PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065741

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065741

Video Streaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

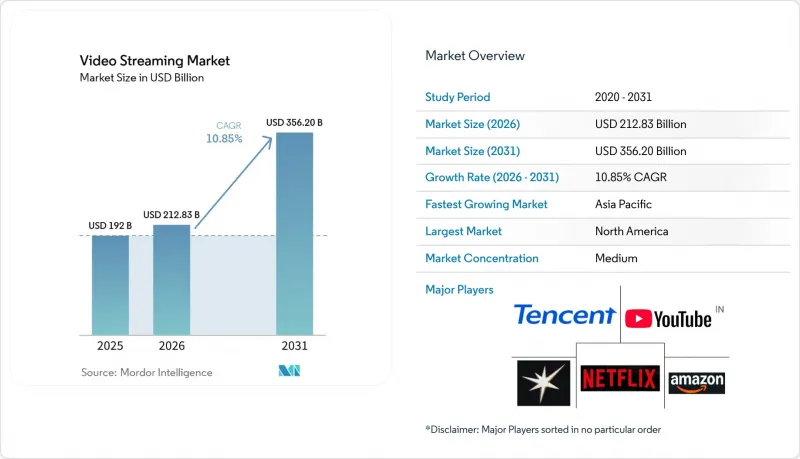

According to Mordor Intelligence, video streaming market size in 2026 is estimated at USD 212.83 billion, growing from 2025 value of USD 192.0 billion with 2031 projections showing USD 356.2 billion, growing at 10.85% CAGR over 2026-2031.

This report is Segmented by Streaming Type (Live Video Streaming, Non-Linear / VOD Streaming), Component (Software, Services), Solutions (Over-The-Top, Internet Protocol TV, and More), Platform (Smartphones and Tablets, Smart TV, Laptops and Desktops, and More), Revenue Model (Subscription, Advertising, Rental / Transactional), Deployment Type (Cloud, On-Premises), End User (Consumer, Enterprise), and Geography.

Global Video Streaming Market Trends and Insights

Growing Availability of High-Speed Internet Connectivity

The rollout of fiber and 5G radically raised the ceiling for bit-rate-intensive services and set a stronger baseline for the video streaming market. By 2025 more than 2.8 billion 5G subscriptions were in service, and fixed-wireless access added several hundred thousand households each quarter in the United States . Operators in India and Indonesia introduced low-cost 5G data packs that prioritized major streaming apps, pulling first-time viewers directly into premium content ecosystems. In parallel, campus-wide Wi-Fi 6 upgrades in Latin America lifted sustained 4 K throughput, enabling local broadcasters to launch companion streaming services that met studio security requirements. Cloud platforms recorded double-digit traffic spikes with every regional speed upgrade, confirming that bandwidth remains the primary flywheel for subscription and advertising revenue expansion.

Rising Popularity of Live Sports and Event Streaming

Live sports migrated quickly from cable to online in 2025 as top leagues sold digital-first packages. A Hub study showed that 69% of fans viewed matches on streaming services, edging out linear broadcast for the first time. Rights deals with the NFL, NBA, La Liga, and IPL translated into nightly surges in concurrent streams, pressuring networks to refine low-latency paths and real-time ad stitching. Younger viewers under 35 drove nearly half of all new sports subscriptions, validating aggressive bids by platforms that pair live feeds with interactive stats overlays. Advertisers followed, shifting brand budgets toward mid-roll and dynamic banner formats embedded in live streams, thus boosting CPMs relative to general entertainment content.

Content Piracy and Unauthorized Distribution

Illicit restreaming siphoned revenue even as enforcement improved. The Asia Video Industry Report for 2024 documented new blocking statutes in India, Malaysia, and Vietnam that targeted pirate IPTV boxes. Sports pay-per-view content remained the most pirated category, prompting rightsholders to embed forensic watermarking that traces each account. While technical counter-measures reduced casual piracy, the perpetual game of domain takedown versus mirror site re-appearance meant that smaller services without robust legal teams continued to lose prospective subscribers, cutting into the aggregate video streaming market growth potential.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Smart-TVs and Connected OTT Devices

- AI-Driven Localized Dubbing Unlocking Non-English Audiences

- Escalating Content Licensing and Production Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Live streaming posted the fastest trajectory, rising at a 14.4% CAGR from 2026 to 2031 as leagues and concert promoters chose direct distribution. The video streaming market size for live formats stood at USD 74420.6 million in 2025 and is expected to surpass USD 169.3 billion by 2031, indicating a dramatic scaling curve. Non-linear/VOD retained dominance due to its 61.25% share in 2025, backed by expansive libraries and robust recommendation engines that propelled over 80% of total plays on major services.

Live sports coverage turned streaming platforms into primary destinations during key tournaments, narrowing the perception gap between cable reliability and online flexibility. Real-time engagement tools such as alternate commentary tracks and in-app merch links unlocked fresh revenue streams and extended session duration. Meanwhile, on-demand services continued to refine compression and pre-fetching strategies that balanced cost efficiency with sharper picture quality, reinforcing their foundational role inside the broader video streaming market.

Software components-players, CMS, analytics layers-accounted for 59.15% of 2025 revenue. However, managed services such as multi-CDN orchestration and server-side ad insertion registered a 16.1% CAGR forecast as publishers outsourced highly specialized delivery tasks. Edge-aware traffic steering ensured low latency during peak global events, which safeguarded the video streaming market size advantages secured by early software adoption.

The surge in services aligned with ad-supported tier expansion because SSAI blended personalized ads into live streams without overt buffering. Providers like Akamai handled traffic bursts that peaked at more than 200 Tbps in 2024, demonstrating infrastructure reliance on third-party expertise. As compliance and accessibility rules tightened, turnkey captioning and DRM services attracted mid-tier platforms keen to manage risk while staying focused on storytelling.

OTT retained a 56.20% grip on revenue in 2025 thanks to its device-agnostic reach and direct billing. Continuous feature rollouts-from personalized profiles to watch-party modes-raised stickiness among households already juggling multiple subscriptions. IPTV rebounded with a 13.1% CAGR after telcos refreshed fiber-to-the-home bundles that guaranteed symmetric bandwidth and bundled local language packs, thereby adding stability to the evolving video streaming market.

Hybrid business models emerged as operators integrated OTT apps into set-top boxes, ensuring single-remote access that appealed to less tech-savvy viewers. Advanced multicast pushed ultra-HD linear channels efficiently, and AI-enhanced EPGs exposed hidden catalog gems. Cable and satellite incumbents leveraged existing sports contracts to package optional 4K streams, delaying but not preventing a long-term share drift toward full IP delivery.

Geography Analysis

North America held 41.85% of global revenue in 2025 as ubiquitous broadband, aggressive original content budgets, and early adoption of advertising hybrids converged. The United States alone is projected to lift streaming revenue from USD 112 billion in 2024 to USD 140 billion by 2029, reinforcing its anchor role in the video streaming market. Competitive churn remained high because households stacked an average of five paid services, prompting platforms to rotate discount bundles and theater-to-stream windows to keep churn below 3% monthly. Canada mirrored these patterns, although regional broadcasters preserved local sports rights that sheltered nationalist viewer preferences.

Asia-Pacific delivered the fastest regional CAGR at 16.8% and is forecast to add USD 16.2 billion in incremental revenue by 2029. India contributed more than one-quarter of the uplift, fueled by discounted mobile data plans and exclusive cricket streaming, while China leaned on state-owned telcos to accelerate FTTH. Japan blended anime with high-budget serials to maintain ARPU leadership. Local platforms such as JioCinema forged low-price tiers paired with daily payment options, a model now copied in Southeast Asia. The video streaming market size gained additional momentum from user generated short-form clips that acted as funnels into premium long-form libraries.

Europe retained solid traction, and the United Kingdom is set to become the continent's largest entertainment market by 2027 as ad-supported tiers find an addressable audience in cost-sensitive households. Thirty-three percent of new UK sign-ups in Q1 2025 selected an ad tier, and Prime Video captured 17% of those activations. Markets such as Germany tightened CO2 disclosure rules for datacenters, prompting greener codec strategies, while France advanced local content quotas that shaped catalog acquisition plans.

Latin America and the Middle East and Africa registered lower absolute revenue but posted healthy double-digit user growth as smart-phone penetration and mobile broadband upgrades reached critical mass. SVOD growth encouraged Wi-Fi 6 adoption across the region, which in turn improved average streaming bit-rates. Nigeria's telcos trialed zero-rated educational channels that steered incremental demand toward commercial entertainment, illustrating mutual benefits between operators and OTT providers in the continually widening video streaming market.

- Netflix Inc.

- Amazon.com Inc. (Prime Video)

- Alphabet Inc. (YouTube)

- The Walt Disney Company (Disney+, Hulu)

- Warner Bros. Discovery Inc. (Max)

- Tencent Holdings Ltd. (Tencent Video)

- Apple Inc. (Apple TV+)

- JioCinema

- Crunchyroll LLC

- Akamai Technologies Inc.

- iQIYI Inc.

- DAZN Group

- fuboTV Inc.

- Kaltura Inc.

- Vimeo Inc.

- Disney+ Hotstar

- iQIYI Inc.

- Bilibili Inc.

- PCCW Media (Viu)

- Rakuten Group Inc. (Rakuten Viki)

- Reliance Industries Ltd. (JioCinema)

- Zee Entertainment Enterprises Ltd. (ZEE5)

- Sky Group Ltd. (NOW)

- Telefonica S.A. (Movistar+)

- Dish Network Corp. (Sling TV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing availability of high-speed internet connectivity

- 4.2.2 Rising popularity of live sports and event streaming

- 4.2.3 Proliferation of smart-TVs and connected OTT devices

- 4.2.4 AI-driven localized dubbing unlocking non-English audiences

- 4.2.5 Telco zero-rating of OTT data in emerging markets

- 4.2.6 5G multicast/broadcast (eMBMS) for in-stadium live feeds

- 4.3 Market Restraints

- 4.3.1 Content piracy and unauthorized distribution

- 4.3.2 Escalating content licensing and production costs

- 4.3.3 Carbon-footprint scrutiny of streaming delivery

- 4.3.4 Codec-standard fragmentation causing device issues

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Assessment of the Impact of Macroeconomic factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Streaming Type

- 5.1.1 Live Video Streaming

- 5.1.2 Non-Linear / VOD Streaming

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Solutions

- 5.3.1 Over-the-Top (OTT)

- 5.3.2 Internet Protocol TV (IPTV)

- 5.3.3 Cable TV

- 5.3.4 Pay-TV

- 5.4 By Platform

- 5.4.1 Smartphones and Tablets

- 5.4.2 Smart TV

- 5.4.3 Laptops and Desktops

- 5.4.4 Gaming Consoles

- 5.5 By Revenue Model

- 5.5.1 Subscription (SVOD)

- 5.5.2 Advertising (AVOD/FAST)

- 5.5.3 Rental / Transactional (TVOD)

- 5.6 By Deployment Type

- 5.6.1 Cloud

- 5.6.2 On-Premises

- 5.7 By End User

- 5.7.1 Consumer

- 5.7.2 Enterprise

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 United Kingdom

- 5.8.3.2 Germany

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 India

- 5.8.4.3 Japan

- 5.8.4.4 South Korea

- 5.8.4.5 Australia and New Zealand

- 5.8.4.6 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 GCC Countries (Saudi Arabia, UAE, Qatar)

- 5.8.5.1.2 Turkey

- 5.8.5.1.3 Rest of Middle East

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Nigeria

- 5.8.5.2.3 Rest of Africa

- 5.8.5.1 Middle East

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Netflix Inc.

- 6.4.2 Amazon.com Inc. (Prime Video)

- 6.4.3 Alphabet Inc. (YouTube)

- 6.4.4 The Walt Disney Company (Disney+, Hulu)

- 6.4.5 Warner Bros. Discovery Inc. (Max)

- 6.4.6 Tencent Holdings Ltd. (Tencent Video)

- 6.4.7 Apple Inc. (Apple TV+)

- 6.4.8 JioCinema

- 6.4.9 Crunchyroll LLC

- 6.4.10 Akamai Technologies Inc.

- 6.4.11 iQIYI Inc.

- 6.4.12 DAZN Group

- 6.4.13 fuboTV Inc.

- 6.4.14 Kaltura Inc.

- 6.4.15 Vimeo Inc.

- 6.4.16 Disney+ Hotstar

- 6.4.17 iQIYI Inc.

- 6.4.18 Bilibili Inc.

- 6.4.19 PCCW Media (Viu)

- 6.4.20 Rakuten Group Inc. (Rakuten Viki)

- 6.4.21 Reliance Industries Ltd. (JioCinema)

- 6.4.22 Zee Entertainment Enterprises Ltd. (ZEE5)

- 6.4.23 Sky Group Ltd. (NOW)

- 6.4.24 Telefonica S.A. (Movistar+)

- 6.4.25 Dish Network Corp. (Sling TV)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment