PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065786

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065786

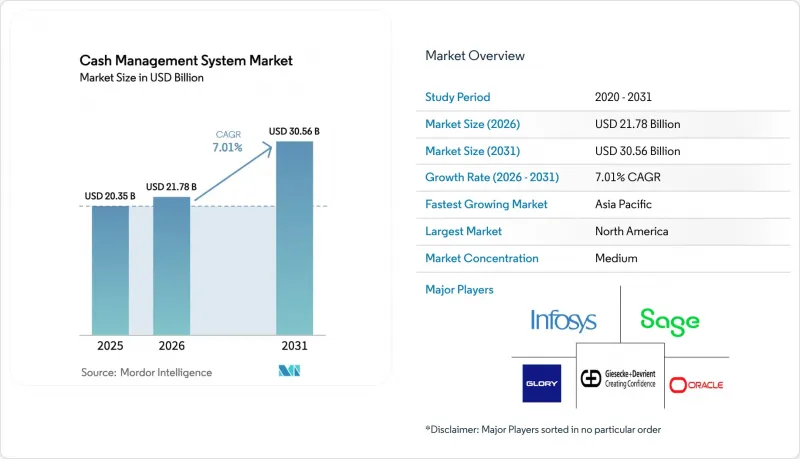

Cash Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cash management system market size is expected to increase from USD 20.35 billion in 2025 to USD 21.78 billion in 2026 and reach USD 30.56 billion by 2031, growing at a CAGR of 7.01% over 2026-2031.

This report Segments the Industry Into by Component (Solution, and Services), Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), Deployment Mode (On-Premise, and Cloud), Operation Type (Cash-Flow Forecasting, Corporate Liquidity Management, and More), End User Industry (Banking, Financial Services and Insurance (BFSI), IT and Telecom, and More), and Geography.

Global Cash Management System Market Trends and Insights

Surge in AI-driven Cash-flow Forecasting

AI models lift forecast accuracy by up to 50%, turning reactive cash tracking into proactive scenario planning across the cash management system market. Algorithms blend historic data with real-time market feeds, allowing treasurers to stress-test liquidity positions and act faster on funding needs. Pandemic-era volatility and rising rates accelerated adoption, and future pairing with blockchain and quantum tools promises still deeper insight.

Expansion of Real-time / Instant Payments Infrastructure

ISO 20022 migration deadlines-for example, the Fedwire switch planned for March 2025-require round-the-clock liquidity and richer transaction data. Banks processing trillions daily, such as J.P. Morgan, are rolling out programmable, blockchain-enabled rails that cut operational steps by 70%. Treasuries must therefore upgrade systems to handle continuous settlement and detailed message formats.

Cybersecurity and Fraud Vulnerabilities

Average US breach losses exceed USD 9 million, underscoring the growing importance of cybersecurity in modern treasury operations, while AI-generated deepfakes add new threats. Treasury units face rising check forgery, card fraud, and payee manipulation, prompting regulators to call for stronger playbooks and identity frameworks. Smaller firms with limited budgets remain particularly exposed.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Cloud-native Treasury Platforms

- Corporate Push for Working-Capital Optimization

- Legacy ERP / Bank-connectivity Integration Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The solutions category accounted for 62.55% of the cash management system market in 2025, reflecting the need for core software licenses and platform rollouts. Yet services revenue is expanding at 13.92% CAGR as firms turn to experts for ISO 20022 mapping, Basel IV rule alignment, and AI model training. Services now drive multi-year engagements covering integration, data migration, and user onboarding. Long projects-often 12-18 months-support recurring consulting revenue that can surpass initial license fees. Managed services that monitor cyber risks and regulatory updates lock in sticky contracts, and vendors package support bundles to guarantee business continuity.

The services boom also signals recognition that success hinges on skills rather than software alone. Consultants configure APIs for dozens of banks, rationalize workflow logic, and deliver dashboards that cut manual reconciliation time. This helps clients trim days of working capital and reduce dependency on aging spreadsheets. As cloud adoption rises, service teams pivot to monitoring, performance tuning, and embedding emerging analytics. This ongoing shift boosts the profile of service providers inside the cash management system market, paving the way for scalable annuity income streams.

Large enterprises retained 59.05% revenue in 2025 thanks to complex multi-bank networks and sizable cash pools within the cash management system market. However, SMEs are posting a 16.02% CAGR, the fastest across organization tiers, as cloud SaaS removes infrastructure and upfront license hurdles. Pre-configured templates and bank-agnostic connectors go live in weeks, letting mid-market CFOs automate 75% of manual tasks. Vendors price seats monthly, aligning with limited budgets and enabling rapid ROI.

