PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065723

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065723

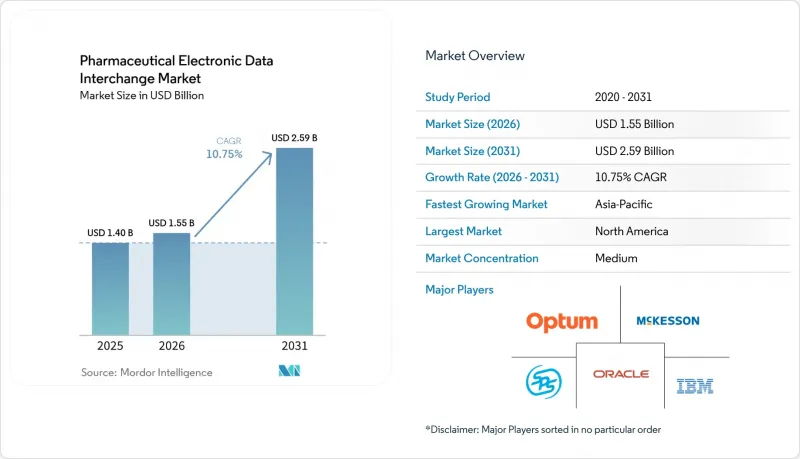

Pharmaceutical Electronic Data Interchange - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pharmaceutical electronic data interchange market size was valued at USD 1.40 billion in 2025 and is estimated to grow from USD 1.55 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 10.75% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions/Software, Services), Delivery Mode (On-Premises, Cloud, Direct, Mobile EDI), Transaction Type (Supply Chain, Pharmacy, Admin/Financial, Serialization and Traceability), End User (Manufacturers, CMOs/CDMOs, Distributors, Pharmacies, Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Pharmaceutical Electronic Data Interchange Market Trends and Insights

DSCSA EPCIS Repository Adoption: The Binding Near-Term Demand Catalyst

With DSCSA enforcement now active across the U.S. drug supply chain, full electronic traceability has become a critical driver in the pharmaceutical electronic data interchange market. The FDA's focus on interoperable, electronic package-level tracing eliminates reliance on manual workarounds. GS1 US is steering the market toward Release 1.3 adoption, with phased rollouts starting in 2026 for dispensers and extending to 2027 for manufacturers. This ensures ongoing activity in repository upgrades, partner onboarding, and conformance testing, driving recurring revenue from exception handling and message alignment.

NCPDP SCRIPT Upgrades Create a Locked-In Compliance Investment Window Through 2028

CMS has mandated NCPDP SCRIPT Standard Version 2023011 compliance for Medicare Part D e-prescribing by 2028, with additional standards due by 2027. ONC has aligned certification requirements with this timeline, pushing health IT developers to complete transitions by 2027. Surescripts has upgraded workflows and introduced a certification tester to assist trading partners. This creates a defined investment window for vendors, intermediaries, and platforms to update systems, while expanding the scope of real-time benefits and prior authorization data exchange.

Ransomware and HIPAA Enforcement Impose Measurable EDI Infrastructure Costs

Cybersecurity has become a significant expense for the pharmaceutical electronic data interchange market, as connected transaction environments are now integral to operations. An August 2025 ransomware attack on Inotiv disrupted internal business applications and data storage while compromising data of 9,542 individuals. This incident highlights the combined operational and legal risks. Additionally, HIPAA enforcement drives up costs for audits, contracts, and platform security, particularly impacting smaller entities that cannot distribute compliance expenses across large transaction volumes.

Other drivers and restraints analyzed in the detailed report include:

- HHS Claims Attachment Standards: A USD 781.98 Million Annual Efficiency Gain for EDI Adopters

- Cloud and Network-Based EDI Displaces Point-to-Point Architectures

- Legacy Multi-Standard Integration Suppresses Mid-Market Adoption Velocity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Solutions/Software accounted for 53.12% of the market, driven by translation software, serialization platforms, and pharmacy management tools. This base remains critical as large organizations rely on embedded enterprise systems for transaction processing. Services are projected to grow at a 10.95% CAGR from 2026 to 2031, highlighting the rising importance of compliance execution, testing, and managed operations over software.

Buyers are prioritizing services to address EPCIS 2.0 readiness, DSCSA conformance, and outsourced transaction management under tight deadlines. Mid-sized manufacturers and CDMOs, lacking internal resources, are key demand drivers, shifting the market toward recurring service revenue models.

On-Premises EDI held a 55.89% share in 2025, reflecting the established base of AS2, SFTP, and VAN-connected systems. These systems remain vital for high-volume distributors and manufacturers integrated with EDI, ERP, and warehouse workflows. Web- and Cloud-Based EDI is the fastest-growing segment, with an 11.15% CAGR from 2026 to 2031, driven by scalability and ease of updates.

Direct point-to-point EDI remains relevant for large trading pairs, while Mobile EDI serves niche use cases like last-mile ordering. Cloud deployment reduces infrastructure costs and accelerates updates, aligning with regulatory deadlines and easing partner onboarding.

Geography Analysis

In 2025, North America accounted for 40.76% of the pharmaceutical electronic data interchange market, securing the largest revenue share. The U.S. leads this growth due to regulatory initiatives like DSCSA, HIPAA claims attachments, and NCPDP SCRIPT upgrades, which drive investments in connectivity, testing, and workflow adjustments. Canada and Mexico contribute through import-driven trade and cross-border pharmaceutical distribution, increasing serialization and documentation complexity.

Asia-Pacific is projected to grow at a 12.25% CAGR from 2026 to 2031, making it the fastest-growing region in the pharmaceutical electronic data interchange market. Growth is driven by digitalization in pharmaceuticals across manufacturing, prescription workflows, and supply documentation, with China, India, Japan, Australia, and South Korea as key players. Japan's JD-NET system migration and initiatives like the May 2025 agreement between Shionogi, Astellas, and NTT DATA highlight compliance and platform-led growth in the region.

The Middle East and Africa region is growing steadily, led by GCC countries like Saudi Arabia and the UAE, with South Africa advancing in regulated pharmaceutical supply documentation. In South America, Brazil and Argentina drive growth through policy modernization supporting electronic prescribing and traceability. Smaller markets in MEA and South America remain in early adoption stages but offer long-term opportunities for vendors catering to localized standards and mid-market buyers.

- Athenahealth

- Availity, LLC

- Axway Software SA

- Boomi, LP

- Cleo Communications US, LLC

- Cognizant

- Comarch S.A.

- Edifecs, Inc.

- Experian Information Solutions, Inc.

- GE HealthCare Technologies Inc.

- Global Healthcare Exchange, LLC

- IBM

- Mckesson

- NextGen Healthcare

- NTT DATA Group Corporation

- OpenText

- Optum

- Oracle

- SPS Commerce, Inc.

- TrueCommerce, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Mandates for Standardized Healthcare Transactions

- 4.2.2 NCPDP SCRIPT and Pharmacy Workflow Upgrades

- 4.2.3 Cloud and API-Enabled EDI Modernization

- 4.2.4 Claims Attachments Digitization and Workflow Automation

- 4.2.5 DSCSA Serialized EPCIS Repository Adoption

- 4.2.6 Rebate and Chargeback Automation in Pharma Channels

- 4.3 Market Restraints

- 4.3.1 Cybersecurity and HIPAA/HITECH Exposure

- 4.3.2 Legacy-System Integration and Multi-Standard Mapping Complexity

- 4.3.3 EPCIS Interpretation Mismatches Across Trading Partners

- 4.3.4 Manual, Fax, Email, and Portal Persistence in Long-Tail Channels

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Solutions / Software

- 5.1.2 Services

- 5.2 By Delivery Mode

- 5.2.1 On-Premises

- 5.2.2 Web- and Cloud-Based EDI

- 5.2.3 Direct (Point-to-Point) EDI

- 5.2.4 Mobile EDI

- 5.3 By Transaction Type

- 5.3.1 Supply Chain Transactions

- 5.3.2 Pharmacy and Prescription Transactions

- 5.3.3 Administrative and Financial Transactions

- 5.3.4 Serialization and Traceability Data Exchange

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers and Biopharmaceutical Companies

- 5.4.2 CMOs and CDMOs

- 5.4.3 Wholesale Distributors and Specialty Distributors

- 5.4.4 Retail, Chain, Mail-Order, and Specialty Pharmacies

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 athenahealth, Inc.

- 6.3.2 Availity, LLC

- 6.3.3 Axway Software SA

- 6.3.4 Boomi, LP

- 6.3.5 Cleo Communications US, LLC

- 6.3.6 Cognizant Technology Solutions Corporation

- 6.3.7 Comarch S.A.

- 6.3.8 Edifecs, Inc.

- 6.3.9 Experian Information Solutions, Inc.

- 6.3.10 GE HealthCare Technologies Inc.

- 6.3.11 Global Healthcare Exchange, LLC

- 6.3.12 International Business Machines Corporation

- 6.3.13 McKesson Corporation

- 6.3.14 NextGen Healthcare, Inc.

- 6.3.15 NTT DATA Group Corporation

- 6.3.16 Open Text Corporation

- 6.3.17 Optum, Inc.

- 6.3.18 Oracle Corporation

- 6.3.19 SPS Commerce, Inc.

- 6.3.20 TrueCommerce, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment