PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065751

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065751

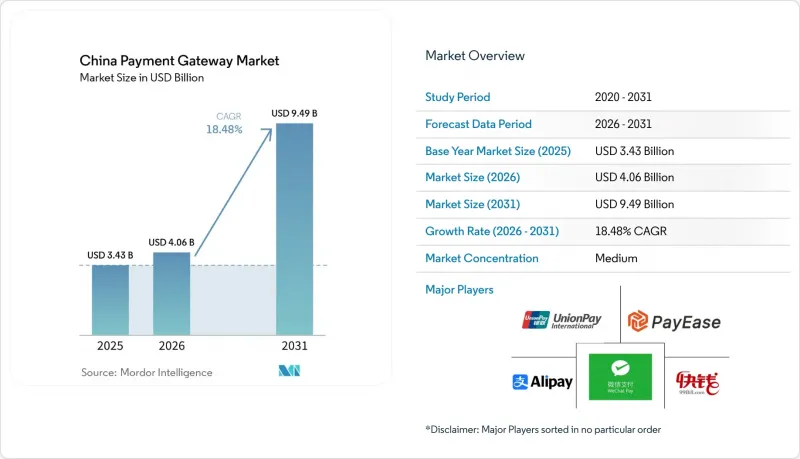

China Payment Gateway - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, china payment gateway market size in 2026 is estimated at USD 4.06 billion, growing from 2025 value of USD 3.43 billion with 2031 projections showing USD 9.49 billion, growing at 18.48% CAGR over 2026-2031.

This report is Segmented by Type (Hosted, Non-Hosted, Platform-Based Super-App Gateways and More), Enterprise Size (Micro, Small, Medium, and More), End-User Industry (Retail and E-Commerce, Travel and Hospitality and More), Payment-Method Integration (Digital Wallets, and More), Deployment Environment (Mobile-App SDK, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China Payment Gateway Market Trends and Insights

Growing E-commerce and M-commerce Surge

Mobile commerce represented 82% of all online spending in 2024, lifting transaction volumes for every serious gateway provider. Live-stream sales, social shopping and influencer-led "instant buy" features escalate demand for sub-second authorisation speeds. Merchants increasingly favour API-only and embedded gateways that remove checkout friction, elevating conversion and repeat purchase rates. Demographic shifts show first-time digital payers emerging from low-income groups, expanding the total addressable user base. These factors collectively position the China payment gateway market for sustained high-teens growth as online retail diversifies beyond the coastal megacities.

Government Cash-less Initiatives and Policy Support

The State Council's March 2024 directive mandated universal acceptance of digital payments in public services and retail, accelerating merchant on-boarding across micro businesses. The People's Bank of China simplified KYC for foreign visitors, enabling larger transaction limits and smoother registration. Harmonised data-flow rules released in 2024 eased cross-border processing, supporting gateway expansion into new trade corridors. Preferential fee caps for small merchants lowered entry barriers, directly boosting gateway penetration in community retail. Collectively, proactive governance keeps the China payment gateway market on an inclusive growth path.

Alipay-WeChat Duopoly Limits New Entrants

Alipay and WeChat Pay together captured more than 90% of mobile transactions in 2024, locking merchants and consumers into closed ecosystems. Their deep integration across social, commerce and finance produces high switching costs that discourage experimentation with alternative gateways. Foreign processors have struggled to build scale, with most remaining confined to niche cross-border use cases. As the duopoly layers biometric authentication, mini-programs and super-app perks around payments, competitive gaps widen further. This dynamic acts as a structural drag on the China payment gateway market's diversity, even while total volumes keep expanding.

Other drivers and restraints analyzed in the detailed report include:

- Cross-border E-commerce Demand

- Digital Yuan (e-CNY) Rollout Boosts Gateway Adoption

- Rising Compliance Burden and Licensing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hosted gateways dominated with 77.15% of China payment gateway market share in 2025, yet the segment faces decelerating growth as merchants migrate to agile architectures. The China payment gateway market size attributable to hosted options reached roughly USD 2.65 billion in 2025, reflecting widespread adoption among SMEs that prefer turnkey compliance. API-only and embedded gateways log the fastest 18.62% CAGR because brands want checkout embedded inside live streams, social feeds and in-game purchases. Super-app gateways from Tencent and Ant offer built-in traffic, loyalty and marketing tools, reducing acquisition costs for merchants. Enterprises demanding custodial data control still select non-hosted or on-premise deployments, particularly in regulated sectors such as finance and telecom. Palm-scan payments, piloted by Tencent, exemplify how embedded authentication layers can differentiate user experience and foster loyalty.

For independent software vendors, API-first design shortens integration cycles from weeks to days, lowering engineering overheads. The architecture also facilitates rapid roll-out of value-added features such as instalments, rewards and insurance. As 5G and edge computing cut latency, gateways offer real-time fraud scoring that enhances approval rates without sacrificing security. Over the forecast horizon, API-centric products are expected to take incremental share from hosted platforms, though hybrid stacks will persist in multi-channel merchants that require both simplicity and customisation.

Micro enterprises delivered only single-digit revenue in absolute terms but posted a 19.91% CAGR, the fastest within the China payment gateway market. Simplified onboarding, reduced MDR fees and government subsidies have lowered entry thresholds, allowing street vendors and rural stores to accept QR payments within minutes. Large enterprises continue to drive scale, often deploying multiple gateways for redundancy and regional coverage. The China payment gateway market size attached to SME segments accounted for roughly USD 2.14 billion in 2025, signifying the importance of this cohort to processors and acquirers alike. As supply-chain digitisation accelerates among township-level firms, gateway vendors are releasing mini-programme toolkits that integrate inventory, marketing and settlement in one workflow.

Medium enterprises typically adopt hosted gateways first, then transition to API-rich platforms once transaction volumes warrant customised flows. Government evaluation metrics for small-business finance push banks to extend bespoke payment support, often in partnership with fintechs. This collaboration spurs innovation such as offline-capable QR codes for low-connectivity areas. For micro merchants, fee holidays and curated training programmes improve digital literacy, further enlarging the addressable base for the China payment gateway market.

List of Companies Covered in this Report:

- Alipay (Ant Group)

- WeChat Pay (Tencent Holdings)

- UnionPay International

- PayEase

- 99Bill Corporation

- Mastercard Inc.

- JD Pay

- ChinaPnR

- iPS

- Lakala Payment

- Yeepay

- Allinpay

- LianLian Pay

- PingPong Payments

- Airwallex

- Adyen

- Worldpay (FIS)

- GZ Bill

- Ping An OneConnect

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce and m-commerce surge

- 4.2.2 Government cash-less initiatives and policy support

- 4.2.3 Smartphones and 5G enable seamless checkout

- 4.2.4 Cross-border e-commerce demand

- 4.2.5 Digital Yuan (e-CNY) rollout boosts gateway adoption

- 4.2.6 AI-driven fraud prevention attracts merchants

- 4.3 Market Restraints

- 4.3.1 Alipay-WeChat duopoly limits new entrants

- 4.3.2 Rising compliance burden and licensing costs

- 4.3.3 Data-localization and cybersecurity barriers for foreign PSPs

- 4.3.4 Urban market saturation, rural onboarding lag

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hosted

- 5.1.2 Non-Hosted

- 5.1.3 Platform-based Super-App Gateways

- 5.1.4 API-Only / Embedded

- 5.1.5 On-premise Self-Hosted

- 5.2 By Enterprise Size

- 5.2.1 Micro Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.2.3 Large Enterprises

- 5.3 By End-User Industry

- 5.3.1 Retail and E-commerce

- 5.3.2 Travel and Hospitality

- 5.3.3 BFSI

- 5.3.4 Media and Entertainment

- 5.3.5 Education

- 5.3.6 Healthcare and Tele-medicine

- 5.3.7 Government and Public Services

- 5.3.8 Others

- 5.4 By Payment-Method Integration

- 5.4.1 Digital Wallets

- 5.4.2 Card Schemes

- 5.4.3 Account-to-Account / QR

- 5.4.4 Buy-Now-Pay-Later

- 5.4.5 Cryptocurrency / CBDC (e-CNY)

- 5.5 By Deployment Environment

- 5.5.1 Mobile-App SDK

- 5.5.2 Web Checkout

- 5.5.3 In-store POS / QR

- 5.5.4 Cross-border Gateway

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Analyst Ranking of Payment Gateways in China

- 6.4 Market Share Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 Alipay (Ant Group)

- 6.5.2 WeChat Pay (Tencent Holdings)

- 6.5.3 UnionPay International

- 6.5.4 PayEase

- 6.5.5 99Bill Corporation

- 6.5.6 Mastercard Inc.

- 6.5.7 JD Pay

- 6.5.8 ChinaPnR

- 6.5.9 iPS

- 6.5.10 Lakala Payment

- 6.5.11 Yeepay

- 6.5.12 Allinpay

- 6.5.13 LianLian Pay

- 6.5.14 PingPong Payments

- 6.5.15 Airwallex

- 6.5.16 Adyen

- 6.5.17 Worldpay (FIS)

- 6.5.18 GZ Bill

- 6.5.19 Ping An OneConnect

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment