PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065737

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065737

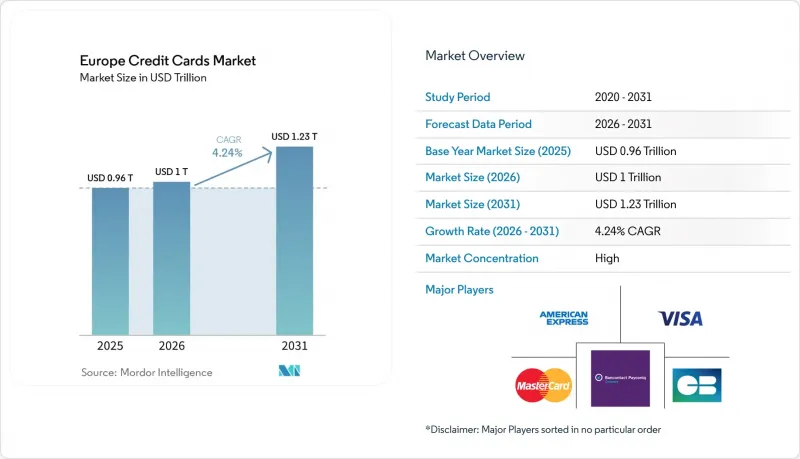

Europe Credit Cards - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe credit cards market size is projected to be USD 0.96 trillion in 2025, USD 1 trillion in 2026, and reach USD 1.23 trillion by 2031, growing at a CAGR of 4.24% from 2026 to 2031.

This report is Segmented by Application (Food & Groceries, Health & Pharmacy, Restaurants & Bars, and More), Card Type (General Purpose Credit Cards, Specialty & Other Credit Cards), Card Format (Physical, Digital), Provider (Visa, Mastercard, Other Providers), and Geography (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Credit Cards Market Trends and Insights

Cash-to-Cashless Shift & Contactless Adoption Surge

Cash use keeps shrinking in daily transactions as digital payments normalize across Europe, with adoption gaps by subregion creating uneven but durable growth vectors for the European credit card market. Northern and Western Europe show the highest digital shopping participation among adults, while Eastern and Southern Europe lag and provide scope for catch-up as acceptance and consumer familiarity improve. Contactless use and card preference remain strong, with consumers citing convenience and speed, and merchants signaling alignment with card acceptance as a default for retail environments, which supports continued card volume growth in mixed-payment settings. Tokenization and streamlined checkout continue to scale, with Mastercard reporting nearly half of European e-commerce transactions tokenized and Click to Pay enrollment more than doubling across 26 markets, which helps secure card credentials in wallets and protects approval rates . Consumer recognition of card security and merchant preference for cards add reinforcement, with both groups trusting card rails for domestic and cross-border transactions over the alternatives. Together, these factors underpin a steady migration from cash and help core issuers capture consistent growth in the European credit card market.

Post-COVID Rebound in Cross-Border Travel Spend

Recovered tourism and corporate travel lift high-yield card spend, which supports premium issuance and category-specific co-brand programs that reinforce the European credit card market. European travel demand remained firm as spending outpaced arrivals in 2025, which boosts transaction values in travel, hospitality, and transportation categories tied to cardholder rewards and insurance features. Business travel is projected to reach USD 458.64 (EUR 389.90 billion) in 2026, which signals healthy corporate activity and supports the issuance of cards with enhanced controls, reporting, and insurance bundles used by enterprise and SME segments . Co-branded travel products are evolving around cross-border needs, highlighted by the European Travel Commission-Mastercard-ICBC card that targets Chinese visitors and links acceptance, destination support, and cultural elements into one credential. This rebound adds momentum to the European credit card market as issuers match travel-linked benefits with revived cross-border volumes and diversify revenue beyond interchange by monetizing insurance and FX. The travel-led mix shift favors premium portfolios that can maintain loyalty and keep spend engaged across borders, which steadies growth through the cycle for the European credit card market.

Interchange-Fee Caps & Stricter EU Regulations

Capped interchange for consumer credit at 0.30% across the EU compresses issuer economics and shifts growth focus toward value-added services, commercial card issuance, and product differentiation that reduces churn in the European credit card market. EU-level audits describe progress in digital payments and the influence of regulation on pricing, innovation, and market structure, which guides how issuers invest in fraud controls and authentication to protect approval rates. Industry associations emphasize the role of interchange in funding network security and innovation, a view that underscores how caps reroute business models toward services and subscriptions. In the United Kingdom, regulators scrutinize post-Brexit cross-border card-not-present pricing, and industry participants track proposals to align fees with pre-Brexit benchmarks for online transactions between the United Kingdom and the EEA. Issuers balance these constraints by investing in tokenization, passkeys, and risk systems that help defend approval performance and transaction margins in the European credit card market.

Other drivers and restraints analyzed in the detailed report include:

- PSD2-Enabled Fintech Credit Expansion

- Embedded-Finance & Co-Branded Card Proliferation

- Instant-Payment & Wallet Substitution Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food & Groceries held 26.83% of the 2025 value, which reflects the category's essential nature and broad in-store acceptance, while e-commerce groceries expand click-and-collect and delivery payments that reinforce card usage patterns. Travel & Tourism is set to be the fastest-growing, supported by revived international arrivals and spending, as well as a healthy business travel outlook that sustains premium features and category-specific rewards. The European credit card market benefits from the return of cross-border flows and the mix shift toward transportation, dining, and entertainment spend that spreads card activity across multiple travel-linked merchant categories. Online media, consumer electronics, and restaurants keep stable shares as households embed repeat digital purchases and on-premises spending supported by cards and tokenized credentials that improve approval rates and fraud control. With cards anchoring 40% of e-commerce and 63% of in-store transactions by value in 2022, issuers are positioned to grow with the breadth of everyday payments that define the European credit card market.

The European credit card market size for Travel & Tourism is projected to expand at a 4.83% CAGR by 2031, and this is reinforced by premium card benefits that match evolving traveler needs in insurance, lounge access, and flexible redemptions. Business travel recovery into 2026 supports corporate card demand, expense tools, and stronger underwriting supported by real-time controls and data-rich reporting, which deepens issuer ties with enterprises and SMEs. Co-brand partnerships continue to surface in travel corridors that combine destination networks, acceptance reach, and multilingual service layers for visitors, as seen in the European Travel Commission-Mastercard-ICBC card. E-commerce-linked applications stay resilient as tokenization and passkeys reduce checkout friction and sustain card-on-file relationships within subscription and content ecosystems. Overall, application diversity and strong acceptance underpin persistent activity in the European credit card market across everyday and discretionary categories.

General-purpose Credit Cards accounted for 91.14% of the 2025 value, which reflects the breadth of bank issuance and the reach of global acceptance that secures cross-border transactions and standard rewards frameworks. Specialty & Other Credit Cards are projected to grow faster at a 5.12% CAGR through 2031, as issuers extend co-brands and embedded finance credentials into vertical software platforms and affinity communities that prize tailored benefits and controls. Mastercard's expansion of tokenization, Click to Pay, and passkeys across Europe enables both general-purpose and specialty portfolios to improve security and conversion in digital journeys for the European credit card market. Enterprise and SME spending needs are attracting more attention in specialty programs built with commercial features, usage restrictions, and automated reporting, which match stricter budgeting and compliance standards. Personalization trends across card form factors, materials, and packaging continue to lift acquisition and spend per user, which supports growth in both mainstream and niche portfolios of the European credit card market.

The European credit card market benefits from specialty programs that target travel, mobility, and benefits use cases, because these products monetize beyond interchange through insurance, FX, and subscription fees. European travel-focused co-brands that link destination support with multilingual service suggest new paths for targeting international visitor segments, which adds volume and retention for issuers running dual portfolios. Visa's partnerships with major European banks also reinforce general-purpose issuance and control more end-customer journeys as debit, credit, and co-brands align under a common acceptance umbrella. As issuers expand capabilities through network and processor relationships, specialty cards can justify premium pricing, while general-purpose cards remain the gateway for broad consumer coverage across the European credit card market. This twin-track approach defends share while enabling targeted growth in high-yield verticals that prize tailored features and flexible integrations. Over the forecast period, general-purpose incumbency is likely to hold, while specialty expansion outpaces in growth terms based on use-case depth and monetization options.

List of Companies Covered in this Report:

- Visa Inc.

- Mastercard Inc.

- American Express Co.

- Revolut Ltd

- Klarna Bank AB

- Cartes Bancaires CB

- Bancontact Payconiq Co.

- Barclays plc

- HSBC Holdings plc

- NatWest Group plc

- Lloyds Banking Group plc

- Deutsche Bank AG

- Commerzbank AG

- BNP Paribas SA

- Credit Agricole SA

- Societe Generale SA

- Banco Santander SA

- CaixaBank SA

- ING Group NV

- Intesa Sanpaolo SpA

- UniCredit SpA

- Nordea Bank Abp

- Danske Bank A/S

- Swedbank AB

- Adyen NV

- Stripe Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cash-to-Cashless Shift & Contactless Adoption Surge

- 4.2.2 Explosive E-commerce Growth Across EU

- 4.2.3 Post-COVID Rebound in Cross-Border Travel Spend

- 4.2.4 PSD2-Enabled Fintech Credit Expansion

- 4.2.5 Embedded-Finance & Co-Branded Card Proliferation

- 4.2.6 BNPL-Credit Card Hybrids Driving New Issuance

- 4.3 Market Restraints

- 4.3.1 Interchange-Fee Caps & Stricter EU Regulations

- 4.3.2 Inflation-Driven Consumer Caution on Revolving Debt

- 4.3.3 Instant-Payment & Wallet Substitution Risk

- 4.3.4 ESG-Led Tightening of Consumer-Credit Rules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Food & Groceries

- 5.1.2 Health & Pharmacy

- 5.1.3 Restaurants & Bars

- 5.1.4 Consumer Electronics

- 5.1.5 Media & Entertainment

- 5.1.6 Travel & Tourism

- 5.1.7 Other Applications

- 5.2 By Card Type

- 5.2.1 General Purpose Credit Cards

- 5.2.2 Specialty & Other Credit Cards

- 5.3 By Card Format

- 5.3.1 Physical

- 5.3.2 Digital

- 5.4 By Provider

- 5.4.1 Visa

- 5.4.2 Mastercard

- 5.4.3 Other Providers

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 BENELUX

- 5.5.7 NORDICS

- 5.5.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Visa Inc.

- 6.4.2 Mastercard Inc.

- 6.4.3 American Express Co.

- 6.4.4 Revolut Ltd

- 6.4.5 Klarna Bank AB

- 6.4.6 Cartes Bancaires CB

- 6.4.7 Bancontact Payconiq Co.

- 6.4.8 Barclays plc

- 6.4.9 HSBC Holdings plc

- 6.4.10 NatWest Group plc

- 6.4.11 Lloyds Banking Group plc

- 6.4.12 Deutsche Bank AG

- 6.4.13 Commerzbank AG

- 6.4.14 BNP Paribas SA

- 6.4.15 Credit Agricole SA

- 6.4.16 Societe Generale SA

- 6.4.17 Banco Santander SA

- 6.4.18 CaixaBank SA

- 6.4.19 ING Group NV

- 6.4.20 Intesa Sanpaolo SpA

- 6.4.21 UniCredit SpA

- 6.4.22 Nordea Bank Abp

- 6.4.23 Danske Bank A/S

- 6.4.24 Swedbank AB

- 6.4.25 Adyen NV

- 6.4.26 Stripe Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment