PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066410

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066410

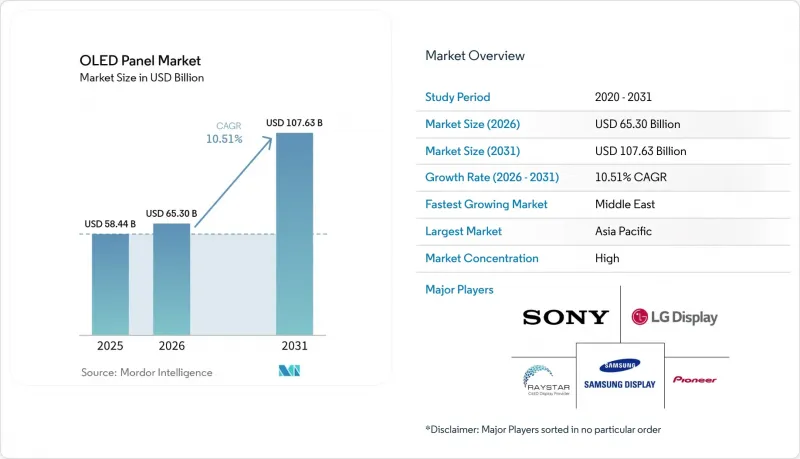

OLED Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the oLED panel market size was valued at USD 58.44 billion in 2025 and is estimated to grow from USD 65.30 billion in 2026 to reach USD 107.63 billion by 2031, at a CAGR of 10.51% during the forecast period (2026-2031).

This report is Segmented by Type (Flexible, Rigid, and Transparent), Display Address Scheme (PMOLED Display, and AMOLED Display), Size (Small-Sized, Medium-Sized, and Large-Sized), Product (Mobile and Tablet, Television, Automotive, Wearable, Lighting Products, Healthcare Devices, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global OLED Panel Market Trends and Insights

Rising Adoption of Flexible OLEDs In Smartphones

Flexible OLED penetration reached 57% of smartphone shipments in Q1 2025 as Chinese Android brands standardized flex panels in mid-tier models and Apple migrated every iPhone SKU to OLED. Unit prices for 6-inch flexible panels are trending below USD 30 by 2027 as Samsung Display's Asan Gen-8-line scales output. The narrowing 15% price gap versus rigid OLEDs positions flex architectures as the default choice, relegating rigid units to feature phones and industrial controls. IEC 62715-2:2022 certification frameworks simplify OEM qualification, further accelerating adoption.

Price-Driven Shift from Rigid to Flexible Supply in China

BOE's USD 8.9 billion Chengdu fab and CSOT's USD 4.1 billion Guangzhou printed-OLED facility add a combined 54,500 substrates per month, compressing rigid utilization below 50% and cutting the flex-rigid price spread to under 15%. Chinese brands now specify flexible OLEDs for smartphones priced under USD 300, squeezing older rigid lines in Korea and Taiwan and prompting conversion or exit strategies. Short-run oversupply risk persists, but accelerated depreciation and government incentives sustain Chinese fabs until demand matches capacity.

Persistent Blue-Emitter Lifetime Limitations

Fluorescent blue emitters exhibit half-lives below 10,000 hours at 1,000 nits, forcing panel makers to overdrive subpixels and adopt tandem stacks, which add USD 50-80 per panel. The cost penalty constrains OLED uptake in 75-inch-plus televisions, where mini-LED LCD delivers comparable HDR at 60% of the price. Commercial blue phosphorescent solutions remain elusive despite ongoing Universal Display R&D, leaving lifetime as OLED's Achilles' heel in ultra-large and high-luminance applications.

Other drivers and restraints analyzed in the detailed report include:

- Emergence Of LTPO Backplanes in Mainstream Models

- Rapid OLED Penetration in Gaming Monitors and Laptops

- Competition From Mini-LED LCD And Micro-LED Roadmaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The OLED panel market size for flexible formats captured USD 29.9 billion in 2025 and is forecast to expand at a 10.81% CAGR as smartphone vendors and IT OEMs pivot to bendable, rollable, and curved displays. Transparent variants, although only 2% of 2025 revenue, will rise fastest at 11.09% CAGR through 2031 thanks to automotive A-pillar integration and retail signage. Rigid panel demand continues to shrink, falling below 20% of segment revenue by 2028. Material savings from printed, maskless processes and higher substrate throughput at Gen-8 fabs will keep flexible pricing competitive against legacy rigid units even as Chinese subsidies taper.

Design latitude drives flexible OLED beyond handsets into laptops, tablets, and wearables. Samsung Display's 17-inch rollable laptop screen and Hyundai Mobis's 18-inch curved cockpit module illustrate how bend radius and thinness unlock novel industrial designs. Transparent OLEDs still struggle with 40% lower transmittance than clear glass, limiting outdoor readability, but indoor transportation and smart-city projects in Seoul and Dubai demonstrate emerging commercial viability. Overall, flexible architecture secures its position as the default across consumer electronics while rigid panels retreat to niche industrial utilities.

AMOLED commanded 83.63% revenue in 2025 and remains the workhorse engine of the OLED panel market. LTPO-AMOLED, the fastest-growing subset at 10.95% CAGR, marries oxide and poly-silicon transistors to enable 1-120 Hz refresh modulation, reducing handset power budgets by up to one-fifth. The OLED panel market share for LTPO reached 18% in 2025 and is projected to surpass 35% by 2031 as Apple, Samsung, and Chinese rivals standardize the feature in premium tiers.

PMOLED lingers in sub-2-inch wearables and industrial displays but will slip below 5% revenue contribution by 2029. Japan Display's eLEAP process, boosting aperture ratios to 60% and doubling luminance, advances AMOLED longevity in notebooks and automotive dashboards. Compliance with the IEC 62341 series eases homologation across regions, reinforcing AMOLED's lead as mini-LED LCD and micro-LED face scaling hurdles.

Geography Analysis

Asia Pacific controlled 71.49% of 2025 revenue, propelled by China's 52.1% share of global panel turnover and USD 13 billion in cumulative Gen-8/9 capex by BOE and CSOT. South Korea retained technological primacy, owning 82.6% of OLED TV output and 64.5% of iPhone 17 panel supply, while Japan focused on high brightness eLEAP devices. India, with sub-30% smartphone OLED penetration, remains price sensitive but shows upside as domestic brands pivot to affordable flexible AMOLED imports. Asia Pacific thus remains the production heartland, balancing Chinese scale and Korean innovation.

North America and Europe contributed premium demand without domestic fabrication. The regions shipped 1.83 million OLED TVs in H1 2025, a 13% annual uptick, buoyed by 77-inch units falling below USD 3,000. Automotive OLED momentum is notable in Europe, where Mercedes-Benz, Audi, and BMW deploy both interior and exterior OLED modules, leveraging established tier-one supply chains. Apple's all-OLED 2025 iPhone lineup further enlarges North American flexible panel pull-through.

The Middle East, though accounting for a small revenue base, is forecast to grow at 11.83% CAGR as Saudi Arabia's NEOM and the UAE's smart-city programs specify transparent and signage OLEDs for public infrastructure. South America and Africa trail with sub-10% penetration due to currency volatility and import tariffs that inflate retail prices. Hence, while traditional regions continue to dominate, targeted infrastructure deployments in the Gulf states provide a fresh spur to diversified geographic revenue.

- LG Display Co., Ltd

- Sony Corporation

- Pioneer Corporation

- Raystar Optronics Inc.

- Ritek Corporation

- OSRAM OLED GmbH

- WiseChip Semiconductor Inc.

- Winstar Display Co. Ltd

- Visionox Co. Ltd

- BOE Technology Group Co., Ltd

- Tianma Microelectronics Co., Ltd

- AU Optronics Corp.

- Japan Display Inc.

- Universal Display Corporation

- CSOT (China Star)

- JOLED Inc.

- Everdisplay Optronics (EDO)

- Sharp Corporation

- Royole Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Flexible OLEDs in Smartphones

- 4.2.2 Price-Driven Shift From Rigid to Flexible Supply in China

- 4.2.3 Emergence of LTPO Backplanes in Mainstream Models

- 4.2.4 Rapid OLED Penetration in Gaming Monitors and Laptops

- 4.2.5 Demand for Curved and Free-Form Automotive Cockpit Displays

- 4.2.6 Increasing Brand Adoption of Foldable and Rollable Form Factors

- 4.3 Market Restraints

- 4.3.1 Persistent Blue-Emitter Lifetime Limitations

- 4.3.2 Competition From Mini-LED LCD and Micro-LED Roadmaps

- 4.3.3 Capital-Intensive Gen-8/9 OLED Fab Build-outs

- 4.3.4 Oversupply Risk From Aggressive Chinese Capacity Expansion

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Flexible

- 5.1.2 Rigid

- 5.1.3 Transparent

- 5.2 By Display Address Scheme

- 5.2.1 PMOLED Display

- 5.2.2 AMOLED Display

- 5.3 By Size

- 5.3.1 Small-Sized OLED Panel

- 5.3.2 Medium-Sized OLED Panel

- 5.3.3 Large-Sized OLED Panel

- 5.4 By Product

- 5.4.1 Mobile and Tablet

- 5.4.2 Television

- 5.4.3 Automotive

- 5.4.4 Wearable

- 5.4.5 Lighting Products

- 5.4.6 Healthcare Devices

- 5.4.7 Home Appliances

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 LG Display Co., Ltd

- 6.4.2 Sony Corporation

- 6.4.3 Pioneer Corporation

- 6.4.4 Raystar Optronics Inc.

- 6.4.5 Ritek Corporation

- 6.4.6 OSRAM OLED GmbH

- 6.4.7 WiseChip Semiconductor Inc.

- 6.4.8 Winstar Display Co. Ltd

- 6.4.9 Visionox Co. Ltd

- 6.4.10 BOE Technology Group Co., Ltd

- 6.4.11 Tianma Microelectronics Co., Ltd

- 6.4.12 AU Optronics Corp.

- 6.4.13 Japan Display Inc.

- 6.4.14 Universal Display Corporation

- 6.4.15 CSOT (China Star)

- 6.4.16 JOLED Inc.

- 6.4.17 Everdisplay Optronics (EDO)

- 6.4.18 Sharp Corporation

- 6.4.19 Royole Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment