PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065600

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065600

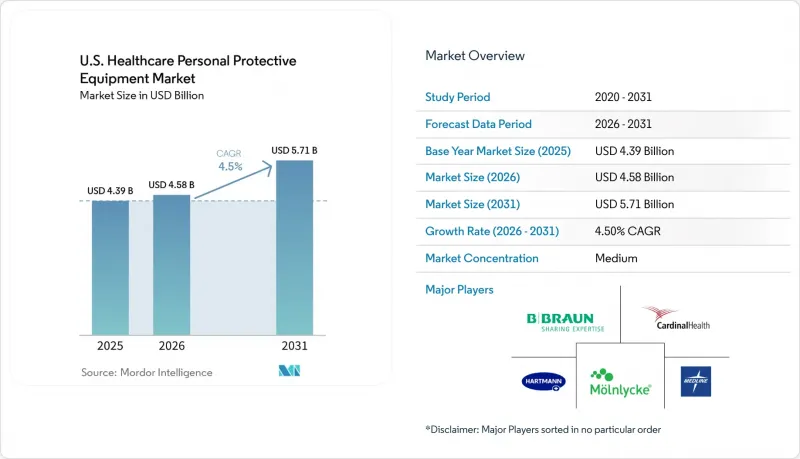

U.S. Healthcare Personal Protective Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. healthcare personal protective equipment market size is projected to be USD 4.39 billion in 2025, USD 4.58 billion in 2026, and reach USD 5.71 billion by 2031, growing at a CAGR of 4.5% from 2026 to 2031.

This report is Segmented by Product Type (Hand Protection, Protective Clothing, Respiratory Protection, Face Protection, Eye Protection, Others) and End User (Hospitals, Ambulatory and Outpatient Care, Home Healthcare, Diagnostic and Laboratory Settings, Others). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Healthcare Personal Protective Equipment Market Trends and Insights

Healthcare-Associated Infection Control Compliance

In the U.S., hospitals increasingly view adherence to PPE protocols as both a clinical necessity and a financial priority. Healthcare-associated infections remain a significant challenge, with approximately 1.7 million incidents occurring annually in U.S. hospitals. This ensures the consistent use of gloves, gowns, masks, and respiratory protection in patient care. CMS has introduced updates to NHSN HAI measures, effective FY 2029, under the Hospital-Acquired Condition Reduction Program. As performance standards tighten, procurement teams face growing pressure to prioritize compliance-driven PPE purchasing, solidifying its role in the U.S. healthcare PPE market.

Aging Patient Base And Higher Clinical-Touch Volumes

The aging U.S. population is driving increased demand for PPE due to the higher care intensity required for older patients. These patients often need extended monitoring, longer hospital stays, and more frequent staff interactions, leading to greater usage of gloves, gowns, and respiratory protection. This trend extends beyond hospitals to home-based and ambulatory care settings, where infection control remains critical. Consequently, the aging demographic is strengthening the demand base of the U.S. healthcare PPE market, even as overall growth remains steady.

Post-Pandemic Inventory Digestion And Price Resets

The U.S. healthcare PPE market continues to face challenges stemming from pandemic-era overstocking. Major health systems are managing surplus inventories of gloves, isolation gowns, and masks, which has slowed reorder activity despite consistent clinical usage. Suppliers are navigating stable demand but reduced purchasing momentum. Additionally, trade and sourcing policy discussions are emphasizing concerns over import reliance and procurement costs. Short-term revenue remains under pressure, reflecting inventory clearance delays, price adjustments, and uneven restocking.

Other drivers and restraints analyzed in the detailed report include:

- Strategic Stockpiling And Domestic Sourcing Mandates

- Care Migration To Outpatient And Home Settings

- Hospital Margin Pressure And SKU Rationalization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hand protection captured 38.50% of U.S. healthcare PPE market share in 2025, making it the largest product category in the U.S. healthcare PPE market. Hand protection dominates the U.S. healthcare PPE market, holding the largest share due to the widespread use of gloves in patient interactions across various care settings. Examination gloves see the highest consumption due to routine usage, while surgical gloves remain a premium segment driven by procedure volumes, sterility needs, and clinician preferences. Respiratory protection also holds strategic importance as health systems maintain preparedness standards, supported by regulatory guidance on air-purifying respirators.

Protective clothing is projected to grow at the fastest CAGR through 2031, driven by increased demand for isolation and surgical gowns as procedural activities expand across care environments. Domestic sourcing rules enhance the strategic importance of gowns, while AAMI barrier classifications guide purchasing decisions by balancing comfort, exposure risk, and procedure complexity. Face and eye protection categories, though smaller, benefit from ongoing standardization in infection control practices.

List of Companies Covered in this Report:

- 3M

- Alpha Pro Tech, Ltd.

- Ansell

- Armbrust American

- B. Braun

- Cardinal Health

- DeRoyal Industries

- DuPont

- Lakeland Industries, Inc.

- Medicom Group

- Medline Inc.

- Moldex-Metric, Inc.

- Molnlycke Health Care

- MSA Safety Incorporated

- O&M Halyard, Inc.

- Owens & Minor, Inc.

- Hartmann Group

- Prestige Ameritech

- SafeSource Direct, LLC

- Top Glove Corporation Bhd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Healthcare-Associated Infection Control Compliance

- 4.2.2 Aging Patient Base and Higher Clinical-Touch Volumes

- 4.2.3 Strategic Stockpiling and Domestic Sourcing Mandates

- 4.2.4 Care Migration to Outpatient and Home Settings

- 4.2.5 Reusable Respiratory PPE for Preparedness and Total Cost of Ownership

- 4.2.6 Tariff-Driven Preference for U.S.-Made Supply

- 4.3 Market Restraints

- 4.3.1 Post-Pandemic Inventory Digestion and Price Resets

- 4.3.2 Hospital Margin Pressure and SKU Rationalization

- 4.3.3 Fit-Testing and Program Burden for Advanced Respirators

- 4.3.4 Waste and Sustainability Scrutiny of Single-Use PPE

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining power of suppliers

- 4.7.2 Bargaining power of buyers

- 4.7.3 Threat of new entrants

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Hand Protection

- 5.1.1.1 Examination gloves

- 5.1.1.2 Surgical gloves

- 5.1.2 Protective Clothing

- 5.1.2.1 Isolation gowns

- 5.1.2.2 Surgical gowns

- 5.1.2.3 Coveralls

- 5.1.2.4 Lab coats and procedure apparel

- 5.1.2.5 Headwear and footwear

- 5.1.3 Respiratory Protection

- 5.1.3.1 Surgical N95 respirators

- 5.1.3.2 Standard N95 respirators used in care settings

- 5.1.3.3 Elastomeric half-mask respirators

- 5.1.3.4 Powered air-purifying respirators

- 5.1.4 Face Protection

- 5.1.5 Eye Protection

- 5.1.6 Others

- 5.1.1 Hand Protection

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory and Outpatient Care

- 5.2.3 Home Healthcare

- 5.2.4 Diagnostic and Laboratory Settings

- 5.2.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Alpha Pro Tech, Ltd.

- 6.3.3 Ansell Limited

- 6.3.4 Armbrust American

- 6.3.5 B. Braun Melsungen AG

- 6.3.6 Cardinal Health, Inc.

- 6.3.7 DeRoyal Industries, Inc.

- 6.3.8 DuPont de Nemours, Inc.

- 6.3.9 Lakeland Industries, Inc.

- 6.3.10 Medicom Group

- 6.3.11 Medline Inc.

- 6.3.12 Moldex-Metric, Inc.

- 6.3.13 Molnlycke Health Care AB

- 6.3.14 MSA Safety Incorporated

- 6.3.15 O&M Halyard, Inc.

- 6.3.16 Owens & Minor, Inc.

- 6.3.17 PAUL HARTMANN AG

- 6.3.18 Prestige Ameritech

- 6.3.19 SafeSource Direct, LLC

- 6.3.20 Top Glove Corporation Bhd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment