PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065603

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065603

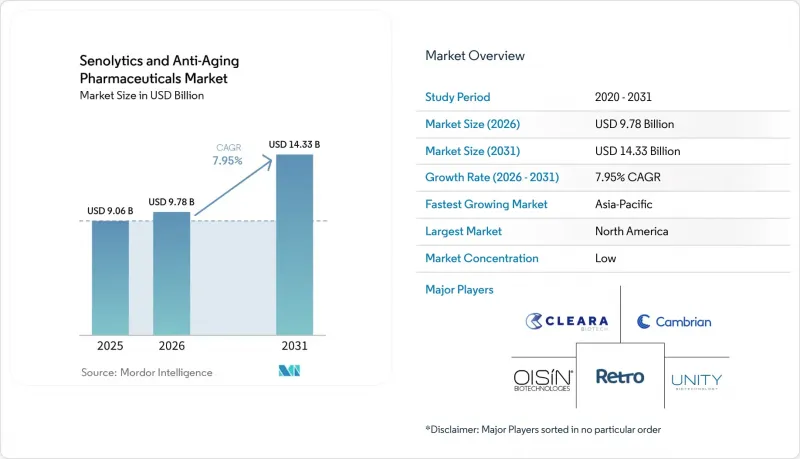

Senolytics And Anti-Aging Pharmaceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the senolytics and anti-Aging pharmaceuticals market size is expected to grow from USD 9.06 billion in 2025 to USD 9.78 billion in 2026 and is forecast to reach USD 14.33 billion by 2031 at 7.95% CAGR over 2026-2031.

This report is Segmented by Drug Class (Senolytics, Anti-Aging Pharmaceutical), Application (Clinical Use, Consumer Wellness), End User (Hospitals and Clinics, Biopharma and Virtual Biotechs, Longevity Clinics, Others), Distribution (Prescription, OTC/Supplements, Clinical Trials), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Senolytics And Anti-Aging Pharmaceuticals Market Trends and Insights

Rising Burden of Age-Related Chronic Diseases

The senolytics and anti-aging pharmaceuticals market continues to derive strong demand from the prevalence of chronic diseases in aging populations. In 2021, the global population aged 70 and older reached 494.4 million, with ischemic heart disease, stroke, and COPD as leading causes of death, all linked to senescence-related mechanisms. A 2025 study projected 75.5 million global deaths from non-communicable diseases by 2050, with cardiovascular disease as the largest contributor. As life expectancy increases without a proportional rise in healthy years, healthcare priorities are shifting toward therapies that reduce morbidity rather than merely extending survival. This positions the market at the intersection of medical need, payer interest, and preventive health demand.

Expanding Geroscience R&D Funding and Private Capital

Increased funding for geroscience programs is driving the senolytics and anti-aging pharmaceuticals market. Longevity investments rose to USD 8.49 billion across 325 deals in 2024, up from USD 3.82 billion in 2023, with 31% of the capital allocated to later-stage ventures. Investors are favoring milestone-driven platforms over open-ended research. Acquisition activity is also rising, as companies with promising clinical signals in regulated indications attract larger pharmaceutical players seeking faster market entry. Early proof-of-concept results are becoming critical for securing capital and advancing toward regulatory approval.

Unclear Regulatory Pathway for Aging Indications

The market for senolytics and anti-aging drugs faces significant regulatory challenges. Aging is not officially recognized as a disease, making it difficult for sponsors to demonstrate the efficacy of anti-aging treatments. Research must focus on specific age-related conditions like fibrosis, retinal diseases, frailty, or neurodegeneration, which fragments development, extends timelines, and limits data pooling. Additionally, payers may question the value of senescence clearance compared to established off-label drugs. For companies in this market, regulatory strategies are as critical as biological advancements, particularly when converting broad healthspan claims into disease-specific endpoints.

Other drivers and restraints analyzed in the detailed report include:

- Clinical Proof-of-Concept in Ophthalmology, Fibrosis, Frailty, and Kidney Disease

- Platform Diversification Beyond Small Molecules

- Off-Target Toxicity and Narrow Therapeutic Windows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Anti-Aging Pharmaceuticals accounted for 72.95% of revenue, maintaining its lead in the senolytics and anti-aging pharmaceuticals market. This reflects the commercial maturity of NAD+ precursors, rapamycin-related therapies, and hormone-modulating products, which are accessible through prescription and over-the-counter channels. These products generate revenue as they are available without waiting for first-in-class senolytic approvals.

Senolytics are projected to grow at an 8.15% CAGR through 2031, outpacing the overall market growth. The pipeline includes small molecules, gene-based constructs, immune-directed strategies, and precision reprogramming concepts, highlighting growth driven by modality diversity. As results emerge in areas like ocular health, fibrosis, frailty, and inflammation, the gap between current revenue leaders and future pipeline potential is expected to narrow.

In 2025, Clinical Use and Off-label Therapeutics held 60.95% of the market, making it the largest application segment. This is driven by the use of established agents like dasatinib, rapamycin, and metformin in defined medical settings. Academic medical centers and specialist clinics play a key role by combining trial enrollment, compassionate use, and protocol-based prescribing.

Consumer Wellness and Longevity Use is expected to grow at an 8.35% CAGR through 2031, making it the fastest-growing application. Growth is supported by wider biomarker access, direct-to-consumer diagnostics, and a shift from niche biohacking to mainstream healthspan management. Longevity programs increasingly use tools like biological age clocks and inflammatory panels to track responses, enhancing credibility.

Geography Analysis

In 2025, North America accounted for 41.12% of the revenue share in the senolytics and anti-aging pharmaceuticals market, making it the largest regional contributor. This leadership is driven by advanced clinical infrastructure, concentrated venture capital, and a growing network of physician-led longevity and preventive medicine clinics. The United States remains the key player due to its high concentration of clinical-stage longevity biotech firms that influence valuations, trial activities, and partnerships across the market.

Europe remains a significant region in the senolytics and anti-aging pharmaceuticals market, combining a strict regulatory framework with active scientific involvement in senescence research. Countries like Germany, the U.K., France, Italy, and Spain support both consumer adoption of anti-aging solutions and clinical-stage therapeutic advancements. The U.K. contributes through companies such as Genflow Biosciences and Juvenescence, while EU nations back early-phase programs in dermatology and fibrosis-related areas.

Asia-Pacific is the fastest-growing region in the senolytics and anti-aging pharmaceuticals market, with a projected CAGR of 11.37% through 2031. China and Japan drive this growth due to rising demand for aging-related solutions and increasing commercial interest in anti-aging products. Japan's April 2026 launch of SenoRich highlights the region's progress, showcasing both clinical potential and visible retail activity.

- Altos Labs, Inc.

- BioAge Labs, Inc.

- Calico Life Sciences LLC

- Cambrian BioPharma, Inc.

- Cleara Biotech B.V.

- Deciduous Therapeutics Inc.

- Genflow Biosciences plc

- Halia Therapeutics, Inc.

- Juvenescence Limited

- Life Biosciences, Inc.

- NewLimit, Inc.

- Oisin Biotechnologies

- Rejuvenate Bio, Inc.

- Repair Biotechnologies, Inc.

- Retro Biosciences, Inc.

- Rubedo Life Sciences, Inc.

- SIWA Therapeutics, Inc.

- Telomir Pharmaceuticals, Inc.

- Turn Biotechnologies, Inc.

- UNITY Biotechnology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Age-Related Chronic Diseases

- 4.2.2 Expanding Geroscience R&D Funding and Private Capital

- 4.2.3 Clinical Proof-of-Concept in Ophthalmology, Fibrosis, Frailty, and Kidney Disease

- 4.2.4 Platform Diversification Beyond Small Molecules into Gene, Immune, and Rejuvenation Therapies

- 4.2.5 Senescence Atlas and Biomarker Infrastructure Improving Trial Stratification

- 4.2.6 Ophthalmology and Dermatology as Lower-Risk First Commercialization Wedges

- 4.3 Market Restraints

- 4.3.1 No Approved Aging Indication and Unclear Regulatory Pathway for Aging Claims

- 4.3.2 Off-Target Toxicity and Narrow Therapeutic Windows for Systemic Senolytics

- 4.3.3 Beneficial Senescence Biology Limits Indiscriminate Cell Clearance

- 4.3.4 Biomarker Heterogeneity Complicates Enrichment, Dosing Cadence, and Durable-Response Claims

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Senolytics

- 5.1.2 Anti -Aging Pharmaceutical

- 5.2 By Application

- 5.2.1 Clinical Use / Off-label Therapeutics

- 5.2.2 Consumer Wellness / Longevity Use

- 5.3 By End User

- 5.3.1 Hospital and Clinics

- 5.3.2 Biopharmaceutical Companies and Virtual Biotechs

- 5.3.3 Longevity and Preventive-Medicine Clinics

- 5.3.4 Others

- 5.4 By Distribution

- 5.4.1 Prescription-Based

- 5.4.2 Over-the-Counter (OTC) / Supplements

- 5.4.3 Clinical Trials / Compassionate Use

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Altos Labs, Inc.

- 6.3.2 BioAge Labs, Inc.

- 6.3.3 Calico Life Sciences LLC

- 6.3.4 Cambrian BioPharma, Inc.

- 6.3.5 Cleara Biotech B.V.

- 6.3.6 Deciduous Therapeutics Inc.

- 6.3.7 Genflow Biosciences plc

- 6.3.8 Halia Therapeutics, Inc.

- 6.3.9 Juvenescence Limited

- 6.3.10 Life Biosciences, Inc.

- 6.3.11 NewLimit, Inc.

- 6.3.12 Oisin Biotechnologies

- 6.3.13 Rejuvenate Bio, Inc.

- 6.3.14 Repair Biotechnologies, Inc.

- 6.3.15 Retro Biosciences, Inc.

- 6.3.16 Rubedo Life Sciences, Inc.

- 6.3.17 SIWA Therapeutics, Inc.

- 6.3.18 Telomir Pharmaceuticals, Inc.

- 6.3.19 Turn Biotechnologies, Inc.

- 6.3.20 UNITY Biotechnology, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment