 Scientific Reports review found that milled PMMA bases delivered stronger flexural performance, better hardness, and stronger dimensional consistency than many 3D-printed alternatives, which continues to support milling in accuracy-sensitive cases.

The fastest momentum is now shifting toward monolithic output, which is why this part of the digital denture market is drawing so much attention from equipment suppliers. 3D Systems said its NextDent 300 MultiJet platform delivered production gains of up to 300% over analog workflows and 120% over conventional 2-part printing in beta settings, largely because it removes the bonding step between base and teeth. Hybrid print-and-bond workflows remain important during this transition because they let laboratories use digital production in stages without retiring existing equipment too quickly. That matters for operators who want better turnaround and workflow digitization but still need to manage capital exposure carefully. FDA 510(k) clearance also remains central across route choices, because it reduces the compliance risk that laboratories and clinicians weigh when choosing between a familiar system and a newer one.

List of Companies Covered in this Report:

- 3D Systems

- 3 Shape

- Amann Girrbach

- AvaDent Digital Dental Solutions

- Asiga

- BEGO USA, Inc.

- Bruin Biometrics, LLC

- Carbon, Inc.

- DENTCA, Inc.

- Desktop Health

- Dentsply Sirona

- DGSHAPE Americas

- Formlabs, Inc.

- Glidewell Dental

- Ivoclar Vivadent

- Keystone Industries

- Kulzer

- Straumann Group

- SprintRay

- Stratasys

- VITA Zahnfabrik H. Rauter GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Edentulous Senior Base

- 4.2.2 CAD/CAM and 3D Printing Adoption

- 4.2.3 DSO-Led Digitization and Procurement

- 4.2.4 Demand For Implant-Retained and Aesthetic Prosthetics

- 4.2.5 FDA-Cleared Monolithic and Antimicrobial Denture Materials

- 4.2.6 Digital Archives Enable Duplicate Dentures and Fewer Visits

- 4.3 Market Restraints

- 4.3.1 High Capital Cost of Scanners Printers, and Software

- 4.3.2 Coverage Gaps and Out-Of-Pocket Affordability

- 4.3.3 Technician Pipeline and Digital Training Gaps

- 4.3.4 Workflow Standardization and Material-Validation Gaps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Complete Digital Dentures

- 5.1.2 Partial Digital Dentures

- 5.1.3 Implant-Supported Overdentures

- 5.1.4 Fixed Hybrid Full-Arch Dentures

- 5.2 By Manufacturing Route

- 5.2.1 Subtractive Milling

- 5.2.2 Vat Photopolymerization 3D Printing

- 5.2.2.1 SLA-Based Workflows

- 5.2.2.2 DLP / LCD-Based Workflows

- 5.2.3 Material Jetting / Multi-Material Monolithic Printing

- 5.2.4 Hybrid Print-And-Bond Workflows

- 5.3 By Material

- 5.3.1 PMMA / Acrylic Resin

- 5.3.2 Composite / Hybrid Resin

- 5.3.3 Flexible Nylon / Polyamide

- 5.3.4 Metal-Supported Frameworks

- 5.4 By Application

- 5.4.1 Definitive Dentures

- 5.4.2 Immediate Dentures

- 5.4.3 Duplicate / Backup Dentures

- 5.4.4 Try-In and Provisional Dentures

- 5.5 By End User

- 5.5.1 Dental Laboratories

- 5.5.2 Independent Dental Clinics and Hospitals

- 5.5.3 DSOs And Group Practices

- 5.5.4 Academic and Hospital-Affiliated Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3D Systems, Inc.

- 6.3.2 3Shape A/S

- 6.3.3 Amann Girrbach AG

- 6.3.4 AvaDent Digital Dental Solutions

- 6.3.5 Asiga

- 6.3.6 BEGO USA, Inc.

- 6.3.7 Bruin Biometrics, LLC

- 6.3.8 Carbon, Inc.

- 6.3.9 DENTCA, Inc.

- 6.3.10 Desktop Health

- 6.3.11 Dentsply Sirona Inc.

- 6.3.12 DGSHAPE Americas

- 6.3.13 Formlabs, Inc.

- 6.3.14 Glidewell Dental

- 6.3.15 Ivoclar Vivadent AG

- 6.3.16 Keystone Industries

- 6.3.17 Kulzer GmbH

- 6.3.18 Straumann Group

- 6.3.19 SprintRay Inc.

- 6.3.20 Stratasys Ltd.

- 6.3.21 VITA Zahnfabrik H. Rauter GmbH & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment