PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065788

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065788

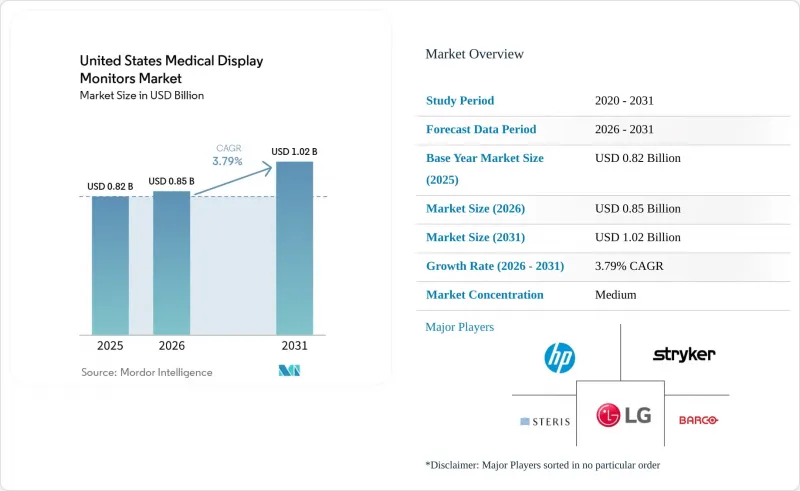

United States Medical Display Monitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031)

According to Mordor Intelligence, the united states medical display monitors market size is projected to be USD 0.82 billion in 2025, USD 0.85 billion in 2026, and reach USD 1.02 billion by 2031, growing at a CAGR of 3.79% from 2026 to 2031.

This report is Segmented by Type (Greyscale, Color), Resolution (Up To 2 MP, 2. 1-4 MP, 4. 1-8 MP, Above 8 MP), Technology (LED-Backlit LCD, OLED, CCFL-Backlit LCD), Application (General Radiology, Mammography, Surgery, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Report Offers the Value (in USD) for the Above Segments.

United States Medical Display Monitors Market Trends and Insights

Imaging-Center Expansion and Reading-Room Modernization

Outpatient imaging remains one of the clearest near-term demand supports for the United States medical display monitors market. Lumexa Imaging operated more than 190 outpatient centers, completed 4 million procedures in 2025, and added 4 new centers in 2026 through joint ventures with Advocate Health and UPMC while targeting 8 to 10 de novo openings annually. Every new center, renovated site, or expanded reading room creates multiple display purchase points across primary diagnostic stations, secondary review screens, and backup work areas. The demand effect is not limited to new buildings because modernization projects also force facilities to reevaluate calibration status, luminance consistency, and monitor age across existing rooms. In the United States medical display monitors market, accreditation-linked procurement behavior matters because facilities that want to maintain high diagnostic standards cannot rely on general commercial screens for every workflow. That pattern supports recurring replacement, recalibration, and service revenue for vendors that can sustain certified QA ecosystems over several years.

4K Minimally Invasive and Hybrid OR Upgrade Cycle

The surgical side of the United States medical display monitors market is entering a more defined 4K and Mini-LED replacement cycle. Sony launched the LMD-32M1MD in January 2025 as the first medical monitor certified to VESA DisplayHDR 1000, and later expanded the lineup in July 2025 with additional 27-inch and 43-inch models for broader procedural use. LG also received FDA 510(k) clearance in September 2025 for the 32HS710S 4K surgical monitor, while EIZO stated that its CuratOR EX3245H Mini-LED model would begin shipping in November 2026 with 1,900 cd/m2 peak brightness and a 1,000,000:1 contrast ratio. These launches matter because a large installed base of pre-4K HD displays from 2015 to 2020 is aging out of its preferred service window in operating rooms and ambulatory settings. Many older systems were purchased for cost efficiency, not for fluorescence guidance, robotic assistance, or sustained high dynamic range performance during long procedures. That gap is creating a replacement wave in the United States medical display monitors market that should stay active as hospitals and ASCs standardize their OR visualization stacks.

High Acquisition Cost for Premium Diagnostic and Surgical Displays

High-end medical displays remain expensive enough to slow unit adoption in parts of the United States medical display monitors market. EIZO launched the RadiForce GX570 in April 2026 as a 5 MP monochrome mammography monitor with a 2,200:1 contrast ratio and an Instant Backlight Booster that reaches 2,500 cd/m2, while Barco positioned Coronis OneLook as a 32 MP breast imaging display for full-resolution review. The gap between a certified medical display and a high-performance commercial monitor can reach USD 5,000 to USD 20,000 per unit, which is significant for smaller facilities that need several stations at once. Accreditation standards still create a floor under demand, because luminance verification and DICOM calibration are not optional in many clinically sensitive workflows. Even so, budget pressure is strongest in rural hospitals, independent imaging operators, and lower-volume specialty settings where capital committees review every replacement closely. This keeps procurement disciplined and slows the speed at which the United States medical display monitors market can fully migrate to the highest resolution and brightest premium tiers.

Other drivers and restraints analyzed in the detailed report include:

- FDA-Cleared Digital Pathology Primary Diagnosis Adoption

- AI-Enabled Multi-Modality Workflow Complexity Favors Premium Diagnostic Displays

- Long Replacement Cycles and Lower-Cost Substitute Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Greyscale displays held 61.78% of the United States medical display monitors market share in 2025, which confirms that monochrome visualization still anchors routine radiology and mammography reading volumes. Color displays are projected to record the faster 4.91% CAGR through 2031 as pathology and surgical workflows demand stronger tissue hue fidelity and broader visual context. The United States medical display monitors market still relies on greyscale for high-volume diagnostic work because DICOM GSDF-calibrated monochrome rendering remains the clinical standard for many radiology tasks. That installed base gives greyscale an enduring advantage in replacement demand, even when new use cases are shifting toward color.

Color demand is expanding for clear workflow reasons rather than for cosmetic preference. FDA-cleared pathology systems increasingly reference approved color displays as part of the diagnostic setup, which means monitor selection now sits inside regulated deployment planning instead of general IT sourcing. Surgical visualization is also inherently color dependent because fluorescence guidance, perfusion imaging, and robotic procedures depend on stable rendering during long cases. At the same time, the United States medical display monitors industry is still investing in greyscale product performance, which is visible in EIZO's April 2026 launch of the RadiForce GX570 for mammography use. The type landscape is therefore splitting into 2 durable demand pools, one centered on radiology continuity and another centered on expanding color-critical workflows. That balance keeps greyscale large while allowing color to gain share over the forecast period.

The 2.1 MP to 4 MP band accounted for 32.16% of the United States medical display monitors market size in 2025, which reflects the deep installed base of 3 MP-class workstations used across general imaging and review environments. This band remains the practical center of the market because it covers many diagnostic tasks while staying more accessible to facilities with tighter capital budgets. The United States medical display monitors market continues to favor this range for broad deployment because it offers a workable balance between clinical utility and procurement cost. That is why community hospitals and many outpatient sites still fall within this mid-range tier.

The 4.1 MP to 8 MP band is forecast to grow at a 4.73% CAGR through 2031 as mammography and whole-slide imaging create stronger demand for sustained high-resolution rendering. The April 2024 USPSTF breast cancer screening recommendation lowered the starting age for routine screening to 40, which expands the long-term screening base and supports continued equipment demand in accredited breast imaging settings. At the top end, Barco's Coronis OneLook brings 32 MP capability to breast imaging review, showing how premium resolution is being used to improve throughput in high-volume programs. The United States medical display monitors industry is therefore seeing a reshaping effect rather than a full migration, because mid-range remains dominant while high-resolution demand expands in clinically specific settings. Segments above 8 MP stay niche, but their relevance is rising in breast imaging, advanced surgical applications, and specialized academic environments where panning reduction and full-field review matter.

List of Companies Covered in this Report:

- Advantech Co., Ltd.

- ASUS

- Barco NV

- Canvys (Richardson Electronics, Ltd.)

- Double Black Imaging Corporation

- EIZO Corporation

- FSN Medical Technologies

- FUJIFILM Healthcare Americas Corporation

- HP Development Company, L.P

- Image Diagnostics Inc.

- JVCKENWOOD Corporation

- Karl Storz

- LG Electronics Inc.

- Novanta Inc.

- Olympus America Inc.

- Rein Medical GmbH

- Reshin Monitors

- Sony Group

- Stryker

- STERIS

- WIDE USA

- Winmate Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Imaging-Center Expansion and Reading-Room Modernization

- 4.2.2 4K Minimally Invasive and Hybrid OR Upgrade Cycle

- 4.2.3 Higher Breast Imaging and Oncology Read Volumes

- 4.2.4 AI-Enabled Multi-Modality Workflow Complexity Favors Premium Diagnostic Displays

- 4.2.5 FDA-Cleared Digital Pathology Primary Diagnosis Adoption

- 4.2.6 Zero-Footprint Diagnostic Viewing Raising Remote QA Demand

- 4.3 Market Restraints

- 4.3.1 High Acquisition Cost for Premium Diagnostic and Surgical Displays

- 4.3.2 Long Replacement Cycles and Lower-Cost Substitute Pressure

- 4.3.3 2026 QMSR Compliance Burden for Device Makers

- 4.3.4 Web Viewer Adoption Deferring Some Dedicated Workstation Display Upgrades

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Greyscale

- 5.1.2 Color

- 5.2 By Resolution

- 5.2.1 Up to 2 MP

- 5.2.2 2.1 MP to 4 MP

- 5.2.3 4.1 MP to 8 MP

- 5.2.4 Above 8 MP

- 5.3 By Technology

- 5.3.1 LED-backlit LCD

- 5.3.2 OLED

- 5.3.3 CCFL-backlit LCD

- 5.4 By Application

- 5.4.1 General Radiology and Diagnostic Imaging

- 5.4.2 Mammography

- 5.4.3 Surgery and Interventional Imaging

- 5.4.4 Digital Pathology

- 5.4.5 Dentistry

- 5.4.6 Clinical Review, Education, and Telemedicine

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Imaging Centers and Diagnostic Laboratories

- 5.5.3 Specialty Clinics

- 5.5.4 Ambulatory Surgical Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Advantech Co., Ltd.

- 6.3.2 ASUS

- 6.3.3 Barco NV

- 6.3.4 Canvys (Richardson Electronics, Ltd.)

- 6.3.5 Double Black Imaging Corporation

- 6.3.6 EIZO Corporation

- 6.3.7 FSN Medical Technologies

- 6.3.8 FUJIFILM Healthcare Americas Corporation

- 6.3.9 HP Development Company, L.P

- 6.3.10 Image Diagnostics Inc.

- 6.3.11 JVCKENWOOD Corporation

- 6.3.12 KARL STORZ SE & Co. KG

- 6.3.13 LG Electronics Inc.

- 6.3.14 Novanta Inc.

- 6.3.15 Olympus America Inc.

- 6.3.16 Rein Medical GmbH

- 6.3.17 Reshin Monitors

- 6.3.18 Sony Group Corporation

- 6.3.19 Stryker Corporation

- 6.3.20 Steris

- 6.3.21 WIDE USA

- 6.3.22 Winmate Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment