PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065625

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065625

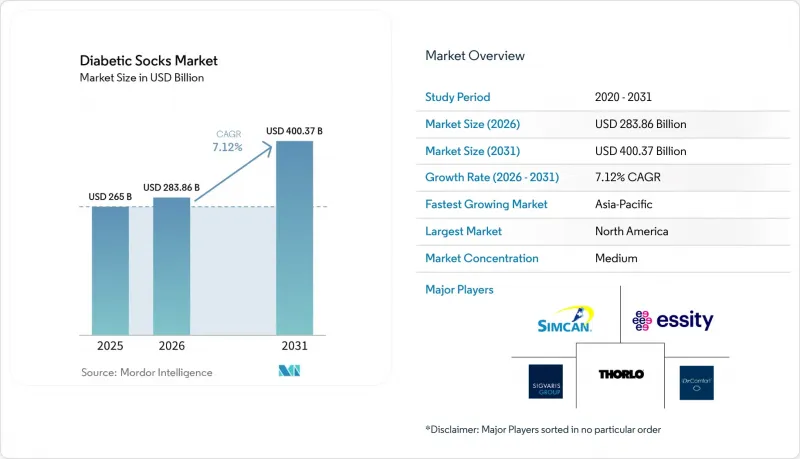

Diabetic Socks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the diabetic socks market size was valued at USD 265 billion in 2025 and is estimated to grow from USD 283.86 billion in 2026 to reach USD 400.37 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

This report is Segmented by Product Type (Ankle, Calf, Knee-High), Material (Cotton, Bamboo, Wool, Acrylic, Blends), Distribution Channel (Hypermarkets, Pharmacy, and More), End User (Male, Female, Unisex), Technology (Non-Binding, Compression, Copper-Infused, Smart Monitoring, Infrared), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Diabetic Socks Market Trends and Insights

Rising Diabetes Prevalence and Peripheral Neuropathy

The diabetic socks market is expanding due to the increasing global prevalence of diabetes. In 2024, 589 million adults were living with diabetes, a figure projected to reach 853 million by 2050, creating a growing demand for foot protection. Additionally, up to 50% of diabetes patients develop peripheral neuropathy, making friction-reducing and protective products essential for preventive care. Urban areas, with a 12.26% diabetes prevalence in 2024 compared to 9.23% in rural regions, enhance market accessibility through pharmacies, hospitals, and online platforms. Painful diabetic neuropathy, affecting 46.7% of patients with diabetic peripheral neuropathy, further drives demand for protective socks.

Greater Clinical Emphasis on Ulcer Prevention

The market is benefiting from a stronger clinical focus on ulcer prevention rather than post-complication treatment. Temperature-sensing diabetic socks have demonstrated significant reductions in foot ulcers, amputations, and outpatient visits, elevating their role in structured podiatric and endocrinology workflows. Clinicians are increasingly incorporating these socks into early-intervention protocols, supported by evidence that strengthens reimbursement prospects. Brands like THORLO differentiate themselves with clinical studies showcasing reduced foot pain, blisters, and moisture, setting them apart from general retail alternatives.

Premium Pricing Versus Ordinary Socks

The diabetic socks market faces affordability challenges in many regions, particularly where diabetes prevalence outpaces disposable income growth. Clinically designed socks are priced significantly higher than standard cotton alternatives, with premium brands ranging from USD 17 to USD 140, compared to basic options under USD 3. This disparity is critical as 81% of the global diabetic population resides in low- and middle-income countries with limited healthcare budgets. The cost gap is even wider for smart socks due to advanced features like temperature monitoring and connectivity. Without insurance or payer support, expanding premium and smart products to a broader audience remains challenging.

Other drivers and restraints analyzed in the detailed report include:

- Wider Retail and E-Commerce Availability of Diabetic Socks

- Fiber-Engineered Moisture and Friction Control

- Limited Awareness and Physician Recommendations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, calf length socks dominated the diabetic socks market, accounting for 68.10% of the product type segment. Their mid-leg coverage offers protection without knee restriction, making them versatile for casual, medical, and orthopedic footwear. These socks address areas prone to rubbing and pressure, aligning with preventive foot-care needs, and remain the market's volume anchor due to their balance of protection, comfort, and daily wear compatibility.

Ankle length socks are the fastest-growing product type, projected to grow at a 7.45% CAGR from 2026 to 2031. Their appeal lies in catering to active users preferring athletic footwear and lighter coverage in warm weather. Over-the-calf and knee-high variants, while offering advanced features, face cautious adoption due to clinical concerns. Circufiber's over-the-calf range addresses this by focusing on circulation support rather than compression, maintaining relevance in the market.

Cotton held 44.40% of the material segment in 2025, driven by its affordability, availability, and consumer familiarity. However, its clinical limitations, such as friction risks when wet, highlight the need for patient education on fiber choices as a health decision rather than a comfort preference.

Bamboo-based materials, with a forecasted 7.70% CAGR through 2031, are gaining traction for their antimicrobial, temperature-regulating, and sustainable properties, particularly in North America and Europe. Wool remains relevant in colder climates for insulation and pressure buffering, while acrylic and synthetic blends balance affordability and performance, ensuring their continued role in the market.

Geography Analysis

In 2025, North America led the diabetic socks market with a 40.12% share, driven by high diabetes prevalence, strong healthcare spending, and structured clinical pathways for diabetic foot care. CMS coverage for diabetic therapeutic shoes and related supplies under specific eligibility criteria has facilitated the transition of diabetic socks from retail interest to medically supported use. Additionally, the region's early adoption of connected products, such as smart socks, aligns with its care delivery and payer systems, reinforcing its market leadership.

Europe, led by Germany, the United Kingdom, France, Italy, and Spain, is another key player in the diabetic socks market. National health systems and referral pathways streamline the integration of diabetic foot products into routine care. Germany's strong adoption of compression hosiery supports established players like Jacob Rohner AG and Thuasne LLC through pharmacy and hospital channels. Sustainability is also becoming a differentiator, with companies like SIGVARIS GROUP France introducing waterless-dyed compression stockings and reducing water consumption in product lines, blending clinical and environmental priorities.

Asia-Pacific is the fastest-growing region in the diabetic socks market, projected to grow at a 9.35% CAGR through 2031. China and India, with a combined diabetic adult population exceeding 200 million in 2024, provide a strong volume base. However, uneven reimbursement and physician recommendations across countries highlight the need for diverse growth strategies. Online channels are bridging gaps in specialty retail infrastructure, while Japan stands out for its early adoption of advanced healthcare products and structured retail distribution. Orthofeet's distributor in Japan expanded to over 80 retail outlets by fall 2025, reflecting international brands' growing presence in the region.

- Aleva Stores

- Circufiber

- Crawford Knitting Company, Inc.

- Diabetic Sock Club

- Dr. Comfort, LLC

- Drymax Technologies Inc.

- Essity

- Jacob Rohner AG

- Medicool, Inc.

- Orthofeet, Inc.

- PediFix

- Rawganique

- SIGVARIS GROUP

- Simcan Enterprises Inc.

- Siren Care, Inc.

- Sweet Feet Diabetic Socks

- THORLO, Inc.

- Thuasne, LLC

- TN SOCKS & TIGHTS LTD

- Wigwam Mills, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes Prevalence and Neuropathy Burden

- 4.2.2 Greater Clinical Emphasis on Ulcer Prevention and Daily Foot Inspection

- 4.2.3 Wider Retail and E-Commerce Availability of Diabetic-Friendly Socks

- 4.2.4 Reimbursed Remote Temperature-Monitoring Sock Programs

- 4.2.5 Fiber-Engineered Moisture and Friction Control as Diabetic-Footwear Adjunct

- 4.3 Market Restraints

- 4.3.1 Premium Pricing Versus Ordinary Socks

- 4.3.2 Limited Awareness and Physician Recommendation in Emerging Markets

- 4.3.3 Guideline Caution on Compression or Knee-High Use Without Specialist Oversight

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Ankle Length

- 5.1.2 Calf Length

- 5.1.3 Over-the-calf / Knee-high

- 5.2 By Material

- 5.2.1 Cotton

- 5.2.2 Bamboo

- 5.2.3 Wool

- 5.2.4 Acrylic

- 5.2.5 Synthetic Blends

- 5.3 By Distribution Channel

- 5.3.1 Hypermarkets and Retail Chains

- 5.3.2 Pharmacy and Drug Stores

- 5.3.3 Online Retail

- 5.3.4 Specialty Medical Stores

- 5.4 By End User

- 5.4.1 Male

- 5.4.2 Female

- 5.4.3 Unisex

- 5.5 By Technology

- 5.5.1 Standard Non-binding Diabetic Socks

- 5.5.2 Compression Diabetic Socks

- 5.5.3 Antimicrobial / Copper-Infused Diabetic Socks

- 5.5.4 Smart Temperature-Monitoring Socks

- 5.5.5 Infrared / Circulation-Enhancing Socks

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.5.3.1 Saudi Arabia

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aleva Stores

- 6.3.2 Circufiber

- 6.3.3 Crawford Knitting Company, Inc.

- 6.3.4 Diabetic Sock Club

- 6.3.5 Dr. Comfort, LLC

- 6.3.6 Drymax Technologies Inc.

- 6.3.7 Essity Aktiebolag

- 6.3.8 Jacob Rohner AG

- 6.3.9 Medicool, Inc.

- 6.3.10 Orthofeet, Inc.

- 6.3.11 PediFix

- 6.3.12 Rawganique

- 6.3.13 SIGVARIS GROUP

- 6.3.14 Simcan Enterprises Inc.

- 6.3.15 Siren Care, Inc.

- 6.3.16 Sweet Feet Diabetic Socks

- 6.3.17 THORLO, Inc.

- 6.3.18 Thuasne, LLC

- 6.3.19 TN SOCKS & TIGHTS LTD

- 6.3.20 Wigwam Mills, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment