PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065753

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065753

Domestic Service Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

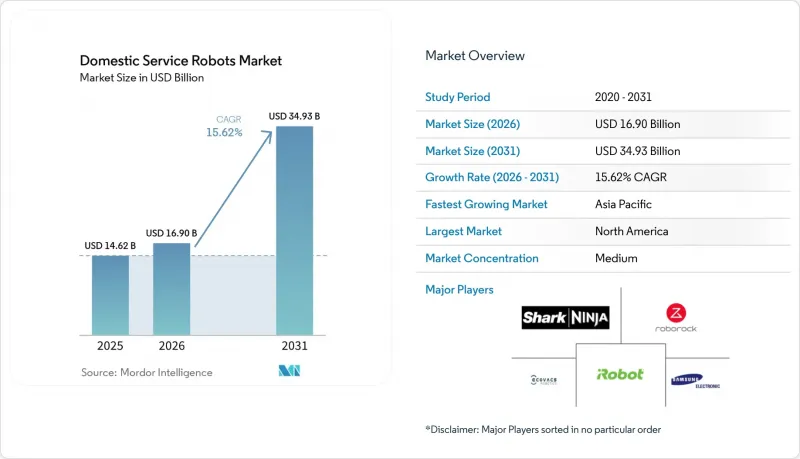

According to Mordor Intelligence, the domestic service robots market size is expected to grow from USD 14.62 billion in 2025 to USD 16.9 billion in 2026 and is forecast to reach USD 34.93 billion by 2031 at 15.62% CAGR over 2026-2031.

This report is Segmented by Robot Type (Floor-Cleaning Robots, Lawn-Mowing Robots, and More), Application (Vacuuming and Mopping, Lawn Mowing, Pool Cleaning, and More), Connectivity and Intelligence Level (Stand-Alone, Wi-Fi Connected, and More), Distribution Channel (Online Retail, Offline Retail, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Global Domestic Service Robots Market Trends and Insights

Growing adoption in smart-home ecosystems

Manufacturers repositioned domestic robots as roaming control hubs rather than isolated gadgets. Voice-assistant tie-ins, such as Alexa integration with mobile platforms, enabled room-to-room orchestration of lighting, climate, and entertainment, elevating robots to the centre of home automation. Hardware vendors prioritised open APIs to ensure frictionless onboarding with existing sensors and cameras. The shift attracted ecosystem investors who view recurring software updates as value retention levers.

Aging population and assisted-living demand

Japan's super-aged society catalysed social-assistive robot pilots that supplemented overstretched caregiving staff. Clinical studies recorded moderate to high acceptance of robot-mediated therapy for autism and dementia, accelerating grant funding for companion platforms. Government incentives for in-home monitoring solutions encouraged vendors to embed fall-detection and medication-reminder modules, fortifying the domestic service robots market growth narrative.

Data privacy and cybersecurity risks

High-profile exploits in 2024 allowed attackers to commandeer robot vacuums, stream video feeds, and broadcast hate speech, shaking consumer confidence. The EU Data Act, effective September 2025, placed explicit obligations on device makers to share data only with user consent and to enable data porting. Compliance investments rose as firms adopted zero-trust architectures, secure boot, and end-to-end encryption. Vendors able to validate privacy-by-design gained a marketing edge.

Other drivers and restraints analyzed in the detailed report include:

- Labour shortages for domestic chores

- Subscription-based RaaS lowers CAPEX

- Ethical worries over child-robot bonding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Floor-cleaning models controlled a 64.70% domestic service robots market share in 2025, benefiting from early commercialisation and falling navigation sensor costs. Companion robots, however, are projected to mark an 17.60% CAGR through 2031, powered by demographic shifts and improved conversational AI. The domestic service robots market size for companion units is expected to rise sharply as healthcare insurers test reimbursement schemes for in-home monitoring. Roborock's leap to 16% global share illustrated the advantage of agile firmware updates and regionally sourced components. Kitchen-automation prototypes, including robotic arms that stir, flip, and plate meals, moved from restaurant pilots to premium residential showrooms, widening the innovation funnel.

The lawn-mowing subcategory recorded double-digit growth in large-lot suburbs, boosted by improvements in boundary-free visual SLAM. Pool-cleaning robots preserved a niche among luxury homeowners who prioritise continuous water-quality monitoring. Pet-care robots, though small in absolute numbers, saw a venture funding influx due to rising pet humanisation. Cross-segment feature migration, such as self-emptying dustbins appearing in lawn mowers, signalled engineering synergies that compress product-development cycles.

Vacuuming and mopping retained 65.60% share of the domestic service robots market size in 2025, cementing their role as gateway purchases that familiarised households with robotic autonomy. Elder-care and companionship applications are forecast to deliver an 17.70% CAGR to 2031 as ageing societies demand fall alerts, cognitive stimulation, and remote vitals logging. The domestic service robots market share of care applications is set to expand when insurers factor reduced hospital readmissions into premium calculations. Surveillance functions gained traction where local regulations allowed mobile cameras, although privacy sensitivities limited blanket adoption. Multi-modal units that blend cleaning, security, and entertainment within one chassis proliferated, enabling upsell paths without new hardware investment.

Demand for robotic lawn services accelerated in regions with labour shortages and high hourly wage rates. Developers addressed early adoption hurdles-such as boundary wire placement-through camera-based geofencing. Pool-cleaning robots achieved steady replacement demand as filter technology improvements reduced maintenance intervals. Functional diversification underscored a trend where single robots tackle multiple chores during idle cycles, maximising return on battery capacity.

Geography Analysis

North America commanded 38.30% of the domestic service robots market share in 2025, buoyed by high disposable income, established smart-home penetration, and clear liability frameworks. Retailers integrated extended warranties that eased adoption anxiety. The region's subscription uptake amplified recurring revenue visibility.

Asia-Pacific is projected to post a 19.70% CAGR to 2031, driven by South Korea's world-leading robot density and Japan's demographic urgency. Chinese brands leveraged scale manufacturing and local component ecosystems to offer competitive price-performance ratios, facilitating export surges once domestic demand plateaued.

Europe's domestic service robots market size expanded as regulators finalised the Data Act and AI liability rules, creating a harmonised yet strict compliance landscape that favoured firms with strong privacy credentials. Scandinavian countries piloted energy-efficient charging stations tied to renewable power grids, tying domestic robots to sustainability targets. Western European consumers displayed heightened ethical scrutiny, prompting transparent data-handling disclosures.

South America and the Middle East and Africa recorded early-stage growth. Currency volatility and import duties weighed on upfront sales, but subscription offerings reduced sticker shock. Local distributors partnered with global brands to navigate customs and after-sales logistics, while city authorities tested robot-assisted waste sorting in gated communities.

- iRobot Corporation

- Ecovacs Robotics Co. Ltd.

- Roborock Technology Co. Ltd.

- Samsung Electronics Co. Ltd.

- Neato Robotics LLC

- SharkNinja Operating LLC

- Xiaomi Corp. (Dreame & Mijia)

- Dyson Technology Ltd.

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Cecotec Innovaciones S.L.

- Husqvarna Group (Gardena)

- Maytronics Ltd.

- Segway-Ninebot Group

- Ubtech Robotics Inc.

- ZMP Inc.

- F&P Robotics AG

- Bobsweep Inc.

- ILIFE Innovation Ltd.

- Tertill Corporation

- Eufy (Anker Innovations)

- Karcher GmbH & Co. KG

- Midea Group (Cozii & Eureka)

- Matic Robotics

- Trifo Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption in smart-home ecosystems

- 4.2.2 Aging population and assisted-living demand

- 4.2.3 Labour shortages for domestic chores

- 4.2.4 Home-insurance risk-mitigation programs

- 4.2.5 Subscription-based RaaS lowers CAPEX

- 4.2.6 Indoor-air-quality driven hygiene labels

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cyber-security risks

- 4.3.2 High upfront cost of multi-function robots

- 4.3.3 Fragmented domestic-IoT standards

- 4.3.4 Ethical worries over child-robot bonding

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of Substitute Products

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of New Entrants

- 4.8 Impact of Macroeconomic Factors

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Robot Type

- 5.1.1 Floor-Cleaning Robots

- 5.1.2 Lawn-Mowing Robots

- 5.1.3 Pool-Cleaning Robots

- 5.1.4 Companion and Social-Interaction Robots

- 5.1.5 Kitchen and Food-Preparation Robots

- 5.1.6 Pet-Care Robots

- 5.1.7 Other Robot Types

- 5.2 By Application

- 5.2.1 Vacuuming and Mopping

- 5.2.2 Lawn Mowing

- 5.2.3 Pool Cleaning

- 5.2.4 Surveillance and Home Security

- 5.2.5 Companionship and Elderly Care

- 5.2.6 Pet Entertainment and Feeding

- 5.2.7 Other Applications

- 5.3 By Connectivity and Intelligence Level

- 5.3.1 Stand-alone (No Connectivity)

- 5.3.2 Wi-Fi Connected

- 5.3.3 AI-Assisted (Visual-SLAM etc.)

- 5.3.4 Multi-Robot Coordinated Systems

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.4.3 Direct Subscription / RaaS

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 iRobot Corporation

- 6.4.2 Ecovacs Robotics Co. Ltd.

- 6.4.3 Roborock Technology Co. Ltd.

- 6.4.4 Samsung Electronics Co. Ltd.

- 6.4.5 Neato Robotics LLC

- 6.4.6 SharkNinja Operating LLC

- 6.4.7 Xiaomi Corp. (Dreame & Mijia)

- 6.4.8 Dyson Technology Ltd.

- 6.4.9 LG Electronics Inc.

- 6.4.10 Panasonic Holdings Corp.

- 6.4.11 Cecotec Innovaciones S.L.

- 6.4.12 Husqvarna Group (Gardena)

- 6.4.13 Maytronics Ltd.

- 6.4.14 Segway-Ninebot Group

- 6.4.15 Ubtech Robotics Inc.

- 6.4.16 ZMP Inc.

- 6.4.17 F&P Robotics AG

- 6.4.18 Bobsweep Inc.

- 6.4.19 ILIFE Innovation Ltd.

- 6.4.20 Tertill Corporation

- 6.4.21 Eufy (Anker Innovations)

- 6.4.22 Karcher GmbH & Co. KG

- 6.4.23 Midea Group (Cozii & Eureka)

- 6.4.24 Matic Robotics

- 6.4.25 Trifo Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment