PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065749

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065749

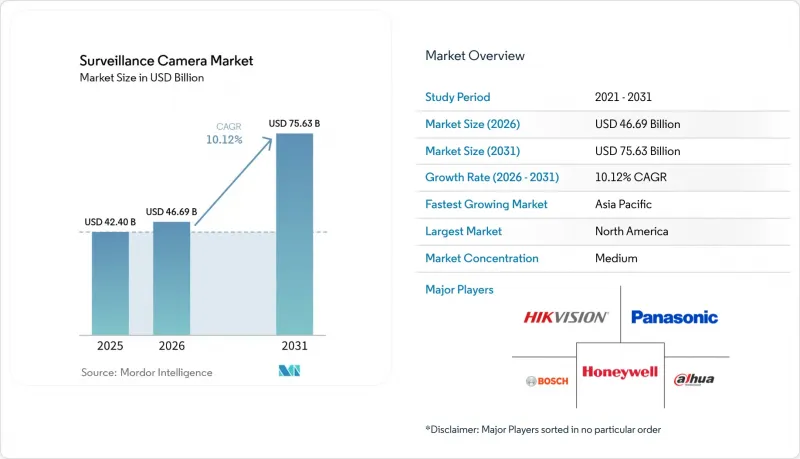

Surveillance Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, surveillance camera market size in 2026 is estimated at USD 46.69 billion, growing from 2025 value of USD 42.40 billion with 2031 projections showing USD 75.63 billion, growing at 10.12% CAGR over 2026-2031.

This report is Segmented by Technology (Analog Cameras, IP Cameras, and More), Form Factor (Dome Cameras, Bullet Cameras, and More), Resolution (Non-HD, HD, and More), Connectivity (Wired, Power-Over-Ethernet, and More), Deployment Model (On-Premise, and More), End-User Industry (BFSI, Transportation and Infrastructure, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Surveillance Camera Market Trends and Insights

5G-edge networks unlock UHD surveillance

Industrial sites adopting 5G achieve sub-10 ms latency, allowing 4K cameras to stream uninterrupted while embedded AI flags anomalies such as equipment defects or safety breaches. Manufacturers report 37% fewer safety incidents and a 42% uptick in quality-control efficiency as edge inference replaces manual inspection.

AI crowd analytics in mega Asian hubs

Transit authorities in Singapore and South Korea deploy analytics that distinguish routine movement from security threats, cutting false alarms by 76% and boosting detection accuracy to 94%. Passenger-flow insights improve staffing decisions, raising peak-hour throughput by 23%.

GPU shortages raise AI-camera costs

Edge-AI cameras face component cost spikes of 18-25% as delivery windows for vision accelerators stretch to 26 weeks. Smaller vendors without preferential allocation risk delays that can shift channel share to larger rivals.

Other drivers and restraints analyzed in the detailed report include:

- Safe-city programs accelerate in GCC capitals

- Cloud-native VSaaS adoption in North-American retail

- Data localization complicates cloud roll-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IP cameras commanded a 64.35% revenue share in 2025, and their installed base is expanding on the back of PoE simplicity and software-defined functionality. Hybrid models, which bridge coaxial infrastructure to IP analytics, are advancing at a 11.84% CAGR as cost-sensitive users phase out legacy analog gear. Value is migrating from the lens to the algorithm; consequently, software-centric entrants capture margin by embedding AI into video management systems that formerly relied on human monitoring.

Market incumbents now bundle API-rich platforms that integrate intrusion sensors, access control, and business dashboards. This service-oriented pivot positions vendors to monetize recurring analytics subscriptions rather than one-time camera sales, a trend reshaping revenue recognition across the surveillance camera market.

Dome units retained 31.45% of 2025 sales thanks to vandal resistance and aesthetic appeal in retail aisles and office lobbies. PTZ models, with a 12.88% CAGR, allow operators to track suspects across wide areas, making a single device the functional equivalent of multiple fixed cameras and supporting higher average selling prices. Bullet designs remain favored for perimeter defense where directional deterrence is paramount, while turret and multi-sensor innovations answer niche requirements for 360° coverage without fisheye distortion.

Manufacturers are embedding auto-tracking algorithms that reposition PTZ lenses in real time, ensuring that the surveillance camera market size for PTZ solutions captures incremental share from static devices in logistics hubs and transport terminals. At the same time, thermographic options are being specified for smoke-filled or zero-light environments to safeguard critical energy assets.

Geography Analysis

Asia accounted for 40.60% of global revenue in 2025 and continues to expand at an 10.78% CAGR as China's public-safety investments and India's smart-city tenders accelerate procurement cycles. Singapore's metro upgraded to AI crowd analytics that trimmed false alerts by 76% while boosting threat recognition accuracy to 94%. Regional manufacturers capitalize on domestic scale to iterate rapidly, closing technology gaps with Western competitors.

North America holds the second-largest share, underpinned by retail VSaaS adoption and federal initiatives protecting critical infrastructure. Forty-four percent of users now operate at least one cloud-connected site, a figure that grows as multi-location chains consolidate security operations. Privacy mandates in Canada spur demand for anonymization tools, influencing product roadmaps oriented toward compliance-ready analytics.

