PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065725

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065725

Mobile Card Reader - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

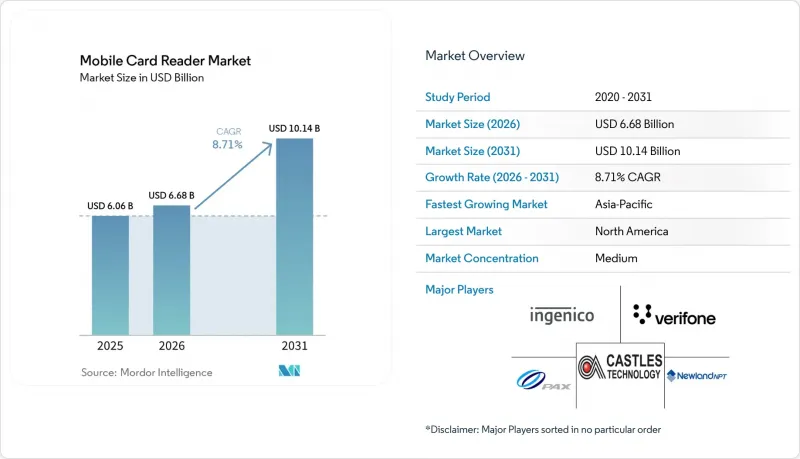

According to Mordor Intelligence, the mobile card reader market size is projected to expand from USD 6.06 billion in 2025 and USD 6.68 billion in 2026 to USD 10.14 billion by 2031, registering a CAGR of 8.71% between 2026 and 2031.

This report is Segmented by Component (Hardware, and Software and Services), Deployment (On-Premise, and Cloud), Technology (EMV Chip and PIN, Near-Field Communication and Contactless, and More), Application (Hospitality and Food Service, Transportation and Field Services, and More), End User (Micro-Merchants and Sole Traders, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Mobile Card Reader Market Trends and Insights

Rising Contactless And NFC Payment Acceptance

NFC and contactless technology accounted for a major portion of the technology segment in 2025, indicating that the mobile card reader market is now centered on tap-ready acceptance rather than optional contactless support. Merchants are no longer treating contactless as a feature upgrade because it now affects checkout speed, customer experience, and terminal relevance across daily retail activity. That shift has shortened the viable life of older devices, especially in developed markets where replacement timelines have moved from 5 years to less than 3 years. It has also driven demand toward smart mobile terminals and companion readers that support multiple payment modes on a single device. The same trend is reinforced by PCI MPoC standards, which are widening the range of compliant mobile acceptance options around NFC-capable devices and reader-linked phone deployments.

SME And Micro-Merchant Digitization

SMEs accounted for a large share of end-user demand in 2025, which makes small business digitization one of the clearest growth engines in the mobile card reader market. Merchant activation is expanding beyond traditional storefronts and into delivery, service, and market-trader use cases where portability matters more than full counter infrastructure. Government-led payment digitization programs in India, Indonesia, and Southeast Asia are supporting this shift by moving more small merchants into formal acceptance systems. Ant International's EPOS360 rollout shows how payment acceptance is now bundled with settlement, financing, and business management functions for smaller merchants, making the reader a gateway to a broader service stack. As a result, the mobile card reader market is seeing growth not only from hardware sales but also from merchant onboarding models that trade lower device pricing for longer-term transaction and software revenue.

Cybersecurity And Compliance Burden

Cybersecurity remains a major restraint because the mobile card reader market is moving deeper into open Android ecosystems and cloud-linked device fleets. The European Payments Council reported that financial service firms face cyberattack exposure far above most other sectors, which keeps payment infrastructure under sustained pressure to strengthen controls and monitoring. In April 2026, ESET Research disclosed a new NGate malware variant that abused a legitimate Android NFC payment application to relay card data and capture PINs, demonstrating how quickly the threat landscape is evolving around mobile acceptance tools. Smaller merchants are affected more sharply because they often lack dedicated security teams but still need to meet payment and data protection standards. This raises onboarding friction, increases support needs for providers, and limits how quickly some merchant groups can scale within the mobile card reader market.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel Retail And Tableside Checkout Expansion

- Cloud-Linked Value-Added POS Software Adoption

- Hardware Price Compression And Margin Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 67.93% of the mobile card reader market share in 2025, confirming that physical acceptance devices still anchor spending across the category. Companion card readers and smart mobile terminals remain the starting point for merchant activation because every card-accepting business needs certified hardware before it can begin processing. The hardware layer is also changing in the mobile card reader market, as integrated smart terminals are taking share from single-function dongles that depend on a host phone for broader tasks. Merchants increasingly prefer a single device that handles payment acceptance, barcode scanning, receipts, and broader store activities within a single workflow.

Software and services are projected to grow at a 9.11% CAGR through 2031, which shows where the revenue mix is moving next in the mobile card reader market. Payment software, terminal management, security tools, and merchant applications are becoming more important because they create recurring income after the device is installed. PAX said its PAXSTORE ecosystem now supports more than 110 million deployed terminals across 120 countries, which illustrates how app distribution and fleet management have become part of the core value proposition rather than an added layer. The mobile card reader industry is therefore shifting from hardware-led procurement toward platform-led relationships that last far beyond the initial terminal sale.

On-premises deployment accounted for 56.66% in 2025, indicating that a large installed base still prefers local control over payment environments. This is most visible in larger retail fleets and in regulated settings where network policies, audit demands, or system integration needs still favor a locally managed model. Many merchants also keep on-premises setups because existing infrastructure is embedded in daily operations and replacement can be disruptive. Even so, the mobile card reader market is steadily moving away from purely site-bound management as merchants expect faster updates and easier device oversight.

Cloud deployment is the fastest-growing segment of the mobile card reader market, advancing at a 9.03% CAGR through 2031. The appeal is practical because remote software updates, terminal monitoring, and multi-location visibility reduce operational friction for both vendors and merchants. Ingenico's 360 platform launch in February 2026 showed how providers are packaging device services, analytics, and transaction tools into a single cloud environment that can scale across regions. This leaves the mobile card reader industry with a clearer divide between vendors that can support managed fleets through the cloud and those that still depend mainly on hardware shipment volume.

Geography Analysis

North America accounted for 46.39% of the mobile card reader market in 2025, maintaining its lead. The United States remains the core revenue contributor because the card-based payment culture is strong and SME merchant density is high. The region also benefits from established card network infrastructure and from payment platforms that simplify onboarding for smaller merchants. These factors support recurring refresh demand as devices age and merchant expectations for software and contactless capabilities rise. South America remains smaller in absolute terms, but the mobile card reader market is gaining ground there as formal merchant payment infrastructure expands and digital acceptance becomes more important for underbanked merchant groups.

Europe held a significant share in 2025 and remains one of the most mature regions in the mobile card reader market. Demand is supported by NFC-readiness requirements, high smartphone use, and dense retail networks that sustain steady terminal demand. Germany offers a clear example of this shift, VR Payment reported that contactless girocard payments accounted for 88.5% of all girocard transactions in December 2025, and the active POS estate rose to more than 1.34 million terminals. The United Kingdom, France, Italy, and Spain also remain important because they combine large merchant bases with continued migration toward portable and smart payment devices. Europe, therefore, remains a key replacement and upgrade market rather than only a first-time deployment market.

Asia-Pacific is the fastest-growing regional segment in the mobile card reader market, with a 9.67% CAGR through 2031. Growth comes from merchant digitization programs, wider wallet use, tourism-linked payment acceptance, and the need for merchants to support multiple payment rails in the same environment. TNG Digital and EPOS launched EPOS360 and EPOS360 BlueTap in Malaysia in January 2026 to support local SMEs through the TNG eWallet ecosystem, which shows how payment providers are targeting this merchant base with integrated acceptance tools. The Middle East and Africa remain smaller contributors, but both are gaining relevance as cashless mandates, mobile payment infrastructure, and merchant formalization programs improve the long-term setup for the mobile card reader market.

- Ingenico Group S.A.

- VeriFone, Inc.

- PAX Technology Limited

- Castles Technology Co., Ltd.

- BBPOS Limited

- Miura Systems Ltd.

- MagTek, Inc.

- International Technologies and Systems Corporation

- Newland Payment Technology

- Shenzhen Sunmi Technology Co., Ltd.

- Urovo Technology Co., Ltd.

- Posiflex Technology, Inc.

- Dspread Technology (Beijing) Inc.

- DATECS LTD.

- Fujian Centerm Information Co., Ltd.

- Stripe, Inc.

- NEW POS TECHNOLOGY LIMITED

- SZZT Electronics Co., Ltd.

- Shanghai Smartpeak Intelligent Technology Co., Ltd.

- Dejavoo Systems, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Contactless and NFC Payment Acceptance

- 4.3.2 SME and Micro-Merchant Digitization

- 4.3.3 Omnichannel Retail and Tableside Checkout Expansion

- 4.3.4 Cloud-Linked Value-Added POS Software Adoption

- 4.3.5 PCI MPoC Certification Expanding Reader-Plus-Phone Deployments

- 4.3.6 Embedded Merchant Services Increasing Reader Attachment Rates

- 4.4 Market Restraints

- 4.4.1 Cybersecurity and Compliance Burden

- 4.4.2 Hardware Price Compression and Margin Pressure

- 4.4.3 Tap-to-Phone SoftPOS Cannibalization of Entry-Level Readers

- 4.4.4 Secure Element and Certification Bottlenecks

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Companion Card Readers

- 5.1.1.2 Smart Mobile Terminals

- 5.1.1.3 Reader Accessories and Docks

- 5.1.2 Software and Services

- 5.1.2.1 Payment Acceptance Software

- 5.1.2.2 Terminal Management and Security Software

- 5.1.2.3 Value-Added Merchant Applications

- 5.1.1 Hardware

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Technology

- 5.3.1 EMV Chip and PIN

- 5.3.2 Near-Field Communication and Contactless

- 5.3.3 Magnetic Stripe

- 5.3.4 Hybrid Multi-Interface Readers

- 5.4 By Application

- 5.4.1 Retail

- 5.4.2 Hospitality and Food Service

- 5.4.3 Transportation and Field Services

- 5.4.4 Healthcare

- 5.4.5 Entertainment and Events

- 5.5 By End User

- 5.5.1 Micro-Merchants and Sole Traders

- 5.5.2 Small and Medium-Sized Enterprises

- 5.5.3 Large Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ingenico Group S.A.

- 6.4.2 VeriFone, Inc.

- 6.4.3 PAX Technology Limited

- 6.4.4 Castles Technology Co., Ltd.

- 6.4.5 BBPOS Limited

- 6.4.6 Miura Systems Ltd.

- 6.4.7 MagTek, Inc.

- 6.4.8 International Technologies and Systems Corporation

- 6.4.9 Newland Payment Technology

- 6.4.10 Shenzhen Sunmi Technology Co., Ltd.

- 6.4.11 Urovo Technology Co., Ltd.

- 6.4.12 Posiflex Technology, Inc.

- 6.4.13 Dspread Technology (Beijing) Inc.

- 6.4.14 DATECS LTD.

- 6.4.15 Fujian Centerm Information Co., Ltd.

- 6.4.16 Stripe, Inc.

- 6.4.17 NEW POS TECHNOLOGY LIMITED

- 6.4.18 SZZT Electronics Co., Ltd.

- 6.4.19 Shanghai Smartpeak Intelligent Technology Co., Ltd.

- 6.4.20 Dejavoo Systems, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment