PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066430

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066430

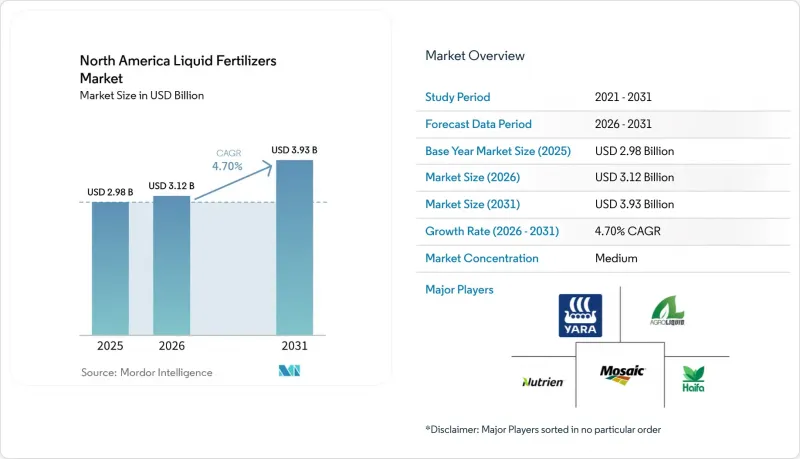

North America Liquid Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america liquid fertilizers market size is projected to expand from USD 2.98 billion in 2025 and USD 3.12 billion in 2026 to USD 3.93 billion by 2031, registering a 4.70% CAGR between 2026 and 2031.

This report is Segmented by Nutrient Type (Nitrogen, Potassium, Phosphate, and Micronutrients), by Ingredient Type (Organic and Synthetic), by Mode of Application (Starter Solution, Foliar Application, Fertigation, and More), by Crop Type (Grains and Cereals, Pulses and Oilseeds, and More), and by Geography (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America Liquid Fertilizers Market Trends and Insights

Precision-Agriculture Adoption Accelerates Demand for Liquid Nutrients

Variable-rate equipment covers around 40% of large farms across the Corn Belt and Prairie Provinces, allowing liquids to be metered more precisely than granules. The adoption of fertigation in high-value crops, such as fruits, vegetables, and specialty grains, is rising, particularly in water-managed regions of the United States and Canada. Liquid fertilizers are compatible with drip and pivot irrigation systems, allowing for simultaneous irrigation and nutrient delivery. This approach enhances nutrient-use efficiency while reducing the number of application passes and associated fuel costs.

Shift to Fertigation Under Water-Scarcity Programs

California's groundwater law and similar rules in Arizona and Texas push growers toward drip and micro-irrigation that rely on soluble liquids. Multiple small fertigation doses follow crop uptake curves, cutting leaching losses and volatilization. Texas High Plains conversions lifted regional liquid sales by double digits in 2024-2025. Arizona vegetable farms documented nitrogen savings of 25% to 30% after switching from broadcast granules. Compliance deadlines make fertigation a non-negotiable transition for many producers. State and federal conservation programs, supported by agencies such as the United States Department of Agriculture Natural Resources Conservation Service (USDA NRCS), offer financial assistance for drip and micro-irrigation infrastructure. These subsidies help lower initial capital costs for growers, making fertigation systems and their associated liquid fertilizers more cost-effective while supporting objectives for water-use efficiency and nutrient management compliance.

Corrosive Handling and Storage Infrastructure Costs

Urea Ammonium Nitrate (UAN) and ammonium polyphosphate require stainless tanks and corrosion-resistant pumps, which roughly doubles capex compared to dry storage solutions. Secondary containment adds further expense, discouraging small dealers from stocking liquids and limiting rural service density. Liquid fertilizer systems, particularly those using Urea Ammonium Nitrate (UAN), accelerate wear on seals, valves, hoses, and pump components due to their corrosive properties. This results in more frequent replacements, increased downtime during critical application periods, and higher operating costs compared to dry fertilizer handling systems.

Other drivers and restraints analyzed in the detailed report include:

- Crop-Specific Liquid Blends Launched by Tier 1 Suppliers

- Adoption of Aerial and Drone Foliar Spraying

- Cold-Chain Constraints for Biologically Enhanced Liquids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nitrogen led the segment with 54% of the North America liquid fertilizers market share in 2025, supported by large corn and wheat acreages that favor sidedress Urea Ammonium Nitrate (UAN) . Corn, wheat, and soybean acreage in the United States and Canada continues to drive significant demand for nitrogen fertilizers, particularly in liquid form, due to their quick soil absorption and compatibility with variable-rate application and fertigation systems.

Micronutrients are forecast to grow at a 7.1% CAGR through 2031, spurred by iron and zinc deficiencies across calcareous soils in the upper Midwest. The adoption of digital agronomy tools and soil-testing platforms by growers has increased demand for targeted micronutrient applications, such as zinc, iron, manganese, and boron. Unlike commodity nitrogen fertilizers, micronutrients and custom liquid blends are priced higher per gallon, providing suppliers with improved profitability and encouraging investment in research and development as well as customized formulations.

Synthetic formulations held the largest segment, 72% of the North America liquid fertilizers market size in 2025, but expanded modestly as commodity acreage is already well penetrated. Synthetic liquid fertilizers, such as urea-ammonium nitrate (UAN), ammonium polyphosphate, and potassium nitrate, are widely used because they deliver highly concentrated nutrients in readily soluble forms. Their predictable nutrient composition enables growers to precisely match application rates to crop requirements, making them particularly suitable for large-scale grain and cereal production. Additionally, synthetic liquid fertilizers integrate effectively with variable-rate and fertigation systems, further solidifying their role in modern North American agricultural practices.

Organic liquids are advancing at a 8.1% CAGR to 2031, driven by demand from certified facilities and greenhouse vegetables that require National Organic Program compliance. Organic liquid fertilizers, derived from plant, animal, or microbial sources, are increasingly adopted for fruits, vegetables, and specialty crops. These fertilizers enhance soil health and microbial activity while aligning with regulatory and consumer-driven sustainability objectives. High-value crop growers are particularly drawn to organic liquids for their ability to deliver targeted nutrients without synthetic residues, thereby supporting both product quality and environmental sustainability.

List of Companies Covered in this Report:

- The Mosaic Company

- CF Industries Holdings Inc.

- AgroLiquid

- Haifa Group

- Kugler Company

- Sociedad Quimica y Minera de Chile SA

- EuroChem Group AG

- K+S Aktiengesellschaft

- Triangle C. C.

- Yara International ASA

- Helena Agri-Enterprises

- Tessenderlo Group

- Brandt Consolidated Inc.

- Grupa Azoty SA

- Nufarm Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision-agriculture adoption accelerates demand for liquid nutrients

- 4.2.2 Shift to fertigation under water-scarcity programs

- 4.2.3 Crop-specific liquid blends launched by Tier-1 suppliers

- 4.2.4 Government incentives for domestic fertilizer capacity

- 4.2.5 Adoption of aerial and drone foliar spraying

- 4.2.6 Growth of controlled-environment agriculture hubs

- 4.3 Market Restraints

- 4.3.1 Corrosive handling and storage infrastructure costs

- 4.3.2 Volatility of natural-gas feedstock prices

- 4.3.3 Per- and polyfluoroalkyl substances (PFAS) and emerging contaminant regulation pressure

- 4.3.4 Cold-chain constraints for biologically enhanced liquids

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Nutrient Type

- 5.1.1 Nitrogen

- 5.1.2 Potassium

- 5.1.3 Phosphate

- 5.1.4 Micronutrients

- 5.2 By Ingredient Type

- 5.2.1 Organic

- 5.2.2 Synthetic

- 5.3 By Mode of Application

- 5.3.1 Starter Solution

- 5.3.2 Foliar Application

- 5.3.3 Fertigation

- 5.3.4 Injection into Soil

- 5.3.5 Aerial and Drone Application

- 5.4 By Crop Type

- 5.4.1 Grains and Cereals

- 5.4.2 Pulses and Oilseeds

- 5.4.3 Commercial Crops

- 5.4.4 Fruits and Vegetables

- 5.4.5 Turf and Ornamentals

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 The Mosaic Company

- 6.4.2 CF Industries Holdings Inc.

- 6.4.3 AgroLiquid

- 6.4.4 Haifa Group

- 6.4.5 Kugler Company

- 6.4.6 Sociedad Quimica y Minera de Chile SA

- 6.4.7 EuroChem Group AG

- 6.4.8 K+S Aktiengesellschaft

- 6.4.9 Triangle C. C.

- 6.4.10 Yara International ASA

- 6.4.11 Helena Agri-Enterprises

- 6.4.12 Tessenderlo Group

- 6.4.13 Brandt Consolidated Inc.

- 6.4.14 Grupa Azoty SA

- 6.4.15 Nufarm Limited

7 Market Opportunities and Future Outlook