Competition intensifies as fintech challengers tailor intuitive dashboards and low-code interfaces for finance teams with minimal IT staff. SME demand reflects regulatory parity: ISO 20022 and fraud rules apply equally to firms of any size. Consequently, the cash management system's market penetration is increasing in the mid-market cohort. Adoption lifts transparency, freeing trapped cash and supporting export growth for smaller manufacturers and online retailers that previously lacked treasury sophistication.

Geography Analysis

North America led with a 39.05% share of the cash management system market in 2025, underpinned by Fed ISO 20022 deadlines, fintech density, and a USD 1.76 trillion working-capital improvement gap. Large banks run programmable payment pilots that slash back-office workloads by up to 70%. The region also ranks highest in fraud losses, spurring demand for AI-driven risk modules.

Asia-Pacific is rising faster, clocking a 13.29% CAGR on the back of 7% annual investment banking growth and SME digitization that accounts for half of transaction banking revenue. Deep domestic e-commerce activity in China and India, coupled with cross-border corridors across ASEAN, requires multi-currency pooling and hedging. Global banks such as BNY Mellon have scaled APAC payment hubs processing USD 2.5 trillion daily.

Europe remains sizable due to MiFID II, EMIR, and pending Basel IV rules. Boards there emphasize ESG integration, with 64% of treasurers citing sustainability metrics as a strategic priority. Nordic corporates pioneer open-banking APIs, while UK firms prepare for the Bank of England's renewed RTGS infrastructure. Emerging regions in the Middle East, Africa, and South America are poised to accelerate once digital ID and regulatory modernization catch up, enlarging the global cash management system market.

- Oracle Corporation

- SAP SE

- Fidelity National Information Services, Inc.

- Kyriba Corp.

- Finastra Group Holdings Limited

- Fiserv, Inc.

- Bottomline Technologies (de), Inc.

- GTreasury LLC

- Infosys Limited

- HCL Technologies Limited

- NTT DATA Corporation

- Aurionpro Solutions Limited

- The Sage Group plc

- Giesecke+Devrient GmbH

- GLORY LTD.

- Coupa Software Incorporated

- HighRadius Corporation

- Serrala Group GmbH

- Treasury Intelligence Solutions GmbH

- Nomentia Oy

- Cashfac Technologies Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI-driven Cash-flow Forecasting

- 4.2.2 Expansion of Real-time / Instant Payments Infrastructure

- 4.2.3 Growing Adoption of Cloud-native Treasury Platforms

- 4.2.4 Corporate Push for Working-capital Optimization

- 4.2.5 Open-banking and API Standardization (ISO 20022)

- 4.2.6 Mandatory Liquidity-Risk Stress-testing (Basel IV)

- 4.3 Market Restraints

- 4.3.1 Cyber-security and Fraud Vulnerabilities

- 4.3.2 Legacy ERP / Bank-connectivity Integration Hurdles

- 4.3.3 Fragmented Cross-border Regulatory Compliance

- 4.3.4 Shortage of Treasury-analytics Talent

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Impact Assessment of Key Stakeholders

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Services

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 By Operation Type

- 5.4.1 Cash-flow Forecasting

- 5.4.2 Corporate Liquidity Management

- 5.4.3 Payables Automation

- 5.4.4 Receivables Automation

- 5.4.5 Treasury and Risk Compliance

- 5.5 By End-user Industry

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare

- 5.5.4 Government and Public Sector

- 5.5.5 Retail and E-commerce

- 5.5.6 Manufacturing

- 5.5.7 Automotive

- 5.5.8 Construction

- 5.5.9 Packaging

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Nigeria

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 Asia-Pacific

- 5.6.5.1 China

- 5.6.5.2 India

- 5.6.5.3 Japan

- 5.6.5.4 South Korea

- 5.6.5.5 ASEAN

- 5.6.5.6 Australia

- 5.6.5.7 New Zealand

- 5.6.5.8 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE

- 6.4.3 Fidelity National Information Services, Inc.

- 6.4.4 Kyriba Corp.

- 6.4.5 Finastra Group Holdings Limited

- 6.4.6 Fiserv, Inc.

- 6.4.7 Bottomline Technologies (de), Inc.

- 6.4.8 GTreasury LLC

- 6.4.9 Infosys Limited

- 6.4.10 HCL Technologies Limited

- 6.4.11 NTT DATA Corporation

- 6.4.12 Aurionpro Solutions Limited

- 6.4.13 The Sage Group plc

- 6.4.14 Giesecke+Devrient GmbH

- 6.4.15 GLORY LTD.

- 6.4.16 Coupa Software Incorporated

- 6.4.17 HighRadius Corporation

- 6.4.18 Serrala Group GmbH

- 6.4.19 Treasury Intelligence Solutions GmbH

- 6.4.20 Nomentia Oy

- 6.4.21 Cashfac Technologies Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment