PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065735

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065735

Family Entertainment Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

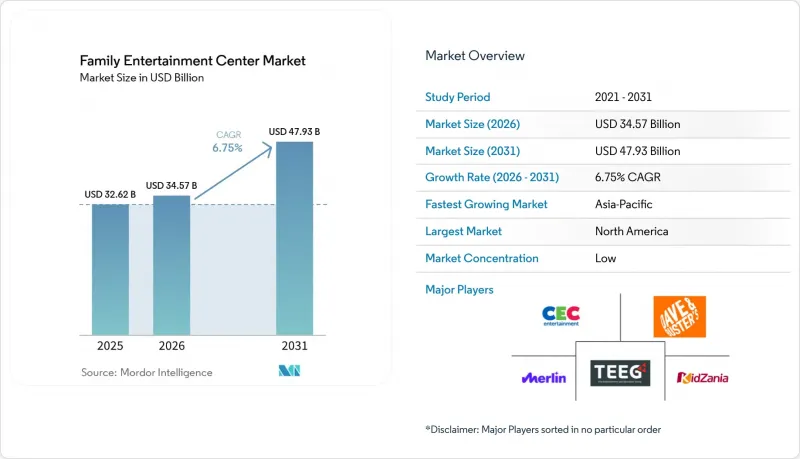

According to Mordor Intelligence, the global family entertainment center market was valued at USD 32.62 billion in 2025 and estimated to grow from USD 34.57 billion in 2026 to reach USD 47.93 billion by 2031, at a CAGR of 6.75% during the forecast period (2026-2031).

This report is Segmented by Type (CECs, Cedcs, Aecs, Lbecs), Activity Area (Physical Play, AR/VR Gaming, Skill Games), Facility Size (<=5K Sq. Ft., 5K-40K Sq. Ft., 1-10 Acres, & More), Visitor Demographics (Families 0-8, 9-12, Teens, Young Adults, Adults), Revenue Source (Entry Fees, F&B, Merchandising, Advertising, Other), and Geography (NA, SA, Europe, APAC, MEA). Forecasts in Value (USD).

Global Family Entertainment Center Market Trends and Insights

Experience-led Family and Group Leisure Demand

Consumer preferences are shifting toward shared and participatory leisure, driving consistent demand for family entertainment centers (FECs) across various economies. Economic impact studies highlight the significant role of FECs within organized leisure, with attendance figures reflecting their growing popularity. These centers benefit from group outings, as families often engage with multiple venue sections during a single visit. This dynamic increases overall spending on entry, gaming, food, and events, making such visits more valuable than single-attraction outings. The FEC market continues to thrive on repeat visits tied to weekends, school breaks, and celebrations, rather than relying solely on one-time discretionary spending.

AR/VR-Enabled Attraction Refresh

AR and VR have transitioned from being mere novelties to essential tools, sparking renewed investment interest in the family entertainment center market. In March 2026, Sandbox VR announced USD 300 million in lifetime ticket sales from over 80 venues worldwide. The company highlighted that a single content release raked in over USD 50 million, underscoring the lucrative potential of immersive attractions, even within a limited space. Furthermore, the release revealed that nearly one-third of patrons are repeat visitors. This statistic emphasizes the importance of content refreshes in driving not just initial visits but also return traffic. For operators, this insight suggests a shift: older physical attractions can now be either replaced or enhanced with modular immersive zones, continually updated through software and content cycles. This evolution leads to a more adaptable capital expenditure profile for the family entertainment center market. This is particularly crucial in urban areas, where operators seek maximum returns from constrained floor spaces.

High Upfront Capex and Maintenance Burden

High initial investment poses a significant challenge for operators in the family entertainment center market, particularly those developing full-service venues with active play, gaming, and food services. Establishing a mixed-format venue requires substantial upfront costs, excluding ongoing maintenance expenses. Tariffs have increased construction and equipment capital expenditure over a two-year period, complicating earlier project assumptions while operators attempt to maintain stable admission prices. Independent operators face greater difficulties due to limited procurement scale and financial flexibility compared to larger chains. Consequently, the market is expected to adopt stricter expansion strategies, prioritize selective new builds, and show increased interest in acquiring operators with established sites and proven local demand.

Other drivers and restraints analyzed in the detailed report include:

- Urban Spending and Weather-proof Indoor Entertainment Demand

- Multi-activity Social Venues Widening Audience Mix

- Competition from Home Digital Entertainment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Children's Entertainment Centers accounted for 35.83% of the family entertainment center market share in 2025, highlighting their role in driving global revenues. Their success is linked to demand for birthday celebrations, family outings, and repeat weekend activities for younger children. Operators effectively package food, redemption, and events to attract early-age visitors. However, older children and mixed-age groups now seek diverse experiences, gradually reducing the dominance of child-focused centers in the market.

Location-based VR Entertainment Centers are projected to grow at a 7.80% CAGR from 2026 to 2031, driven by faster content updates, novelty, and compact formats suited for urban areas. Sandbox VR, with over 80 global venues and USD 300 million in lifetime ticket sales as of March 2026, demonstrates the scalability of immersive formats with effective content and customer management. In February 2026, The LEGO Group acquired 29 LEGO Discovery Centre and LEGOLAND Discovery Centre sites from Merlin Entertainments, signaling a shift toward greater operational control over branded experiences. This trend reflects increasing competition between edutainment and immersive concepts for family engagement. The industry is moving toward formats prioritizing intellectual property, content refresh rates, and ownership over brand legacy.

Skill and Competition Games contributed 40.21% of revenue in 2025, making them the largest activity-area category in the family entertainment center market. Their broad appeal spans children, teenagers, young adults, and corporate groups. Activities such as bowling, laser tag, karting, and mini-golf drive engagement through organized bookings, league-style participation, and repeat challenges, optimizing weekly utilization. Arcade and redemption areas generate direct revenue and encourage repeat visits through merchandise sales. Physical play areas remain relevant but are increasingly integrated into broader venue layouts instead of standalone concepts.

AR and VR Gaming Zones are projected to grow at an 8.17% CAGR through 2031, emerging as the fastest-growing activity area in the family entertainment center market. This growth is driven by improved hardware affordability, expanded content libraries, and the appeal of immersive group experiences. Sandbox VR's performance demonstrates consumer interest in regularly updated immersive sessions. For multi-activity operators, XR zones act as both an attraction and a feature that boosts interest across the venue. The market is increasingly divided between activity categories that benefit from content updates and those reliant on fixed mechanical setups.

Geography Analysis

North America accounted for 34.47% of the family entertainment center market share in 2025, making it the largest regional contributor to global revenue. The region benefits from established operators, consumer familiarity with organized indoor leisure, and a mature franchise ecosystem. Large companies better absorb insurance, labor, and equipment costs than smaller competitors. Dave & Buster's reported FY2025 revenue of USD 2.1 billion across 243 venues and announced international franchise agreements for over 35 locations, with FY2026 openings planned in Delhi, Perth, and Mexico City. This scale highlights North America's central role in the market, despite emerging growth opportunities elsewhere.

Asia-Pacific is projected to grow at an 8.36% CAGR through 2031, driven by urbanization, middle-class spending growth, and the spread of organized entertainment formats across China, India, South Korea, and Southeast Asia. The region is witnessing increased adoption of media intellectual property in physical entertainment, along with expansion of branded indoor experiences across multiple countries. Asia-Pacific offers high growth potential and opportunities for localized concepts tailored to language, content, and spending behaviors.

Europe remains a key demand center due to high spending per visit, stable mall traffic, and interest in competitive-socializing formats. The Middle East and Africa, though smaller, attract significant investment in large-format destinations. Recent expansions in the Gulf reflect growing leisure capacity, while global manufacturers increasingly view the region as a strong growth market. This positions Europe as a stable market and Middle East and Africa as a strategic expansion area.

- CEC Entertainment

- Dave & Buster's Entertainment

- TEEG

- KidZania

- Merlin Entertainments

- Round1 Entertainment

- Cinergy Entertainment Group

- Scene75 Entertainment Centers

- Urban Air Adventure Park

- Lucky Strike Entertainment

- Andretti Indoor Karting and Games

- Apex Entertainment

- iPlay America

- Bandai Namco Amusement

- Hollywood Bowl Group

- Majid Al Futtaim Entertainment

- SMAAASH

- Landmark Group / Fun City

- Funriders Leisure & Amusement

- Tenpin

- Sky Zone

- Malibu Jack's

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Experience-led family and group leisure demand

- 4.2.2 AR/VR-enabled attraction refresh

- 4.2.3 Urban spending and weather-proof indoor entertainment demand

- 4.2.4 Multi-activity social venues widening audience mix

- 4.2.5 Mall-space repurposing into experiential anchors

- 4.2.6 Birthday, school, and corporate event monetization

- 4.3 Market Restraints

- 4.3.1 High upfront capex and maintenance burden

- 4.3.2 Competition from home digital entertainment

- 4.3.3 Liability insurance inflation for active-play formats

- 4.3.4 Tariffs and FX pressure on imported amusement hardware

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Children's Entertainment Centers (CECs)

- 5.1.2 Children's Edutainment Centers (CEDCs)

- 5.1.3 Adult Entertainment Centers (AECs)

- 5.1.4 Location-based VR Entertainment Centers (LBECs)

- 5.2 By Activity Area

- 5.2.1 Physical Play Activities

- 5.2.1.1 Trampoline and Ninja Courses

- 5.2.1.2 Soft Play and Climbing Areas

- 5.2.1.3 Indoor Playgrounds

- 5.2.2 Arcade Studios (Video Games,Redemption Games)

- 5.2.3 AR and VR Gaming Zones (VR Arenas and Simulators, AR and Mixed-Reality Attractions)

- 5.2.4 Skill and Competition Games (Bowling,Laser Tag,Go-Karts,Mini Golf etc.)

- 5.2.1 Physical Play Activities

- 5.3 By Facility Size

- 5.3.1 Up to 5,000 Sq. Ft.

- 5.3.2 5,001 to 20,000 Sq. Ft.

- 5.3.3 20,001 to 40,000 Sq. Ft.

- 5.3.4 1 to 10 Acres

- 5.3.5 Over 10 Acres

- 5.4 By Visitor Demographics

- 5.4.1 Families with Children (0-8)

- 5.4.2 Families with Children (9-12)

- 5.4.3 Teenagers (13-19)

- 5.4.4 Young Adults (20-25)

- 5.4.5 Adults (Ages 25+)

- 5.5 By Revenue Source

- 5.5.1 Entry Fees and Ticket Sales

- 5.5.2 Food and Beverages

- 5.5.3 Merchandising and Redemption

- 5.5.4 Advertising and Sponsorship

- 5.5.5 Other Ancillary Revenue

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 CEC Entertainment

- 6.4.2 Dave & Buster's Entertainment

- 6.4.3 TEEG

- 6.4.4 KidZania

- 6.4.5 Merlin Entertainments

- 6.4.6 Round1 Entertainment

- 6.4.7 Cinergy Entertainment Group

- 6.4.8 Scene75 Entertainment Centers

- 6.4.9 Urban Air Adventure Park

- 6.4.10 Lucky Strike Entertainment

- 6.4.11 Andretti Indoor Karting and Games

- 6.4.12 Apex Entertainment

- 6.4.13 iPlay America

- 6.4.14 Bandai Namco Amusement

- 6.4.15 Hollywood Bowl Group

- 6.4.16 Majid Al Futtaim Entertainment

- 6.4.17 SMAAASH

- 6.4.18 Landmark Group / Fun City

- 6.4.19 Funriders Leisure & Amusement

- 6.4.20 Tenpin

- 6.4.21 Sky Zone

- 6.4.22 Malibu Jack's

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment