PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065773

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065773

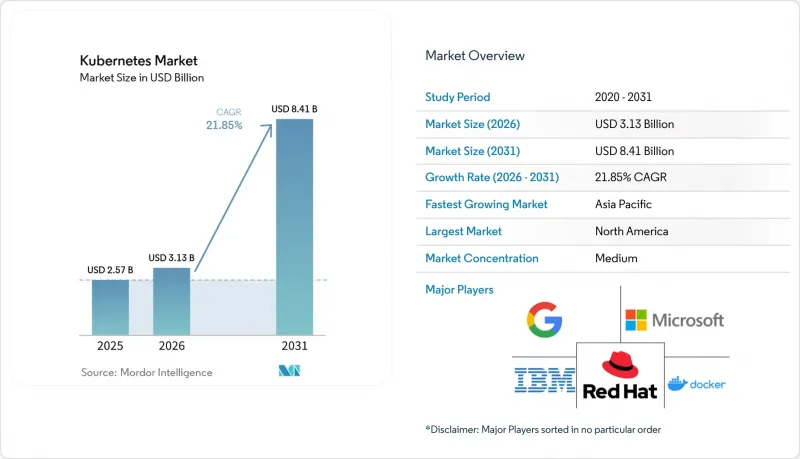

Kubernetes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the kubernetes market size is expected to grow from USD 2.57 billion in 2025 to USD 3.13 billion in 2026 and is forecast to reach USD 8.41 billion by 2031 at 21.85% CAGR over 2026-2031.

This report is Segmented by Component (Solutions and Services), Deployment Model (Self-Hosted Kubernetes and Managed Kubernetes), Organization Size (Small and Medium-Sized Enterprises (SMEs) and Large Enterprises), End User Vertical (Banking, Financial Services, and Insurance (BFSI), Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Kubernetes Market Trends and Insights

Advent of Microservices

Organizations are dismantling monoliths in favor of smaller, independently deployable services that demand sophisticated orchestration, and Kubernetes excels at that role. Eighty percent of enterprises plan to build most new applications on cloud-native stacks within five years. Purpose-built design patterns such as sidecar, ambassador, and adapter are mainstream, improving modularity and maintainability. As this design shift continues, the Kubernetes market becomes a strategic backbone for faster release cycles and business agility, transforming platform-engineering priorities across industries.

Increased Adoption of AI and ML Workloads

Compute-intensive AI initiatives benefit from Kubernetes functions such as node autoscaling, GPU scheduling, and service resilience. More than half of surveyed enterprises already run AI/ML workloads in Kubernetes clusters. Sector-specific tools like Kubeflow streamline model training, while a Google, ByteDance, Red Hat collaboration has optimized load balancing and model-server performance for large-language-model inference. The result is a wider addressable base for AI-ready infrastructure and an expanding Kubernetes market.

Lack of Skilled Talent Pool

Specialized know-how remains scarce as 37% of IT leaders report a skills gap across DevOps and DevSecOps. The steep learning curve fuels the rise of dedicated platform-engineering teams and encourages investment in automation. Enterprises also lean on managed service providers to bridge expertise gaps while modernizing workloads previously tied to legacy virtualization stacks.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Managed Kubernetes Services

- Expansion of Hybrid and Multi-Cloud Strategies

- Security and Compliance Complexities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions still form the largest slice at 55.40% of the Kubernetes market in 2025, covering core distributions and management add-ons. The Services arm, however, is advancing at a 23.3% CAGR as enterprises seek migration blueprints, performance tuning, and continuous compliance advice. A rising number of consulting engagements focus on vertical use-cases-healthcare, finance, telecommunications - where governance requirements are strict and downtime is intolerable. The Kubernetes market for services is expected to more than double by 2031 as certification programs and domain-specific frameworks attract new integrators.

The surge also reflects widening complexity between Kubernetes feature sets and operator know-how. Cloud4C notes that 59% of adopters deem compliance their chief pain point, creating a pull for specialized audit and remediation services. Managed Kubernetes subscriptions further accelerate consumption by shifting SLA enforcement and upgrade chains to vendors, a pattern especially resonant with resource-constrained teams wanting predictable cost envelopes.

Managed offerings dominate with 62.30% of current spend, underpinned by the hyperscalers' managed Kubernetes services. Growth now clusters around multi-cloud managed variants, projected to climb at 22.4% CAGR. Organizations balancing latency, sovereignty, and spending spread workloads across AWS, Azure, Google Cloud, and on-premises assets, turning Kubernetes into the neutrality layer for policy and placement. Kubernetes market for multi-cloud deployments is reinforced as enterprises insist on avoiding single-provider lock-in and pursue optimized utilization.

Self-hosted clusters retain relevance among firms with bespoke security mandates or mainframe adjacency. Hybrid models serve as stepping-stones, letting teams containerize critical applications internally while bursting peaks to public clouds. Tool vendors are rolling out single-pane dashboards, GitOps pipelines, and policy engines that abstract differences among clouds, a move that compresses operational overhead and widens the Kubernetes market.

Geography Analysis

North America secured 36.40% of global revenue in 2025, anchored by the United States, which accounts for more than half of Kubernetes users worldwide. Hyperscale cloud footprints, early-mover enterprises, and deep developer communities sustain regional leadership. AI-infused workloads, especially in finance and retail, intensify Kubernetes adoption, and a patchwork of sectoral regulations (HIPAA, FISMA) spurs investment in security automation and policy gateways. Market participants here increasingly deploy multi-cloud blueprints, making Kubernetes the universal substrate for workload portability.

Asia-Pacific is the fastest-growing region with a 22.6% CAGR forecast for 2026-2031. Widespread digitization, 5G buildouts, and cloud data-center expansion in China, India, and Japan ignite demand. CAST AI's move into India exemplifies provider momentum in the region. Domestic giants such as Alibaba Cloud promote tailored Kubernetes stacks that satisfy local compliance, sustaining momentum. Manufacturing use-cases-smart factories, supply-chain telemetry-further contribute to the Kubernetes market expansion.

Europe commands a substantial slice, buoyed by GDPR-focused security spending and strong open-source culture. Enterprises in Germany, the United Kingdom, and France emphasize hybrid architectures to balance sovereignty and agility. Kubernetes adoption inside the banking and telco segments supports core system modernization. Community collaboration, including Cloud Native Computing Foundation (CNCF) meetups and code events, nurtures a robust contributor base that accelerates enterprise trust. Emerging hubs in the Middle East and Africa and South America, while smaller, display steady uptake as localized cloud availability zones come online, further widening the global Kubernetes market footprint.

- Google LLC

- Microsoft Corporation

- Amazon Web Services, Inc.

- Red Hat, Inc. (IBM)

- IBM Corporation

- VMware, Inc.

- Oracle Corporation

- SUSE (Rancher Labs)

- Cisco Systems, Inc.

- Alibaba Cloud

- Tencent Cloud

- Huawei Technologies Co., Ltd.

- DigitalOcean, LLC

- Mirantis, Inc.

- Platform9 Systems, Inc.

- Fairwinds

- Nutanix, Inc.

- Docker, Inc.

- Canonical Ltd.

- Ionos SE

- KubeSphere (QingCloud)