Europe's market is shaped by GDPR and the emerging AI Act, pushing suppliers to integrate privacy-preserving functions such as on-device redaction. The United Kingdom modernizes an extensive legacy network with edge AI, while Germany emphasizes industrial integration where cameras feed quality-control systems. Nordic municipalities deploy cameras not only for safety but also to manage congestion and environmental metrics, expanding application breadth.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Zhejiang Dahua Technology Co., Ltd.

- Axis Communications AB

- Bosch Security Systems GmbH

- Honeywell International Inc.

- Panasonic Corporation

- Motorola Solutions, Inc. (Avigilon)

- Genetec Inc.

- Hanwha Vision Co., Ltd. (Hanwha Techwin)

- Cisco Systems Inc.

- CP Plus GmbH and Co. KG

- Teledyne FLIR LLC

- Johnson Controls Intl. plc (Tyco)

- Pelco, Inc.

- Uniview Technologies Co., Ltd.

- Arlo Technologies, Inc.

- Eagle Eye Networks, Inc.

- Swann Communications Pty Ltd.

- Lorex Technology Inc.

- Verkada Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enabling 5G-Edge Networks Unlocking Real-Time UHD Surveillance in Smart Factories

- 4.2.2 Mandates for AI-based Crowd Analytics in Mega Asian Transport Hubs

- 4.2.3 Rapid Roll-out of Safe-City Programs in Middle-East Oil Economies

- 4.2.4 Shift to Cloud-Native VSaaS Among North-American Multi-site Retailers

- 4.2.5 Insurance Incentives for Connected-Home Cameras in Europe's High-Risk Urban Zones

- 4.2.6 Heightened Compliance Requirements for Critical Infrastructure under US TSA Directives

- 4.3 Market Restraints

- 4.3.1 Escalating GPU Shortages Inflating AI-Camera BOM Costs

- 4.3.2 Data-Localization Laws Hindering Cross-Border Video Storage in GCC and ASEAN

- 4.3.3 Privacy-Centric OS Updates Curbing On-Device Face-Recognition in EU

- 4.3.4 Power Constraints in Off-Grid Mining Sites Limiting UHD Adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Analog Cameras

- 5.1.2 IP Cameras

- 5.1.3 Hybrid Cameras

- 5.2 By Form Factor

- 5.2.1 Dome Cameras

- 5.2.2 Bullet Cameras

- 5.2.3 PTZ Cameras

- 5.2.4 Box Cameras

- 5.2.5 Turret Cameras

- 5.2.6 Fisheye Cameras

- 5.2.7 Thermal Cameras

- 5.3 By Resolution

- 5.3.1 Non-HD (<=720p)

- 5.3.2 HD (720p-1080p)

- 5.3.3 Full HD (1080p-2K)

- 5.3.4 Ultra HD / 4K (>=4K)

- 5.4 By Connectivity

- 5.4.1 Wired

- 5.4.2 Power-over-Ethernet (PoE)

- 5.4.3 Wireless (Wi-Fi/Zigbee)

- 5.4.4 Cellular (4G/5G NB-IoT)

- 5.5 By Deployment Model

- 5.5.1 On-Premise

- 5.5.2 Cloud / VSaaS

- 5.5.3 Edge / On-Device Storage

- 5.5.4 Hybrid

- 5.6 By End-User Industry

- 5.6.1 Banking and Financial Institutions (BFSI)

- 5.6.2 Transportation and Infrastructure

- 5.6.3 Government and Defense

- 5.6.4 Healthcare Facilities

- 5.6.5 Industrial and Manufacturing

- 5.6.6 Retail and Hospitality

- 5.6.7 Enterprise and Commercial Offices

- 5.6.8 Residential / Smart Home

- 5.6.9 Logistics and Warehousing

- 5.6.10 Educational Campuses

- 5.6.11 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Nordics

- 5.7.3.7 Rest of Europe

- 5.7.4 APAC

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Indonesia

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 ASEAN-5

- 5.7.4.9 Rest of APAC

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Qatar

- 5.7.5.4 Kuwait

- 5.7.5.5 Oman

- 5.7.5.6 Bahrain

- 5.7.5.7 Turkey

- 5.7.5.8 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Kenya

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hangzhou Hikvision Digital Technology Co., Ltd.

- 6.4.2 Zhejiang Dahua Technology Co., Ltd.

- 6.4.3 Axis Communications AB

- 6.4.4 Bosch Security Systems GmbH

- 6.4.5 Honeywell International Inc.

- 6.4.6 Panasonic Corporation

- 6.4.7 Motorola Solutions, Inc. (Avigilon)

- 6.4.8 Genetec Inc.

- 6.4.9 Hanwha Vision Co., Ltd. (Hanwha Techwin)

- 6.4.10 Cisco Systems Inc.

- 6.4.11 CP Plus GmbH and Co. KG

- 6.4.12 Teledyne FLIR LLC

- 6.4.13 Johnson Controls Intl. plc (Tyco)

- 6.4.14 Pelco, Inc.

- 6.4.15 Uniview Technologies Co., Ltd.

- 6.4.16 Arlo Technologies, Inc.

- 6.4.17 Eagle Eye Networks, Inc.

- 6.4.18 Swann Communications Pty Ltd.

- 6.4.19 Lorex Technology Inc.

- 6.4.20 Verkada Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment