PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066460

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066460

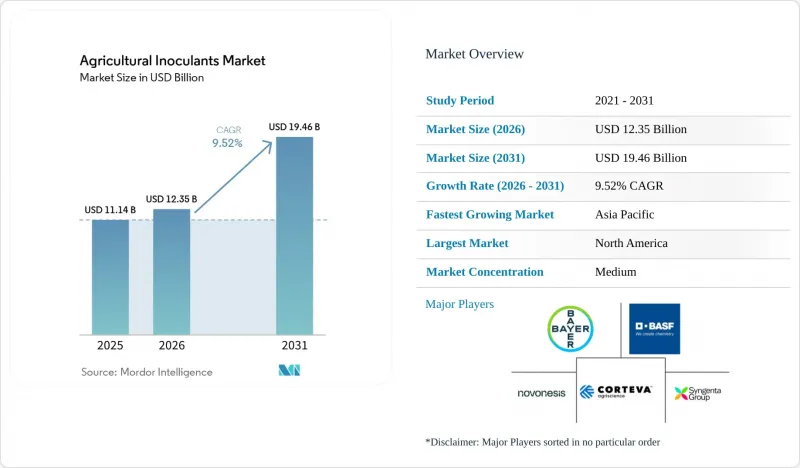

Agricultural Inoculants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agricultural inoculants market size is projected to grow from USD 11.14 billion in 2025 to USD 12.35 billion in 2026 and is forecast to reach USD 19.46 billion by 2031 at 9.52% CAGR over 2026-2031.

This report is Segmented by Function (Crop Nutrition and Biocontrol Agents), Microorganism (Bacteria, Fungi, and Viruses), Mode of Application (Seed Treatment, Soil Treatment, and Foliar Spray), Crop Type (Grains and Cereals, Oilseeds, Commercial Crops, and More), Formulation (Liquid and Dry), and Geography (North America, Asia-Pacific, South America, and More). Forecasts are in Terms of Value (USD).

Global Agricultural Inoculants Market Trends and Insights

Organic Acreage Expansion and Residue-Free Food Demand

The agricultural inoculants market is experiencing growth due to the expansion of organic farming and stricter residue standards in global food supply chains. Consumers in the European Union and North America are increasingly demanding agricultural products with minimal residues, driving the adoption of biological crop inputs. This trend is extending beyond high-value fruits and vegetables to include large-scale field crops. In 2025, the European Commission's bioeconomy framework identified bio-based fertilizers and biological plant-protection products as strategic priorities, promoting their integration into agricultural sustainability initiatives. For growers, positioning products as residue-free enhances market access and ensures pricing stability in compliance-driven sales channels, thereby strengthening the commercial importance of inoculants beyond sustainability-focused applications.

Biofertilizer Adoption to Offset Synthetic Input Cost Volatility

The agricultural inoculants market is also growing as farmers adopt microbial nutrition products to reduce dependence on volatile fertilizer prices and improve nutrient-use efficiency. Instead of completely replacing synthetic fertilizers, many farms are incorporating inoculants to enhance nitrogen fixation and phosphorus uptake within conventional nutrient-management systems. This approach is particularly significant in fertilizer-import-dependent agricultural economies, where input-cost fluctuations can heavily impact farm profitability. A study published in Plants demonstrated that co-inoculation with Bradyrhizobium species and Azospirillum brasilense in certain regions of Brazil's soybean cultivation resulted in significant savings in urea replacement and direct profitability gains. This finding highlights why growers consider these products as effective economic tools. The same study also shows that inoculants are being adopted as part of integrated nutrient programs rather than as simple substitutes for conventional fertilizers. As a result, the Agricultural inoculants market is benefiting from both input cost discipline and better return visibility.

Performance Variability Across Soil and Climate Conditions

Performance variability remains a significant challenge for the agricultural inoculants market, as microbial activity is highly dependent on factors such as soil temperature, moisture, pH, crop history, and native microbial populations. Consequently, inoculants often exhibit inconsistent field performance compared to synthetic inputs, particularly in large-scale farming operations and under varying environmental conditions. Industrial microbiology highlights that the efficacy of inoculants remains significantly influenced by environmental conditions, carrier design, and post-application survival conditions. This variability contributes to a trust gap, as growers seek predictable input responses for reliable planning. Without more precise field recommendations, the agricultural inoculants market is likely to continue to face hesitation in regions with climates and soils that yield inconsistent results.

Other drivers and restraints analyzed in the detailed report include:

- Policy Support for Biologicals and Lower-Residue Crop Protection

- Seed Treatment Adoption to Improve Application Precision

- Farmer Preference for Fast-Acting Synthetic Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biocontrol agents accounted for the largest market share at 58.1% in 2025, making the most significant contribution to the agricultural inoculants market across functional categories. This dominance is attributed to increasing resistance to synthetic pesticides in key pest systems and stricter regulations on certain chemically active ingredients in major crop markets. The agricultural inoculants market continues to rely on biocontrol agents, as they benefit from a well-established commercial infrastructure compared to other biological categories. Companies such as BASF SE, Valent BioSciences LLC, and Koppert Biological Systems B.V. operate in this segment with robust biological pest management portfolios, ensuring global supply capabilities and distributor confidence.

Crop nutrition is the fastest-growing function, projected to expand at a CAGR of 5.1% through 2031. This growth reflects a broader shift in how growers approach nutrient efficiency. In the agricultural inoculants market, biostimulants are increasingly marketed as practical tools for enhancing nutrient uptake and managing stress, rather than as optional plant health supplements. This shift is significant as agronomists can now integrate biostimulants into reduced-rate fertilizer programs, rather than requiring farmers to completely replace conventional systems. In March 2026, BASF SE completed the acquisition of AgBiTech Group, emphasizing the growing focus of major crop input companies on integrating biological technologies into their portfolio strategies and long-term growth plans. Consequently, while mature biocontrol platforms continue to anchor revenue, nutrition-focused products are growing faster in the agricultural inoculants market.

Bacteria accounted for the largest market share in 2025, at 43.4%, representing the most significant segment of the agricultural inoculants market by microorganism. This dominance is attributed to the long-standing commercial use of strains such as Bradyrhizobium, Azospirillum brasilense, and Bacillus subtilis, which are utilized for nitrogen fixation, nutrient mobilization, and plant growth enhancement. In the agricultural inoculants market, bacterial products benefit from established registration processes and widespread application in soybean, pulse, and cereal systems. South America plays a critical role in this segment, as rhizobial products are closely linked to legume production and the economic viability of soybean cultivation. While fungal inoculants are also significant, particularly in horticulture and soil-borne disease management, bacteria continue to provide the broadest commercial base across regions.

Viruses represent the fastest-growing segment of microorganisms, with a projected CAGR of 8.0% through 2031. This growth is driven by the increasing adoption of nucleopolyhedrovirus technologies for managing challenging lepidopteran pests. The agricultural inoculants market is focusing more on this segment as advancements in production economics and field validation make virus-based pest control more scalable.

Geography Analysis

North America held 32.1% of the agricultural inoculants market share in 2025 and remained the largest regional contributor. Strong retailer networks, advanced agronomic advisory systems, and high adoption across soybean and corn production supported this. The United States continues to lead regional demand as microbial products integrate efficiently with seed treatment, crop protection, and sustainability-focused farming programs. In 2025, Pivot Bio, Inc. further expanded adoption through its N-OVATOR program and broader retail partnerships across the Corn Belt. This reinforced the role of biological inputs in improving both farm productivity and environmental performance.

Asia-Pacific is the fastest regional segment with a projected 6.8% CAGR through 2031. This growth is driven by fertilizer cost pressures, government support for biological inputs, and expanding agronomic extension programs. India remains a key growth market as regulatory formalization improves commercialization standards for biological products. In September 2024, Novonesis A/S strengthened its regional presence through its partnership with Krishak Bharati Cooperative Limited (KRIBHCO) to distribute mycorrhizal biofertilizers across major Indian crops. Australia also supports regional growth by increasing the adoption of precision agriculture.

Europe remains an important market for agricultural inoculants, although growth is partly constrained by current European Union regulations governing microorganisms. Ongoing regulatory reviews by the European Commission may gradually expand the list of approved microbial products. South America continues to be a major growth region, particularly in Brazil, where large-scale soybean cultivation and reliance on fertilizer imports are driving rising demand for biological inputs. The Middle East and Africa remain smaller markets but are attracting increasing industry attention because lower historical adoption leaves room for expansion through new distribution and advisory models, particularly in legume production systems.

- BASF SE

- Bayer AG

- Novonesis A/S

- Corteva, Inc.

- Syngenta Group Co., Ltd.

- Valent BioSciences LLC

- Premier Tech Ltd.

- Lallemand Inc.

- Bioceres Crop Solutions Corp.

- Verdesian Life Sciences LLC

- Groundwork BioAg Ltd.

- Pivot Bio, Inc.

- Koppert Biological Systems B.V.

- XiteBio Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Organic acreage expansion and residue-free food demand

- 4.2.2 Biofertilizer adoption to offset synthetic input cost volatility

- 4.2.3 Policy support for biologicals and lower-residue crop protection

- 4.2.4 Seed treatment adoption to improve application precision

- 4.2.5 On-farm compatibility demand for integrated biological programs

- 4.2.6 Shelf-life gains from formulation and encapsulation innovation

- 4.3 Market Restraints

- 4.3.1 Performance variability across soil and climate conditions

- 4.3.2 Farmer preference for fast-acting synthetic alternatives

- 4.3.3 Registration complexity for multi-strain microbial products

- 4.3.4 Cold-chain and contamination risk in microbe distribution

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Crop Nutrition

- 5.1.2 Biocontrol Agents

- 5.2 By Microorganism

- 5.2.1 Bacteria

- 5.2.1.1 Bacillus

- 5.2.1.2 Azotobacter

- 5.2.1.3 Rhizobium and Bradyrhizobium

- 5.2.1.4 Phosphate-solubilizing bacteria

- 5.2.2 Fungi

- 5.2.2.1 Trichoderma

- 5.2.2.2 Mycorrhiza

- 5.2.2.3 Beauveria bassiana

- 5.2.2.4 Metarhizium anisopliae

- 5.2.3 Viruses

- 5.2.1 Bacteria

- 5.3 By Mode of Application

- 5.3.1 Seed Treatment

- 5.3.2 Soil Treatment

- 5.3.3 Foliar Spray

- 5.4 By Crop Type

- 5.4.1 Grains and Cereals

- 5.4.2 Pulses and Oilseeds

- 5.4.3 Commercial Crops

- 5.4.4 Fruits and Vegetables

- 5.4.5 Other Applications

- 5.5 By Formulation

- 5.5.1 Liquid

- 5.5.2 Dry

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Italy

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Kenya

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Novonesis A/S

- 6.4.4 Corteva, Inc.

- 6.4.5 Syngenta Group Co., Ltd.

- 6.4.6 Valent BioSciences LLC

- 6.4.7 Premier Tech Ltd.

- 6.4.8 Lallemand Inc.

- 6.4.9 Bioceres Crop Solutions Corp.

- 6.4.10 Verdesian Life Sciences LLC

- 6.4.11 Groundwork BioAg Ltd.

- 6.4.12 Pivot Bio, Inc.

- 6.4.13 Koppert Biological Systems B.V.

- 6.4.14 XiteBio Technologies Inc.

7 Market Opportunities and Future Outlook