- Spectro Cloud

- Weaveworks

- HashiCorp

- Portainer.io

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advent of Microservices

- 4.2.2 Increased Adoption of AI and ML Workloads

- 4.2.3 Growing Demand for Managed Kubernetes Services

- 4.2.4 Expansion of Hybrid and Multi-Cloud Strategies

- 4.2.5 Edge-Computing Adoption with Lightweight K8s Distros

- 4.2.6 Kubernetes-native FinOps Automation Reducing TCO

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Talent Pool

- 4.3.2 Security and Compliance Complexities

- 4.3.3 Control-Plane Cost Escalation under Autoscaling

- 4.3.4 Hyperscaler Dominance Limits OSS Monetisation

- 4.4 Key Regulatory Landscape

- 4.4.1 North America

- 4.4.1.1 HIPAA

- 4.4.1.2 FISMA

- 4.4.1.3 CIS Kubernetes Benchmark

- 4.4.1.4 PIPEDA

- 4.4.2 Europe

- 4.4.2.1 GDPR

- 4.4.3 Asia-Pacific

- 4.4.3.1 China Cybersecurity Law

- 4.4.3.2 India DPDP Act

- 4.4.3.3 CERT-In Guidelines

- 4.4.3.4 IRAP (Australia)

- 4.4.4 South America

- 4.4.4.1 LGPD - Brazil

- 4.4.4.2 Mexico Federal DP Law

- 4.4.5 Middle East and Africa

- 4.4.5.1 UAE DP Law

- 4.4.5.2 Dubai ESC Guidelines

- 4.4.5.3 Saudi CCRF

- 4.4.1 North America

- 4.5 Industry Ecosystem Analysis

- 4.6 Impact of Macro-Economic Factors

- 4.7 Assessment of Key Use Cases

- 4.7.1 Large-Scale Application Deployment

- 4.7.2 High-Performance Computing

- 4.7.3 AI and ML Workloads

- 4.7.4 Hybrid and Multi-Cloud Deployments

- 4.7.5 Other Emerging Use Cases

- 4.8 Market Player Case Studies

- 4.8.1 Huawei - Internal IT Orchestration

- 4.8.2 PayPal - Container Management for Speed

- 4.8.3 Additional Case Studies

- 4.9 Value / Supply-Chain Analysis

- 4.10 Technological Outlook

- 4.11 Porter's Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Bargaining Power of Buyers

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.1.2.1 Managed Services

- 5.1.2.2 Consulting and Support Services

- 5.2 By Deployment Model

- 5.2.1 Self-Hosted Kubernetes

- 5.2.1.1 On-Premise

- 5.2.1.2 Hybrid

- 5.2.2 Managed Kubernetes

- 5.2.2.1 Cloud-based Managed

- 5.2.2.2 Multi-Cloud Managed

- 5.2.1 Self-Hosted Kubernetes

- 5.3 By Organization Size

- 5.3.1 Small and Medium-Sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Vertical

- 5.4.1 Banking, Financial Services, and Insurance (BFSI)

- 5.4.2 Healthcare

- 5.4.3 Media and Entertainment

- 5.4.4 Information Technology (IT) and Telecom

- 5.4.5 Manufacturing

- 5.4.6 Retail

- 5.4.7 Government and Public Sector

- 5.4.8 Other Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Southeast Asia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Google LLC

- 6.4.2 Microsoft Corporation

- 6.4.3 Amazon Web Services, Inc.

- 6.4.4 Red Hat, Inc. (IBM)

- 6.4.5 IBM Corporation

- 6.4.6 VMware, Inc.

- 6.4.7 Oracle Corporation

- 6.4.8 SUSE (Rancher Labs)

- 6.4.9 Cisco Systems, Inc.

- 6.4.10 Alibaba Cloud

- 6.4.11 Tencent Cloud

- 6.4.12 Huawei Technologies Co., Ltd.

- 6.4.13 DigitalOcean, LLC

- 6.4.14 Mirantis, Inc.

- 6.4.15 Platform9 Systems, Inc.

- 6.4.16 Fairwinds

- 6.4.17 Nutanix, Inc.

- 6.4.18 Docker, Inc.

- 6.4.19 Canonical Ltd.

- 6.4.20 Ionos SE

- 6.4.21 KubeSphere (QingCloud)

- 6.4.22 Spectro Cloud

- 6.4.23 Weaveworks

- 6.4.24 HashiCorp

- 6.4.25 Portainer.io

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis