PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065599

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065599

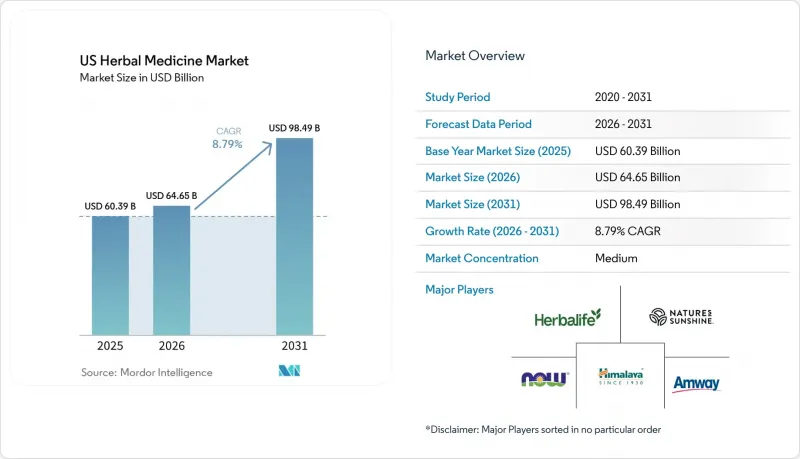

US Herbal Medicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the uS herbal medicine market size was valued at USD 60.39 billion in 2025 and is estimated to grow from USD 64.65 billion in 2026 to reach USD 98.49 billion by 2031, at a CAGR of 8.79% during the forecast period (2026-2031).

This report is Segmented by Product Type (Herbal Pharmaceuticals, Dietary Supplements, and More), Source (Leaves, Roots & Rhizomes, and More), Form (Tablets & Capsules, Powder & Granules, and More), Distribution Channel (Hospitals & Retail Pharmacies, and More), and Medicinal Plant Type (Aloe Vera, Echinacea, Turmeric, Ginseng, Ginger, Garlic, Ginkgo Biloba, Others). Forecasts in Value (USD).

US Herbal Medicine Market Trends and Insights

Preventive Self-Care and Natural-Remedy Preference

Preventive health behavior is driving the US herbal medicine market, shifting focus from occasional illness responses to daily wellness routines. Older adults remain key contributors, maintaining supplement spending despite financial constraints, which highlights consistent demand. Consumers increasingly prefer products aligned with long-term wellness goals, as seen in 2024 retail trends where ashwagandha sales rose while elderberry declined. This shift favors premium, evidence-backed products over value offerings, strengthening revenue stability through regimen use rather than one-time purchases.

Aging Population and Chronic-Condition Self-Management

The aging population, projected to reach 73 million by 2030, significantly influences the US herbal medicine market. Older adults frequently use turmeric and Boswellia for inflammation, ginkgo biloba and ginseng for cognition, and berberine and cinnamon for blood sugar support. Many purchases are driven by consumer research rather than physician recommendations, creating opportunities for education-driven digital sales models. Transparency in herb-drug interactions is critical, as older consumers often manage multiple therapies simultaneously.

Import Dependence and Tariff Volatility for Non-Native Botanicals

In 2026, the US herbal medicine market faces significant challenges due to its reliance on imports. Approximately 40% of U.S. dietary supplement herb imports come from India, while 80% of raw supplement ingredient volume is sourced from China, exposing brands to price volatility and supply disruptions. Tariff actions have further increased costs, with Chinese botanicals facing a 145% tariff burden and Indian botanicals like turmeric, ashwagandha, and Boswellia encountering a 50% to 55% burden. India produces 78% of the world's turmeric and is the sole cultivator of Boswellia serrata, making quick substitutions difficult. Smaller companies must navigate between reduced margins and higher retail prices, emphasizing the need for strategic inventory planning and supplier diversification.

Other drivers and restraints analyzed in the detailed report include:

- GLP-1 Support Routines Lifting Digestive and Metabolic Herbs

- E-Commerce and DTC Discovery Expansion

- Limited Clinical Substantiation for Many Herbal Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Herbal Pharmaceuticals held 30.44% of the US herbal medicine market. Herbal Dietary Supplements are projected to grow at a 9.42% CAGR through 2031, driven by the strong institutional presence of standardized botanical formulations in pharmacy and hospital channels. These products benefit from a focus on consistency, documentation, and third-party verification, giving pharmaceutical-grade offerings an edge in compliance-driven settings.

Herbal Dietary Supplements are expanding rapidly due to their alignment with consumer self-education, adaptogen use, and direct-to-consumer distribution. The projected growth reflects increasing consumer interest in managing stress, sleep, metabolic health, and daily wellness outside traditional prescriptions. Additionally, Herbal Functional Food and Beverages are gaining traction as mainstream food companies seek plant-based positioning and easier integration into daily routines.

Roots & Rhizomes held a 42.79% share in 2025 and are the fastest-growing source segment, with a projected 9.05% CAGR through 2031. This growth is driven by the commercial and clinical importance of root-derived actives like ginseng saponins, turmeric curcuminoids, and ashwagandha withanolides. These ingredients are widely recognized by consumers and formulators and are adaptable across various delivery formats.

The segment is expected to maintain its leadership as advancements in formulation enhance the performance of these actives in commercial products. Improved absorption and targeted biological effects support higher-value positioning while retaining familiar ingredient names. Traceable domestic cultivation for select botanicals strengthens provenance narratives, although many high-demand inputs still rely on overseas sources.

List of Companies Covered in this Report:

- Amway Corp.

- Ancient Brands, LLC

- Gaia Herbs, Inc.

- Garden of Life, LLC

- GNC Holdings, LLC

- Herb Pharm, LLC

- Herbalife Ltd.

- Herbalist & Alchemist, Inc.

- Himalaya

- Irwin Naturals Inc.

- Life Extension Foundation Buyers Club, Inc.

- Nature's Sunshine Products, Inc.

- Nature's Way Products, LLC

- New Chapter, Inc.

- NOW Health Group, Inc.

- Pharmavite LLC

- Solgar, Inc.

- Swanson Health Products, Inc.

- The Bountiful Company

- Traditional Medicinals, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Preventive Self-Care and Natural-Remedy Preference

- 4.2.2 Clean-Label and Plant-Based Premiumization

- 4.2.3 E-Commerce and DTC Discovery Expansion

- 4.2.4 Aging Population and Chronic-Condition Self-Management

- 4.2.5 GLP-1 Support Routines Lifting Digestive and Metabolic Herbal Demand

- 4.2.6 Integrative Wellness Adoption by Millennials and Gen Z

- 4.3 Market Restraints

- 4.3.1 Limited Clinical Substantiation for Many Herbal Claims

- 4.3.2 Ingredient Quality Variability and Adulteration Risk

- 4.3.3 Import Dependence and Tariff Volatility for Non-Domestic Botanicals

- 4.3.4 Contamination and Recall Exposure in Fast-Growth Botanicals

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Herbal Pharmaceuticals

- 5.1.2 Herbal Dietary Supplements

- 5.1.3 Herbal Functional Food & Beverages

- 5.1.4 Herbal Cosmetics & Personal Care

- 5.2 By Source (Plant Part)

- 5.2.1 Leaves

- 5.2.2 Roots & Rhizomes

- 5.2.3 Whole Plant

- 5.2.4 Fruits & Seeds

- 5.2.5 Flowers & Bark

- 5.3 By Form

- 5.3.1 Tablets & Capsules

- 5.3.2 Powder & Granules

- 5.3.3 Liquid Extracts & Syrups

- 5.3.4 Teas & Infusions

- 5.3.5 Others (Soft gel and Gummies, among others)

- 5.4 By Distribution Channel

- 5.4.1 Hospitals & Retail Pharmacies

- 5.4.2 Online/ E-Commerce

- 5.4.3 Specialty Stores

- 5.4.4 Hypermarkets & Supermarkets

- 5.5 By Medicinal Plant Type

- 5.5.1 Aloe Vera

- 5.5.2 Echinacea

- 5.5.3 Turmeric (Curcuma Longa)

- 5.5.4 Ginseng

- 5.5.5 Ginger

- 5.5.6 Garlic

- 5.5.7 Ginkgo Biloba

- 5.5.8 Others (Ashwagandha and Cinnamon, among others)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amway Corp.

- 6.3.2 Ancient Brands, LLC

- 6.3.3 Gaia Herbs, Inc.

- 6.3.4 Garden of Life, LLC

- 6.3.5 GNC Holdings, LLC

- 6.3.6 Herb Pharm, LLC

- 6.3.7 Herbalife Ltd.

- 6.3.8 Herbalist & Alchemist, Inc.

- 6.3.9 Himalaya Wellness Company

- 6.3.10 Irwin Naturals Inc.

- 6.3.11 Life Extension Foundation Buyers Club, Inc.

- 6.3.12 Nature's Sunshine Products, Inc.

- 6.3.13 Nature's Way Products, LLC

- 6.3.14 New Chapter, Inc.

- 6.3.15 NOW Health Group, Inc.

- 6.3.16 Pharmavite LLC

- 6.3.17 Solgar, Inc.

- 6.3.18 Swanson Health Products, Inc.

- 6.3.19 The Bountiful Company

- 6.3.20 Traditional Medicinals, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment