PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066405

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066405

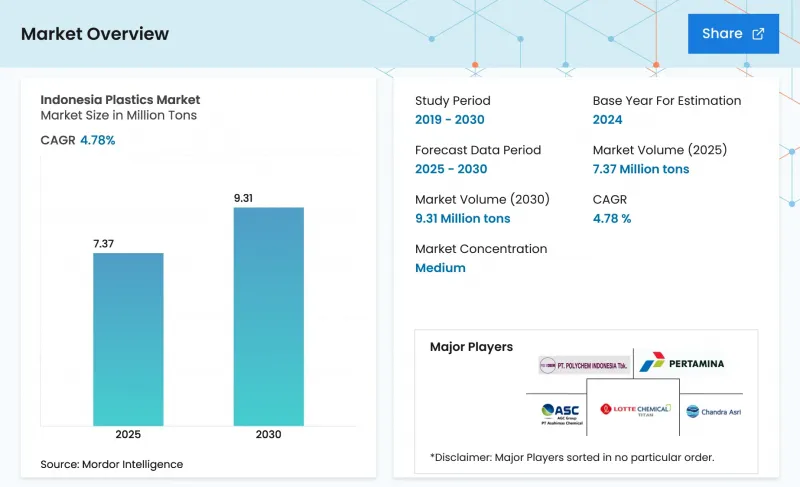

Indonesia Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia plastics market size is expected to grow from 7.42 million tons in 2025 to 7.76 million tons in 2026 and is forecast to reach 9.67 million tons by 2031 at 4.52% CAGR over 2026-2031.

This report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Blow Molding, Extrusion, Injection Molding, and Other Technologies), and Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

Indonesia Plastics Market Trends and Insights

Expansion of Downstream Petro-Complexes

The November 2025 start-up of a 1 million ton ethylene cracker and 450,000 ton polyethylene unit in Cilegon eliminates the need for imported ethylene on Java, cuts pipeline logistics, and leverages up to 50% LPG (liquefied petroleum gas) feedstock flexibility that arbitrages naphtha-LPG spreads. A re-scoped CAP-2 project adds chlor-alkali and ethylene dichloride (EDC) output in 2027, shrinking Indonesia's vinyl import gap, while a planned 720,000 tons polyethylene terephthalate (PET) line set for 2028 lowers beverage-grade reliance on foreign supply. Together, these builds lift projected domestic coverage of overall resin demand to 70% by 2031 and unlock roughly USD 2 billion in annual economic value. Integrated layouts also concentrate skilled labor and shared utilities, reinforcing Java's status as the nucleus of the Indonesia Plastics market. The combined scale is expected to soften feedstock price volatility, though grid congestion around Merak and Cilegon must still be eased to fully capture logistics savings.

Lightweight Auto-Parts Adoption by OEMs

Automotive assemblers are targeting 10% curb-weight cuts that can translate into 6-8% fuel savings, prompting a steady switch from steel to engineering plastics such as PC-ABS blends for dashboards and polyamide for under-hood parts. Tier-1 suppliers in Karawang source locally compounded grades, which reduces import lead time and ring-fence original equipment manufacturers (OEMs) from forex swings. ASEAN harmonized standards reward lower CO2 output, intensifying demand for flame-retardant, high-temperature resins ahead of rising electric-vehicle penetration. Limited domestic capacity for niche polymers like polybutylene terephthalate (PBT) continues to pull in imports from Japan and South Korea, yet joint-venture talks signal momentum toward onshore specialty polymer plants. These moves fortify value capture across the Indonesia Plastics market, even as commodity margins tighten.

30% Excise on Single-Use Plastic Bags

Draft excise legislation proposes IDR 30,000 per kg for thin HDPE and LDPE bags, threatening a 5-8% volume hit for film-grade resin suppliers if enacted in 2026. Retailers could pivot to reusable totes or thicker HDPE bags that dodge weight thresholds, softening true environmental gains. Municipal enforcement capacity varies, as past bans in Banjarmasin and Bogor suffered compliance gaps. The uncertainty already stalls new LDPE capacity investments, with converters waiting for final tax brackets before signing long-term offtake deals. Policy clarity is therefore critical for stable growth in the Indonesia Plastics market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Logistics Boom

- Mandatory EPR and Waste-Segregation Pilots

- Carbon-Pricing Scheme Raising Energy Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional Plastics secured 75.12% of Indonesia Plastics market share in 2025, with polyethylene and polypropylene making up the bulk of film, bottle, and injection molded items. The Indonesia Plastics market size for these grades rose in tandem with e-commerce packaging and construction pipe demand. Polyethylene benefits from high output at newly commissioned Cilegon lines, and polypropylene growth tracks automotive bumper and raffia sack orders. PVC usage in pipe and cable remains resilient, though some converters experiment with polyolefin substitution to navigate chlorine scrutiny.

Engineering Plastics, though smaller in tonnage, command premium pricing in electronics housings and under-hood auto parts, lifting their revenue footprint. PET is set for a capacity burst once a 720,000-ton plant starts in 2028, improving bottle-grade security and trimming import bills. Bioplastics, led by seaweed resins, hold a thin volume but are expected to grow with the fastest CAGR of 6.12% during the forecast period (2025-2031), mirroring global bans on single-use fossil plastics. The Indonesia Plastics market size for biopolymer grades hinges on cost convergence and potential tax credits that are still on the policy table.

List of Companies Covered in this Report:

- Asahimas Chemical Company

- Chandra Asri Group

- Dow

- LOTTE CHEMICAL TITAN HOLDING BERHAD

- LyondellBasell Industries N.V.

- Mitsubishi Chemical Group Corporation

- PT Indonesia Nanya Indah Plastics

- PT Pertamina (Persero)

- PT Polychem Indonesia Tbk

- PT Standard Toyo Polymer (Tosoh Corporation)

- PTT Global Chemical Public Company Limited

- Sulfindo Adiusaha

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of downstream petro-complexes (Cilegon, Tuban)

- 4.2.2 Lightweight auto-parts adoption by OEMs

- 4.2.3 E-commerce logistics boom needing durable secondary packs

- 4.2.4 Mandatory EPR and waste-segregation pilots fueling recyclable resin demand

- 4.2.5 Sea-weed based bioplastics clusters in East Java

- 4.3 Market Restraints

- 4.3.1 30 % excise on single-use plastic bags (from 2026)

- 4.3.2 Carbon-pricing scheme raising energy costs

- 4.3.3 Rail-infrastructure gaps inflating inland resin logistics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyvinyl Chloride (PVC)

- 5.1.1.4 Polystyrene (PS)

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polyamides

- 5.1.2.3 Polycarbonates

- 5.1.2.4 Styrene Copolymers (ABS and SAN)

- 5.1.2.5 Polybutylene Terephthalate (PBT)

- 5.1.2.6 Fluoropolymers

- 5.1.2.7 Polyoxymethylene (POM)

- 5.1.2.8 Polymethyl Methacrylate (PMMA)

- 5.1.2.9 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 By Technology

- 5.2.1 Blow Molding

- 5.2.2 Extrusion

- 5.2.3 Injection Molding

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Furniture and Bedding

- 5.3.6 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Asahimas Chemical Company

- 6.4.2 Chandra Asri Group

- 6.4.3 Dow

- 6.4.4 LOTTE CHEMICAL TITAN HOLDING BERHAD

- 6.4.5 LyondellBasell Industries N.V.

- 6.4.6 Mitsubishi Chemical Group Corporation

- 6.4.7 PT Indonesia Nanya Indah Plastics

- 6.4.8 PT Pertamina (Persero)

- 6.4.9 PT Polychem Indonesia Tbk

- 6.4.10 PT Standard Toyo Polymer (Tosoh Corporation)

- 6.4.11 PTT Global Chemical Public Company Limited

- 6.4.12 Sulfindo Adiusaha

- 6.4.13 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment