PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066424

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066424

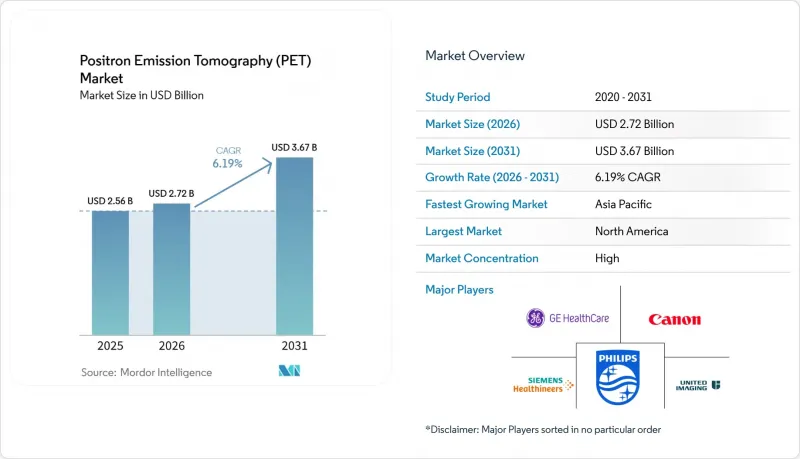

Positron Emission Tomography (PET) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the positron emission tomography market size was valued at USD 2.56 billion in 2025 and is estimated to grow from USD 2.72 billion in 2026 to reach USD 3.67 billion by 2031, at a CAGR of 6.19% during the forecast period (2026-2031).

This report is Segmented by Product Type (Stand-Alone PET Systems, PET/CT Systems, PET/MRI Systems, Cyclotrons, Software & Services), Detector Technology (Photomultiplier Tube, Silicon Photomultiplier), Application (Oncology, and More), End User (Hospitals & Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Positron Emission Tomography (PET) Market Trends and Insights

Rising Prevalence of Oncology Cases

Cancer diagnoses in the United States are expected to reach 2.05 million in 2025, up 3.2% from 2024. Globally, new cases could hit 28 million by 2040 as populations age and smoking persists in parts of Southeast Asia. PET imaging supports both staging and response monitoring, especially for immunotherapy where metabolic activity changes precede anatomical shrinkage. Oncology already delivers 71.74% of scan volume, yet limited reimbursement for routine surveillance restrains growth potential. U.S. data show lung-cancer staging PET uptake at 87%, but post-therapy surveillance only at 34%, leaving significant untapped revenue.

Rapid Shift Toward Fully-Digital PET Detectors

Silicon photomultiplier modules powered 44% of new system installs in 2025, an increase from 31% two years earlier. Timing resolution below 250 picoseconds doubles signal-to-noise ratio, enabling 40% faster workflows or 50% lower tracer doses. GE HealthCare's Discovery MI Gen 2 and Canon Medical's Cartesion Prime exemplify this performance leap. Hospitals can now schedule 12 daily scans rather than 8 on legacy systems, improving equipment utilization by one-third. Manufacturing scale remains a hurdle, since SiPM detectors cost 25% more than photomultiplier tubes, but a new Shanghai fabrication plant promises price parity within three years.

High Capital and Maintenance Costs of PET Systems

Digital PET/CT systems average USD 3.8 million while PET/MRI exceeds USD 4.5 million, and annual service contracts can top USD 300,000. India, for instance, operated only 142 scanners in 2025, equivalent to 0.1 units per million residents, compared with 5.2 in the United States. To manage cost, hospitals extend equipment life to 12 years and favor software subscriptions rather than full replacements, a trend that suppresses new-system volume but fuels aftermarket revenue.

Other drivers and restraints analyzed in the detailed report include:

- Commercialisation of Total-Body PET Enabling Ultra-Low-Dose Imaging

- AI-Enabled Image Reconstruction Reducing Scan Time and Cost

- Radio-Isotope 18F-FDG Supply-Chain Vulnerability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PET/CT systems generated 42.46% of 2025 revenue, underscoring their oncology foothold and favorable reimbursement. Still, PET/MRI platforms will rise at a 10.62% CAGR through 2031 because neurology and cardiac clinicians value MRI soft-tissue contrast. Siemens logged 34 Biograph mMR installs in 2025, and GE placed 22 SIGNA PET/MR units, mostly in neuroscience centers. Software and services rose 12.3% during 2025, reflecting the industry's pivot to subscription models that spread cost across operating budgets. Regulatory momentum from CMS proposals for differentiated hybrid-imaging codes could lift the positron emission tomography market size for PET/MRI beyond this baseline.

Second-tier modalities maintain niche roles. Stand-alone PET caters to radiochemistry labs, while cyclotron sales follow local isotope demand. North America added eight medical cyclotrons in 2025, and China installed fourteen to meet its expanding positron emission tomography market capacity.

Photomultiplier tubes still held 56.24% of revenue in 2025 because of a large installed base and a USD 500,000 price advantage per system. Silicon photomultipliers are forecast to grow 9.67% annually to 2031 due to 40% faster scans and 2-fold lesion detectability gains. Clinical trials comparing United Imaging's uMI Panorama to PMT systems reported 94% sensitivity for sub-centimeter liver lesions versus 76% on older technology. Hospitals therefore plan upgrades once detector costs fall, a scenario likely by 2028 as automotive-scale manufacturing drives economies of scale. Lower injected dose requirements, meanwhile, stretch each radiopharmaceutical batch across more patients, partially easing isotope bottlenecks.

Geography Analysis

North America captured 42.83% of 2025 revenue, supported by 1,740 installed scanners and comprehensive Medicare coverage. The region's 5.8% forecast CAGR lags the global rate because new installations give way to digital replacements. Outcome-based codes introduced in 2024 already encourage upgrades to SiPM and AI-ready platforms. Canada added fourteen scanners in 2025, while Mexico's private hospitals installed six units, indicating modest secondary-market expansion.

Asia-Pacific is set to grow at 8.41% CAGR through 2031, driven by China's goal of 500 new scanners in tier-2 cities by 2027 and India's USD 120 million diagnostic-infrastructure allocation. United Imaging captured 52% of China's 2025 installs with competitively priced systems. Japan's aging population fuels neurology scans, and South Korea's cancer-screening program maintains oncology demand. India's limited cyclotron network remains a bottleneck, restraining rural access despite government funding. Australia's quartet of PET/MRI installs positions it as a neuroscience hub within the region.

In Europe, Germany's 187-scanner base underpins its oncology capacity, and France added twelve units focused on theranostics research. The United Kingdom installed six scanners in 2025 but earmarked GBP 200 million for imaging by 2027, signaling faster growth ahead. EU medical-device rules add six to twelve months of approval time for AI software, damping early adoption. Middle East & Africa and South America together show incremental growth, led by GCC private-hospital demand and eight new systems in Brazil's Sao Paulo corridor.

- Advanced Cyclotron Systems Inc

- Canon

- Cubresa Inc.

- Eckert & Ziegler

- GE Healthcare

- IBA Radiopharma Solutions

- Koninklijke Philips

- Mediso Medical Imaging Systems

- MinFound Medical

- Neusoft Medical Systems

- Positron

- Shimadzu

- Siemens Healthineers

- SOFIE Biosciences

- Sumitomo Heavy Industries

- TeamBest

- United Imaging Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Oncology Cases

- 4.2.2 Rapid Shift Toward Fully Digital PET Detectors

- 4.2.3 Growing Uptake of Hybrid PET/CT And PET/MRI Platforms

- 4.2.4 Expanding Reimbursement Coverage in OECD Countries

- 4.2.5 Commercialization of Total-Body PET Enabling Ultra-Low-Dose Imaging

- 4.2.6 AI-Enabled Image Reconstruction Reducing Scan Time & Cost

- 4.3 Market Restraints

- 4.3.1 High Capital & Maintenance Costs of PET Systems

- 4.3.2 Radioisotope (18F-FDG) Supply Chain Vulnerability

- 4.3.3 Limited 68Ge/68Ga Generator Production Capacity

- 4.3.4 Data-Governance Hurdles for AI-Driven Diagnostics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Stand-alone PET Systems

- 5.1.2 PET/CT Systems

- 5.1.3 PET/MRI Systems

- 5.1.4 Cyclotrons

- 5.1.5 Software & Services

- 5.2 By Detector Technology

- 5.2.1 Photomultiplier Tube (PMT)

- 5.2.2 Silicon Photomultiplier (SiPM)

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Cardiology

- 5.3.3 Neurology

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Diagnostic Imaging Centres

- 5.4.3 Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Advanced Cyclotron Systems Inc

- 6.3.2 Canon Medical Systems

- 6.3.3 Cubresa Inc.

- 6.3.4 Eckert & Ziegler

- 6.3.5 GE HealthCare

- 6.3.6 IBA Radiopharma Solutions

- 6.3.7 Koninklijke Philips N.V.

- 6.3.8 Mediso Medical Imaging Systems

- 6.3.9 MinFound Medical

- 6.3.10 Neusoft Medical Systems

- 6.3.11 Positron Corporation

- 6.3.12 Shimadzu Corporation

- 6.3.13 Siemens Healthineers

- 6.3.14 SOFIE Biosciences

- 6.3.15 Sumitomo Heavy Industries

- 6.3.16 TeamBest

- 6.3.17 United Imaging Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment