PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066386

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066386

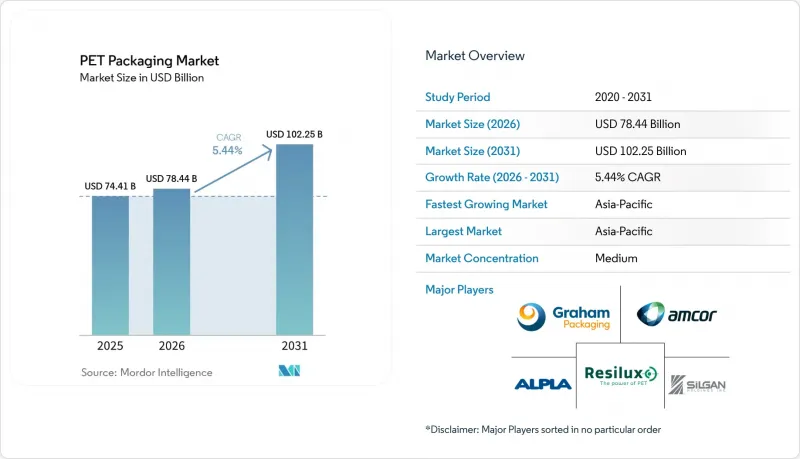

PET Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the PET packaging market size was valued at USD 74.41 billion in 2025 and is forecasted to grow from USD 78.44 billion in 2026 to USD 102.25 billion by 2031, advancing at a CAGR of 5.44% during 2026-2031.

This report is Segmented by Packaging Format (Rigid PET Packaging, and Flexible PET Packaging), Product Type (Bottles and Jars, Pouches and Sachets, and More), Resin Grade (Virgin PET, and Recycled PET), End-User Industry (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Household, Industrial Goods, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global PET Packaging Market Trends and Insights

High Recyclability And Light-Weighting Advantage

The PET packaging market continues to gain from the way light-weighting and recyclability reinforce each other rather than compete with each other. Lower resin use reduces material cost and transport load, while the same package still fits into an established recycling stream in many end uses. This matters because commercial filling lines have already spent years optimizing PET bottle performance, especially in beverages where scale and line speed remain decisive. The regulatory position of food-contact recycling also favors PET because post-consumer mechanical PET recycling remains the only currently authorized route for recycled plastic materials intended for food contact under the relevant EU framework. Procurement teams are therefore treating weight reduction less as a narrow cost exercise and more as a circular packaging requirement tied to contract renewal, portfolio compliance, and long-run supply stability. The PET packaging market is likely to keep benefiting from this dual advantage because few alternative substrates can match both material efficiency and closed-loop acceptance at a commercial scale.

Food-Grade Recycled PET Mandates In Europe And The United States

The PET packaging market is being pushed forward by rules that have already moved beyond policy intent and into enforceable timelines. In Europe, the Single-Use Plastics Directive required 25% recycled content in PET beverage bottles from January 2025, and the Packaging and Packaging Waste Regulation is expected to take recycled-content requirements further for contact-sensitive packaging by 2030 and 2040. In the United States, California AB 793 required 25% recycled content in beverage bottles from 2025 and set a 50% threshold for 2030. These staggered rules are forcing brand owners to sign longer offtake agreements earlier than they would under normal market conditions because waiting for spot supply is becoming a riskier strategy. That is shifting capital decisions across the PET packaging market toward recyclers, processors, and converters that can secure compliant food-grade rPET ahead of enforcement deadlines. The PET packaging market is also seeing spillover into Asia because suppliers that can meet Western food-contact standards are becoming more attractive export partners for global consumer brands.

Volatility In Virgin PET Resin Prices

The PET packaging market remains exposed to feedstock volatility because virgin PET economics are closely tied to purified terephthalic acid and monoethylene glycol. These inputs still shape converter margins, especially where procurement contracts lag changes in upstream pricing. Margin stress is most visible among smaller converters that lack long-term supply cover or integrated sourcing positions. In those cases, resin swings can erase pricing gains and make customer negotiations more difficult during the contract period. The PET packaging market is therefore seeing stronger pressure toward consolidation because larger players can spread raw material risk across scale, geography, and contract structure. This restraint does not change the long-run demand case for PET, but it does make near-term profitability less stable and rewards converters that can lock in feedstock access earlier.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Chemical Recycling Infrastructure

- E-Commerce Demand For Impact-Resistant Lightweight Packaging

- Emerging Bans On Single-Use Sachets In Developing Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid PET packaging held 64.78% of the PET packaging market share in 2025, which shows how firmly the category is anchored in high-volume filling systems. Bottled water, carbonated drinks, and edible oils still rely on PET bottles because line speed, barrier performance, and collection systems have been built around them for decades. That makes material switching expensive, even when brand owners are under pressure to improve sustainability metrics. The PET packaging industry also benefits from the fact that rigid PET is already embedded in recovery systems that support bottle-to-bottle recycling in the most regulated markets. This structural advantage means rigid formats are likely to remain the volume base of the PET packaging market throughout the forecast period.

Flexible PET packaging is projected to grow at a 5.98% CAGR through 2031, which is faster than rigid PET packaging and points to widening end-use relevance. Growth is being supported by mono-material designs that are replacing non-recyclable multi-layer laminates in selected food and personal care applications. This is important because it expands PET into categories that had previously favored barrier combinations that were harder to recycle at scale. The PET packaging market is therefore seeing growth in flexible and rigid applications at the same time, rather than a simple shift from one format to the other. That balance supports broader capacity investment because converters can serve stable bottle demand while also chasing higher-growth flexible use cases. The PET packaging market should continue to reward suppliers that can link flexible innovation to recyclability claims that customers can verify in procurement processes.

Bottles and jars accounted for a 68.91% share of the PET packaging market size in 2025, making them the clear anchor of product-level value. Their lead reflects the global beverage sector's long investment cycle in bottle-specific collection, sorting, and recycling infrastructure. This installed base keeps replacement risk low because competing formats would need to match cost, scale, and downstream compatibility at the same time. Bottles and jars also remain central in food, household, and pharmaceutical applications where product visibility and container integrity shape buying decisions. As a result, the PET packaging market still draws much of its current value from categories where bottles and jars remain the commercial default.

Pouches and sachets are forecasted to grow at a 6.22% CAGR through 2031, which keeps them as the fastest-growing product type in the PET packaging market. Their appeal remains strongest in low-income consumer markets where single-serve price points matter and distribution networks favor lightweight packaging. Preforms are also becoming more important in parts of Africa and the Middle East, where local blow-molding can be more economical than importing finished bottles. At the same time, the outlook for sachets is no longer straightforward because legislation in India and Nigeria has introduced a real policy overhang for this sub-segment. This means the PET packaging market still has room for sachet-led growth in the near term, but capacity built around that format now carries more medium-term risk than bottle-focused assets. Converters that can serve both affordable pack sizes and more regulation-ready formats will be better placed as the PET packaging market adapts to uneven policy enforcement across regions.

Geography Analysis

Asia-Pacific held 47.38% of the PET packaging market share in 2025, which kept it well ahead of every other region. The region is projected to grow at a 6.42% CAGR through 2031, which makes it the fastest-growing geography in the PET packaging market. China and India remain the main anchors because one combines a very large resin and packaging scale, while the other is expanding quickly across food processing and personal care manufacturing. India has become more important for recycled content planning because its FSSAI rule requires 30% recycled content in Category-1 rigid plastic packaging from FY2026. This is drawing more investment into domestic rPET capacity and strengthening the case for India as a future regional supply hub. Japan and South Korea continue to matter for higher-specification bottle development, especially in premium beverages and nutraceutical formats where barrier performance and design precision carry more weight.

Europe remains the most tightly regulated region in the PET packaging market, and this continues to shape demand, investment timing, and sourcing behavior. The EU Single-Use Plastics Directive already required 25% recycled content in PET beverage bottles from January 2025, while the Packaging and Packaging Waste Regulation began its application phase on August 12, 2026, and is expected to tighten recycled-content expectations further over time. The UK is adding separate cost pressure because its Plastic Packaging Tax rose to GBP 228.82 (USD 307.75) per tonne in 2026 for packs with less than 30% recycled content. These rules are increasing the demand for food-contact-grade rPET faster than the existing supply can comfortably support. North America is facing a related pattern because California AB 793 is pushing recycled-content compliance while converters also manage tighter sourcing conditions for domestic supply. The PET packaging market in these regions is therefore moving toward earlier contracting, more vertical integration, and stronger interest in traceable recycled supply.

Africa is anticipated to witness robust growth due to various factors like urbanization, retail formalization, and the move toward individually packaged consumer goods, which continue to support demand across the region. At the same time, policy action against some single-use formats is changing investment priorities, with Nigeria's regulatory process signaling more pressure on sachets and a stronger case for recoverable rigid PET formats. South America is expected to deliver moderate but steady expansion in bottled water, carbonated beverages, and edible oil, while the Middle East is balancing feedstock risk with local manufacturing investment that should reduce import dependence over time.

- Amcor plc

- Resilux NV

- Gerresheimer AG

- ALPLA Werke Alwin Lehner GmbH and Co KG

- Silgan Holdings Inc.

- Graham Packaging Company LP

- GTX Hanex Plastic Sp. z o.o.

- Dunmore Corporation

- Comar LLC

- TOPPAN Holdings Inc.

- Huhtamaki Oyj

- Nampak Ltd.

- Plastipak Holdings Inc.

- ACTI PACK S.A.S

- RETAL Industries Ltd.

- Sealed Air Corporation

- Pactiv Evergreen Inc.

- Uflex Ltd.

- Zhongfu Industrial Co. Ltd.

- Novapet S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Recyclability and Light-Weighting Advantage

- 4.2.2 Food-Grade Recycled PET Mandates in Europe and United States

- 4.2.3 Expansion of Chemical Recycling Infrastructure

- 4.2.4 E-Commerce Demand for Impact-Resistant Lightweight Packaging

- 4.2.5 Integration of Digital Watermarking for Automated Sorting

- 4.2.6 Adoption of Mono-Material PET Caps and Closures Enabling Bottle-to-Bottle Recycling

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin PET Resin Prices

- 4.3.2 Emerging Bans on Single-Use Sachets in Developing Countries

- 4.3.3 Supply Gap in Bottle-Grade rPET

- 4.3.4 Consumer Shift Toward Plastic-Free Packaging Alternatives

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Format

- 5.1.1 Rigid PET Packaging

- 5.1.2 Flexible PET Packaging

- 5.2 By Product Type

- 5.2.1 Bottles and Jars

- 5.2.2 Pouches and Sachets

- 5.2.3 Trays and Clamshells

- 5.2.4 Lids-Caps and Closures

- 5.2.5 Preforms and Other Product Types

- 5.3 By Resin Grade

- 5.3.1 Virgin PET

- 5.3.2 Recycled PET

- 5.4 By End-User Industry

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceuticals

- 5.4.3 Personal Care and Cosmetics

- 5.4.4 Household

- 5.4.5 Industrial Goods

- 5.4.6 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Resilux NV

- 6.4.3 Gerresheimer AG

- 6.4.4 ALPLA Werke Alwin Lehner GmbH and Co KG

- 6.4.5 Silgan Holdings Inc.

- 6.4.6 Graham Packaging Company LP

- 6.4.7 GTX Hanex Plastic Sp. z o.o.

- 6.4.8 Dunmore Corporation

- 6.4.9 Comar LLC

- 6.4.10 TOPPAN Holdings Inc.

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Nampak Ltd.

- 6.4.13 Plastipak Holdings Inc.

- 6.4.14 ACTI PACK S.A.S

- 6.4.15 RETAL Industries Ltd.

- 6.4.16 Sealed Air Corporation

- 6.4.17 Pactiv Evergreen Inc.

- 6.4.18 Uflex Ltd.

- 6.4.19 Zhongfu Industrial Co. Ltd.

- 6.4.20 Novapet S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment