PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066380

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066380

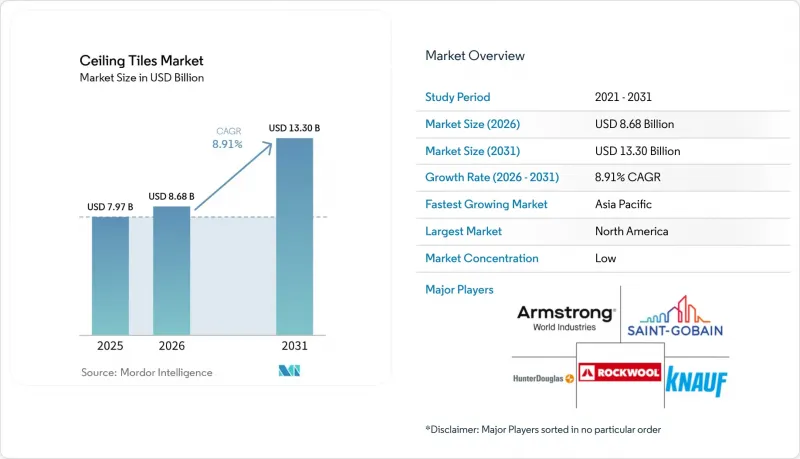

Ceiling Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the ceiling tiles market size is expected to increase from USD 7.97 billion in 2025 to USD 8.68 billion in 2026 and reach USD 13.30 billion by 2031, growing at a CAGR of 8.91% over 2026-2031.

This report is Segmented by Raw Material (Mineral Wool, Metal, Gypsum, and Others), Property (Acoustic and Non-Acoustic), Application (Residential, Commercial, Industrial, and Institutional), and Geography (Asia Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Ceiling Tiles Market Trends and Insights

Rapid Adoption of Acoustic Systems in Open-Plan Offices

As hybrid work models evolve, the demand for quieter collaboration zones intensifies. Rockfon's Sonar dB35 panels, boasting a 0.95 NRC, experienced increased adoption driven by corporate retrofits. Meanwhile, Armstrong's TechZone Ultima system made its mark in the new U.S. Class A office segment. A 2024 study by the Acoustical Society of America revealed a concerning trend: ceiling absorption coefficients dipping below 0.80 are linked to a decline in productivity for floorplates larger than 5,000 sq ft . Knauf's Heradesign wood-wool tiles not only meet the reverberation standards of the WELL Building Standard but also offer the biophilic aesthetics that have gained traction in Europe. These trends highlight the robust demand for acoustic-grade products in the ceiling tiles market.

Green-Building Credits Boosting Mineral-Wool Retrofits in Europe

By 2025, the EU's Building Performance Directive 2024/1275 mandates that governments unveil whole-life carbon benchmarks for public buildings. This move also promotes the use of mineral-wool tiles that come with Environmental Product Declarations. Saint-Gobain's Ecophon Master Rigid, boasting Nordic Swan certification, has gained traction in Germany's retrofit market. Meanwhile, Rockfon's Sonar dB35 line, crafted with recycled content, meets the criteria for BREEAM Excellent credits, bolstering bids for hospitals in the U.K. Given these developments, the European ceiling tiles market is poised for growth, driven by directive-led retrofits.

Energy-Price Volatility Inflating Mineral-Wool Costs

In the first half of 2025, European natural-gas futures increased compared to 2024. This surge in gas prices led to a rise in production costs for both Rockfon and Saint-Gobain. Meanwhile, the U.S. Producer Price Index (PPI) for mineral-wool manufacturing also experienced a year-over-year increase. Additionally, smaller Asian producers, who are importing spot LNG, are experiencing margin compression. This situation is diminishing their competitiveness in the ceiling tiles market.

Other drivers and restraints analyzed in the detailed report include:

- Metro and Airport Build-Outs Mandating Non-Combustible Tiles in Asia

- Digital-Print Gypsum Tiles Enabling Premiumization in GCC Luxury Real Estate

- Threat from Substitutes Such as Asphalt, Mortar, and Low-Cost POP Ceilings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral wool owned 41.12% of the ceiling tiles market share in 2025 as architects valued its thermal and acoustic duality. Metal panels, mainly aluminum, are rising at a 9.03% CAGR because they resist humidity and carry A1 fire ratings required at airports and metros. Gypsum tiles dominate cost-conscious residential builds, though POP competition is squeezing margins in India and Southeast Asia. Composite, PVC, and wood options serve luxury niches seeking organic aesthetics with customized graphics.

Asia Pacific is the backbone of metal's rise, with projects like Hong Kong's Three Runway System and India's metro expansion referencing EN 13501-1 and IS 1646:2023 non-combustible standards. In Europe and North America, mineral wool holds sway in retrofits, driven by the importance of environmental product declarations and WELL acoustic scores. Gypsum's cost-effectiveness ensures its continued use, yet its moisture sensitivity poses challenges in bathrooms and humid climates. Highlighting a market trend, bio-based innovations like Armstrong's Ultima LEC tile signal a move towards lower-carbon raw materials in the ceiling tiles industry.

Geography Analysis

North America held 35.34% of 2025 revenue, supported by LEED v4.1 and WELL adoption, plus stable retrofit demand. Asia Pacific is forecast to grow at a 10.56% CAGR, reflecting China's metro stations, India's airport upgrades, and ASEAN's transit hubs, all of which call for non-combustible solutions. Europe's share stays resilient through mineral-wool retrofits that satisfy the EU Building Performance Directive. Latin America and the Middle East-Africa register mid-single-digit expansion driven by Brazil's residential starts and GCC luxury developments.

China's construction output increased in 2024, concentrating mineral wool and metal tile usage in Tier-1 and Tier-2 commercial builds. Japan's aging stock spurs acoustic retrofits, while Vietnam, Thailand, and Indonesia tighten fire codes, inviting A1-rated products. The ceiling tiles market outlook remains most upbeat in Asia, where rapid urbanization converges with stricter safety standards.

- AWI Licensing LLC

- Foshan Ron Building Material Trading

- Georgia-Pacific

- Guangzhou Titan Building Materials Co., Ltd.

- Haining Shamrock Import & Export Co. Ltd.

- Hunter Douglas N.V.

- Imerys

- Kingspan Group

- Knauf Group

- Mada Gypsum Company

- New Ceiling Tiles LLC

- Odenwald Faserplattenwerk GmbH

- PVC Ceilings SA

- ROCKWOOL A/S

- Saint-Gobain

- SAS International

- Shandong Huamei Building Materials Co., Ltd.

- Techno Ceiling Products

- USG Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of acoustic systems in open-plan offices

- 4.2.2 Green-building credits boosting mineral-wool retrofits in Europe

- 4.2.3 Metro airport build-outs mandating non-combustible tiles in Asia

- 4.2.4 Digital-print gypsum tiles enabling premiumisation in GCC luxury real estate

- 4.2.5 Bio-based binders cutting embodied-carbon of mineral-fibre tiles

- 4.3 Market Restraints

- 4.3.1 Energy-price volatility inflating mineral-wool costs

- 4.3.2 Threat from substitutes such as asphalt mortar

- 4.3.3 Low-cost POP ceilings constraining gypsum-tile uptake in Asia-Pacific

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Mineral Wool

- 5.1.2 Metal

- 5.1.3 Gypsum

- 5.1.4 Others (Composite, Plastic and Wood)

- 5.2 By Property

- 5.2.1 Acoustic

- 5.2.2 Non-Acoustic

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.4 By Geography

- 5.4.1 Asia Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AWI Licensing LLC

- 6.4.2 Foshan Ron Building Material Trading

- 6.4.3 Georgia-Pacific

- 6.4.4 Guangzhou Titan Building Materials Co., Ltd.

- 6.4.5 Haining Shamrock Import & Export Co. Ltd.

- 6.4.6 Hunter Douglas N.V.

- 6.4.7 Imerys

- 6.4.8 Kingspan Group

- 6.4.9 Knauf Group

- 6.4.10 Mada Gypsum Company

- 6.4.11 New Ceiling Tiles LLC

- 6.4.12 Odenwald Faserplattenwerk GmbH

- 6.4.13 PVC Ceilings SA

- 6.4.14 ROCKWOOL A/S

- 6.4.15 Saint-Gobain

- 6.4.16 SAS International

- 6.4.17 Shandong Huamei Building Materials Co., Ltd.

- 6.4.18 Techno Ceiling Products

- 6.4.19 USG Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment